{kind=link}

THE TAX MAN HANGS AROUND FOR LIFE

In February like clock-work we get a letter in the post from the city about our new tax rate along with payment dates for our property tax bill. Whether it’s paying for income tax, property tax, product tax or anything that says tax you know you’ll never get away with dodging it.

Which is why there are two certainties in life: death and taxes

Every year the property tax bill gets higher and higher but that’s expected I suppose since it goes to pay for various things in the community such as municipal services, police, fire, transit and so on.

I received an email from a young couple in the process of buying their first home and they wanted to know what the best way was to pay for their property tax bill.

Dear Mr.CBB,

My wife and I are just finalizing the sale of our new home and were wondering how we should pay for our property tax bill in order for our budget to balance. What else is there that we need to know about our new property and our tax bill? Thanks for any tips.

-Chris and Angela

If you don’t own a home yet you may not know what a property tax bill is so let me give you the basic rundown so you’re prepared for the time you buy your first house. It seems like you will be budgeting which is a must no matter if you rent or own a home.

If you do choose to pay for your property tax bill on your own what we do is include it monthly as a projected expense in our budget. This way the money is saved in our bank account and ready for when the bill comes due. It’s also earning interest along the way.

Our property tax bill is approximately $3,600 per year. There are normally four separate payments of $900 per payment date. To save up monthly we set aside $300 ($3600 / 12 months) a month in our projected expenses. Actual number is $319.68 but I rounded it to an even number for the example. That way, we always have our property tax payment ready to go and as it sits there, it earns a little interest along the way.

I’ll explain more below…come along with me.

What is a property tax bill?

The property tax bill has two portions and is a levy tax that is set by the municipality in which you live in based on the assessed value of your home. The property tax bill is comprised of the municipality portion of the bill and the education factor. Yes, you pay for the education system regardless if you have kids or not. Rates for the education portion are established by the Ministry of Finance

Paying for your property tax bill

When you are a first time home buyer you may not know how you have to pay for your property tax bill unless your mortgage company has opted to save the money by adding it to your mortgage payments.

Most people like to do this so they

- Don’t spend the money they should be saving for their property tax bill

- They may forget to save the money for their property tax bill

- Convenience – set it and forget it

If you don’t want to give the bank your money to hang on to until it’s time to pay your property tax bill which they will do on your behalf you can save the money yourself. This way you can earn a bit of interest with the money or if you are savvy at investing even more.

Why throw money away if you are organized and not worried about missing payments on your property tax bill?

That is how we chose to pay our property tax bill and still continue to do so even though we are mortgage free.

Other ways you can pay for your property tax bill might be;

- Pre-authorized Payment Plans where the city takes money from your bank account at certain times of the year.

- You may be able to pay monthly instead of in one large sum which means your account will be debited monthly until the property tax bill is due. This helps those people who are worried about spending the money if they don’t set it aside.

- Your city may also offer other plans that may work for your budget so contact them and ask.

How do they calculate how much my property tax bill will be?

Good question and I’ve touched on this before in previous post but I’ll go over it again.

Your property tax bill is based on an assessment sent to you in the mail by the Municipal Property Assessment Corporation (MPAC). Once they have your home assessment value they multiply it by the municipality and education tax rates for your property class. In other words depending on where you live and what the assessed value of your house is will determine just how much you will be paying.

What is MPAC?

MPAC is the largest assessment jurisdiction in North America, responsible for accurately assessing and classifying more than five million properties in Ontario in compliance with the Assessment Act and regulations set by the Government of Ontario.

In the Fall of 2012 every homeowner in Ontario received their property assessment with the next assessment being held in 2016. So, we should expect an updated property assessment soon.

To establish your property’s assessed value, MPAC analyzes property sales in your area. This method, called Current Value Assessment, is used by most assessment jurisdictions in North America. Over 200 different factors are considered when assessing residential property; however, five major factors account for approximately 85% of the value.

There are 5 things that affect your MPAC assessment

- Location

- Lot Dimensions

- Living Area

- Age of Property

- Quality of Construction

We live in a higher-end neighbourhood so our property taxes near $3600 where the interim amount is based from the previous years tax levy. Most people just pay it but others may want to make sure that what they are paying is accurate which means they go to the first source of data, their MPAC assessment which will tell you the value of your home. Sometimes this value may be incorrect so changes need to be made.

You can learn all about your property by visiting MPAC AboutMyProperty where you will learn everything you need to know about your current house assessment.

Here, you’ll learn how and why your property was assessed the way it was. Plus you can compare your property assessment with others in your neighbourhood and community. You can also file a Request for Reconsideration through AboutMyPropertyTM if you do not agree with your property’s assessment.

What I’ve learned lately though is that MPAC is legislatively responsible to update assessments as they see fit which means you might receive a new assessment even in an off-year. The main reasons being structural change, property sale, property value change, renovations, new home build and demolition, change to the tax liability of the property or support for a different school system.

There are two school systems, the Public school system and the Catholic school system. If you choose to change who you support you could expect a new assessment in the mail.

MPAC is legislatively responsible for updating this information even in a year when a province-wide Assessment Update is not taking place.

Chris and Angela I hope this short post answers your question but click on all the links which will direct you to even more information right from MPAC. Contact your mortgage company to make sure you haven’t already agreed to pay for your property tax bill with your mortgage payments and certainly drop by and chat to your city municipal office.

Thanks for your question and congrats on your new home purchase.

-MR.CBB

Where our money went in February

Do you know where your money goes every month? We do!

Do you know where your money goes every month? We do!

In February the biggest chunk of money went to pay Property Taxes which ran us just under $1000. I also picked up some products for the bathroom renovations which I’m hoping to start come the Spring so I’m looking for sale items as I go along.

Another expense was paying $134 for our son to get vaccinated for Meningococcal meningitis by the B strain. This is only one of 2 shots he needs to get so we will endure this expense once again. Pretty much no benefits plan will cover Bexsero from what the Pharmacist told us. If yours happens to, lucky for you.

We also pay our electricity and water now monthly which is different from before as it was paid bi-monthly. The cost has also gone up which is no surprise especially if you live in Ontario. Kijiji was our friend this month as we picked up a large box of kids books for $25 and some home decor that my wife was thrilled to get for such a low price. We are considering re-selling it for more but right now she’s got me hanging it on the walls.

Other than that we didn’t have much time to spend any money unless we were going to the grocery store which these days seems like the family outing of the week apart from bringing our son to the gym.

On a good note I do have one day a week off now for the next 6 weeks so I will be using that time to spend with my family.

Pick a budget that’s right for you

I’m currently offering 2 versions of our budget and the reason behind it is simple. Firstly, read the CBB blog disclaimer because what you do with it is your own business so if you mess it up you need to sort that out.

I have not closed off any cells so you can make all the changes you like to the budget to reflect your lifestyle which is what you asked me for in your emails. (See I do listen and read your comments and emails)

Although I would love to help every single fan with their budget I am unable to do so but I am always willing to answer any emails you send me so don’t be shy.

This was after all meant to be our personal budget and although I would love to customize it for every fan that wants to use it but, I’m afraid I cannot.

I’m not selling this budget or hope to make any money from it so enjoy this free budget and I hope that it works for you as much as it does for us.

Sneak peek at our free budget spreadsheet

You can download the free budget spreadsheets here.

- Budget 1– You can use the pre-existing categories or you can use your own if you wish and you have the option to use projected expenses or not. Please read all notes left around the budget for tips.

- Budget 2– Everything is pre-set so you have to use the pre-defined categories but this budget will generate year-end budget figures where the other one won’t but you must use the categories already in this budget. If you change anything you will mess up the formulas and year-end figures.

- Please read all notes left around the budget for tips.

Test the budget for a month and see how it goes.

Our family budget plan

How we budget our monthly expenses?

I often have fans ask me how to budget money on a low-income or they simply a high debt load and want to kill it like my friend Tony who got rid of over $100,000 worth of debt by using a budget.

CBB fans want to know what we do in order to save so much money and the reply I give is simple>> It’s not about the money it’s about the process involved.

We are both money managers of our finances and with our relationship compatibility we have been able to get to where we are in 2016, debt free.

It doesn’t matter if you are using a cash only budget or you use your debit and credit cards, if your budget doesn’t balance you have budget issues you should check it pronto.

Learning how to be your own money manager is important because no one else will care about your money more than YOU!.

We don’t always save as much money as we would like every month but most importantly we are not going into debt but only because we are budgeting our money. In fact we are currently debt-free including the mortgage which means all we pay for is our monthly bills and expenses.

One of the most important things we did for our personal finances was that we never let the budget deter us from reaching our goals.

Sure we’ve had crap months but we’ve made up for it or we learned from our mistakes just like we should. Budget failure only occurs when you give up on your budget which should not happen as long as you truly want to reach your goals.

We didn’t always earn the income we do today but made do with what we were earning so we didn’t go into debt. That my friends is called “living below your means”. The only science to becoming rich!

Sometimes fans email and ask me if living on a budget in Canada is any different from living and budgeting in other countries. To be honest I’m going to say, probably not.

If I still lived in the UK I could use this exact budget spreadsheet to meet all of my needs however the budget needs to be reviewed monthly.

Below are links to the budgeting series which I wrote while designing our excel budget spreadsheet which will give you an idea just how we designed our budget.

I’m not a financial planner/advisor so I can’t tell you how you should budget but I can show you how we budget. I’m just a regular guy just like everyone else; some might call me a budget or numbers nerd.

Learn how to budget with Mr.CBB

Our Budgeting Series

Do you want to learn to budget like we do?

We explain everything we do and more in this mini-series below all about budgeting.

Please take the time to read through our budgeting series plus read Budgeting in the New Year. I hope the information will help stop you from making common budgeting mistakes that I hear of often and that you take something away from the information and apply it to your financial situation.

If you have any questions about what we do with our budget money tracker feel free to email me.

- How We Designed Our Budget Step 1– Gathering All the information

- How We Designed Our Budget Step 2– Budget Categories

- How We Designed Our Budget Step 3– Tracking Receipts

- How We Designed Our Budget Step 4- Note-taking

- How We Designed Our Budget Step 5– 5S Organization

- How We Designed Our Budget Step 6– Who Does What and When?

- How We Designed Our Budget Step 7– Balancing Our Budget

- How We Designed Our Budget Step 8– Knowing our Coupon Savings

- How We Designed Our Budget Step 9– Reading Our Bills

- How We Designed Our Budget Step 10– Projected Expenses

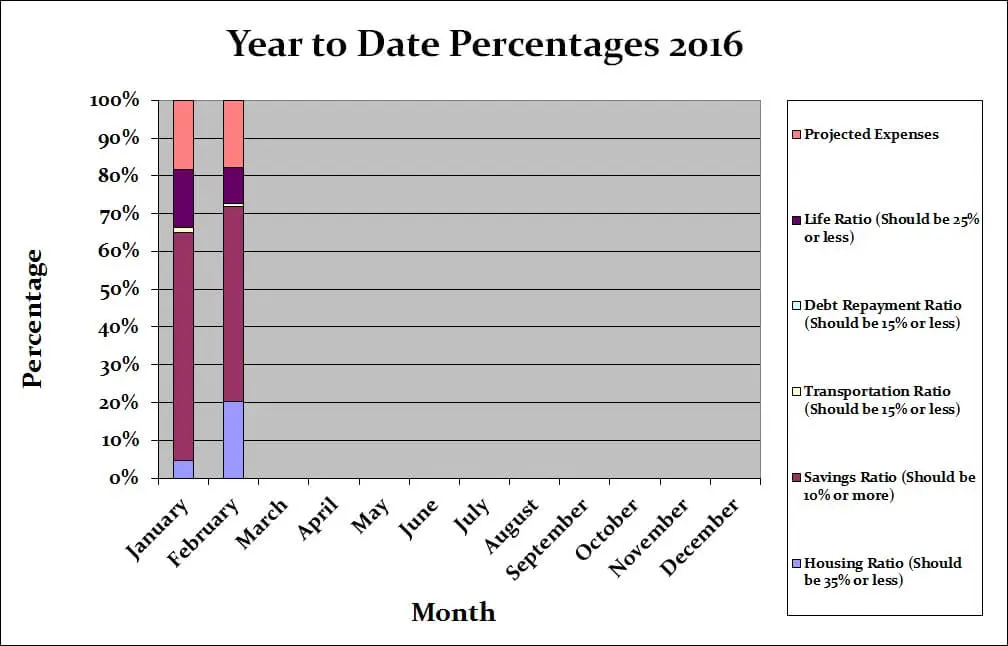

Budget percentages February 2016

Our savings of 51.54% includes savings and investments and emergency savings for this month. If you include the projected expenses savings, we actually saved 69.40% of our income.

The monthly totals comes to 100% which shows that we spent our income this month and used the rest as emergency savings.

The other categories were well within the defined percentage limits. Our projected expenses this month is at 17.86%.

Budget percentages month by month

Breaking down expenses

This is simply a breakdown of our expenses which has helped us to understand where all of our money goes. Since May 2014 we have been mortgage free so much of our money will be directed at savings, investments and renovations.

I appreciate that you enjoy this budget update each month but I do hope you view this as an educational tool rather than comparing your own financial numbers as our situations are all unique.

Although I encourage your comments and love to hear what you have to say about our budget categories and expenses please don’t tell us to donate our money to charities because we have too much or are fortunate. We are hardly out of the clear with finances for the rest of our lives and have worked and sacrificed to get where we are. We do plan to enjoy the money we’ve saved now since we haven’t over the years with our son.

What we do with our “extra cash” is our business and although we do donate to a charity we won’t be putting it on display for the world to see as it defeats the purpose in my eyes. It is part of the budget as you see it. I hope that clears that up for those of you who had concerns about our extra money.

Almost 8 years ago I started working in Canada making a bit over minimum wage and have since moved up the ladder. I’m now working very hard to secure my dream job with one foot in the door. We aren’t all lucky but if you do the best you can at least you can look back and say you gave it a shot.

Sometimes we wish we had more money to budget with but understand that we only have what we earn and if we want more, we need to earn more. Spending less than we earn and budgeting our money has been the easiest way for us to pay down debt and save money.

- Chequing– This is the bank account where all of our debt gets paid from.

- Emergency Savings Account– This is a high-interest savings account.

- Regular Savings Account– This is a savings account that holds our projected expenses.

- Monthly Budgeted Total: $5,093.64

- Monthly Net Income Total: $10,736.34

- (Check out our Ultimate Grocery Guide to see where our grocery money goes)

- Projected Expenses: These are expenses we know we will pay for throughout the year = $1,917.68

- Total Expenses Actually Paid Out: $4,538.77

- Total Expenses Actually Paid Out: Calculated is $10,736.34 (total net monthly income) – $1,917.68 (projected expenses) – $4,279.89 (emergency savings) = $3,840.27

- Actual Cash Savings going into Emergency Savings: Calculated is $10,736.34 (total monthly net income) – $4,538.77 (actual expenses paid out for the month) – $1,917.68 (projected expenses) = $4,279.89

Sving for stuff you haven’t yet paid for…but need to!

What are Projected Expenses? – We project expenses throughout the year so we have the money saved. PE= A projected expense is money automatically saved each month so it is ready when the bill comes in or when you need it as in the example below.

We review our projected expenses at the beginning of the year to set up our yearly budget and adjust as we go along if a new projected expense arises and needs to be added to the budget. Sometimes we remove a projected expense as well so it’s very important to keep an eye on your expenses.

This has happened on many occasions but it’s bound to happen as we can’t predict everything we have to pay for over the course of the year. The important part for us is that we are saving for these expenses and we no longer have to stress about taking money from our savings to pay for them. To learn more about projected expenses read Step 10 in my budgeting series.

When we spend the money in a projected expense category we move that money to our chequing account in order to pay for that incoming expense. So this means the numbers go up and down in the projected expenses account based on what we need to pay for that we saved for in the account over time.

The only thing you need to do is track your projected expenses each month manually as I can’t customize that for you in the excel budget spreadsheet as I don’t know what you will use for projected expenses.

For now we will have to manually track which means month after month we add up what we save in each projected expense category and minus what we spend so we know how much we have and what is left in each category. I have updated our personal excel budget spreadsheet for 2016.

We pay money into the projected expenses account continually throughout the year even when bills come due as its revolving so as one bill gets paid the money continues to come in from the other categories all year-long. This ensures that money is always available. It may not always be enough but having something ready is better than having nothing at all and having to use credit.

So the $1917.68 gets paid into the projected expense account every month no matter what. It seems to be easier to track our money this way but you can do what works best for you.

Sample Projected Expense

If our clothing category was a projected expense we would have a budget of $50 per month for the two of us. If we spend $30 on clothes for the month that means we need to pull $30 from the projected expenses account to pay for this expense or we move only $20 to projected expenses for the month and leave the $30 in your chequing account.

It’s up to you how you do it as I mentioned above. My plan is to create a projected expenses spreadsheet to track the expenses all year-long otherwise you need to do it manually which we currently do in order to make sure we don’t overspend what we haven’t saved or will save over the course of the year.

It’s a fairly easy process and becomes a lifestyle change for your finances but the most important part is that the money is available and saved, which means potentially less stress.

This means we should have $600.00 per year for clothing to spend. We have to track that expense as we spend it manually but hopefully for our 2015 budget I can incorporate that into our spreadsheet so it tallies the numbers up as we go along. That way we will be able to know exactly what we’ve spent as an ongoing total.

(Note: I am working on this but slowly as I wasn’t anticipating all the extra hours with my second job)

Our actual family budget

Time for the juicy category numbers and to see how we made out with our monthly budget. Below you will see two tables, one is our monthly budget and the other is our actual budget for the month of February 2016. This budget represents 2 adults and a toddler plus our investments.

If it is highlighted in blue that means it is a projected expense. You will also see our budget does not include the emergency savings as this is factored in at the end.

Budget for February 2016

March 2016 Goals

As you can see I didn’t accomplish much with my goals in February apart from re-vamping some old blog posts. It’s been busy working 2 jobs but little by little I’m tackling what I can.

I cut down the goals section for 2016 to keep it simple. I was spending too much time focusing on social media numbers which I can’t really control.

- Find a used dresser for our sons clothes on the main level of the house

- Call around to lawyers to talk about getting a Will written up

- Finish sanding and stain our sons kitchen table and chairs

- Start revamping old blog posts (2 a month)- I did complete this in February.

- Finish the master bathroom shower-

- Pick out new tiles for bathroom and accessories (mirror, towel bar holder etc.)-

- Buy a new blind for the garage-

- Finish the walls in the baby room-

- Write down what we want in our new kitchen-

- Start looking at pricing for a new insulated garage door-

- Buy a pressure washer-

- Sort through our sons clothes and sell some-

- Research Kitchen designers in our area-

- Start researching vacation spots for 2016-

- Hang paintings and wrought iron decor on the walls-

- Take down Christmas decor outside if weather permits-

Budget updates month by month

In case you missed our budget updates and want to do a quick search I’ve compiled them all on one handy page: monthly budgets. For the 2016 Year I will also keep track of each month below and update the monthly budgets page.

I will start the list off with our end of year budget update from 2015 just in case you missed it.

That’s all for this month check back at the beginning of April 2016 to see how we made out with our March 2016 budget.

Happy Budgeting CBB’ers!

Are You New To Canadian Budget Binder?

- Find me on Social Media by clicking any one of the links below

- Check out my new Free Recipe Index

- If you like FREE then click this link for my FREE Excel Budget Spreadsheet and all my Free Money Saving Lists!

- You can now have full access to my Ultimate Grocery Shopping Guide in Canada.