{kind=link}

THINK BEFORE YOU ACT ESPECIALLY WITH YOUR FINANCES.

Giving up something doesn’t have to mean giving it up for good. One comment I often hear when I offer budget help is that it’s so hard to reduce household expenses without feeling guilty. This guilt often leads to even more debt being created because of letting people down, including themselves.

The provider(s) may feel they are not good enough to support their family which creates inner turmoil and struggles. No one wants to say you have to give something up, especially to a child. Anyone who has direct access to money or that is affected by the money will feel loss when something has to be chopped.

A reader asked me how to deal with guilt while I was assisting them behind the scenes with their monthly budget. I know she will read this but now she’s in a better place and has her budget under control and her family is on board.

Guilty or not guilty

How do you deal with financial guilt? You don’t- You jump over it and move on. You need to keep things under control and by doing so you’ll gain support by the very people the money shelters. You’ll be proud of the strength it takes to move from darkness into light with an outlook.

Stay focused and you’ll see results. Stay in the hole and you’ll live in it.

Perhaps if we look at lowering household expenses in a more positive light as opposed to a jail sentence then budgets will become easier to handle. Too many people stress themselves out when it comes to using a simple budget because of one thing, balance. The problem is that if you can’t balance something then you either have to take something away or add something to even things out.

Most people don’t want to do either because that means having to find more money or taking away something that they may depend on. Thankfully, there are options available for those people who do set aside current trends to follow through on fixing financial health or to work with a limited income.

A modern example would be the internet. We used to get by without knowing every move that someone took but today we’re obsessed with it. Having access to the world becomes somewhat of an addiction that is hard to break for many people. The thought of going to the library to access free WI-fi or other hot-spots is inconceivable to someone who has home internet or a data plan on their cell phone.

As the case may be the extortionate price of cell phones coupled with high monthly expenses is just as alarmingly met with excuses as access to the internet is.

“I need a phone”

“I don’t have a home phone”

Some people would rather go into debt to hold on to these wonders of the technology world then to let them go temporarily to free themselves from financial harm. These are just two examples however financial guilt may grow deeper when you involve kids or other dependents.

You can’t spend what you don’t have.

When you’ve put your kids in 3 different sports but can hardly pay the bills it’s time for a financial check-up of your household expenses. You may need to pull the plug on piano lessons or you no longer can afford extravagant birthday parties or fun nights shopping at the mall. The emotions all comes back to the budget leader because they are in charge of the money.

How will you handle this?

Debt or Misery

Neither please.

If you’re following a monthly budget for the first time you may start to notice areas that need attention. You then must either reduce household expenses, work more hours or pull money from savings just to get by. If none of these are followed through on then you’ll create debt.

No one REALLY wants to do any of those, myself included. Having debt you struggle to pay back is no fun at all especially at the expense of your health and relationships.

Related: How to make extra money without going crazy.

The favourable part is that you only have to deal with yourself if you’re not in a relationship with joined bank accounts. Even then when you keep your finances separate it can put a strain on one person if the other can’t afford to do the same things as they can. This can weigh heavy on the partner who is paying extra or not getting out and having the fun they want.

Perhaps you are in a relationship or you’re married (with or without children). There is more at stake then just your emotions when it comes to chopping household expenses. If you’re in charge of the household expenses and you give then take away perhaps explaining the reasons why will be helpful.

I’m sure if Mrs. CBB came to me and said my $50 allowance was being axed I’d want to know why (and cry a little). I’m used to having that monthly spending money and without a clear explanation I’d become bitter.

When money is tight emotions can run high which only escalates the problem. Set aside emotions to focus on the task and you’ll not only learn more information about your spending habits but you’ll have a clear picture of what you need to do.

For example, if you are unable to pay for your children to join 3 sports this year opt to supplement that loss with a family excursion to do or see something new. Road trips, nature trails, waterfalls and so on are often met with excitement because of new surroundings.

If you spend too much money on health and beauty at Shoppers Drug Mart find alternate solutions to lower the expenses, a new beauty provider or go without if possible.

Related: How to collect Optimum Points Fast.

If you can’t stay away from hardware stores or from buying ‘toys’ opt for looking at second-hand purchases before buying new. This will help to lower household expenses but allow you to splurge a bit without feeling deprived.

Related: How to save money buying used stuff

You don’t have to just take something away abruptly that causes financial strain rather find an alternate solution that includes something inexpensive to fill that void. Don’t wait months or years either. Take a day or two to brainstorm ideas before you slash household expenses and then do it.

Spend it or Save it

There are times Mrs. CBB and I find ourselves talking about why we aren’t advancing our budget since we are now debt free. Should we really be so frugal when there is no need, or is there?

My advice and I don’t give it often but don’t ever lose sight of your future path just because you feel ‘comfortable financially’.

With that being said budgeting will always be a part of our family but we won’t feel guilty about lowering household expenses if need be to;

- Save money for a future purchase

- Balance the budget

- Invest in retirement or second-income

- Pay off any new debt we incur

It would be great if knew we would always be debt free BUT that’s not the case, we don’t know. On the other hand we are fortunate that we can safely spend a bit more but with-in reason.

For example, Mrs. CBB purchased a brand new Galaxy Samsung 7 for $500 which would have been a no-no when we had debt. The last new cell phone she purchased was in 1999 from Rogers with a monthly plan. She never upgraded until she bought a used Iphone 4 for $75 off Kijiji.

This is part of that temporarily putting ‘wants’ on hold until the path is clear to splurge a bit. We were still frugal with the purchase as it can cost upwards of $1000 with tax to buy the Samsung 7 new (less now as Samsung 8 will be released).

Lowering household expenses

Don’t beat yourself up if you have slim down your household expenses because what you do today will affect your tomorrow. Always think about alternatives and the way you communicate any financial changes to your family.

Remember unless you teach your kids about the value of money and how it can impact lives they might not understand. There are adults out there that won’t understand and probably never will but if we all just think before we act I’m sure we’d be met with support rather than opposition. This also helps release any stress or guilt felt by those who are in charge of the monthly budget even if that means having a conversation with yourself.

Discussion Question: How do you lower household expenses without feeling guilty? Do you involve everyone who will be directly affected?

Where our money went in March

Hi Everyone,

Can you believe we are already in April? During the month of March Mrs. CBB and I really didn’t get out of the house much at all. Most of our receipts were for gasoline and groceries. Now that the Spring and summer months are upon us we will see more money going towards home maintenance hopefully to get some of these renovations completed.

That’s our month of earning money and spending money.

Mr.CBB

Pick a Free budget that’s right for you

I’m currently offering 2 versions of our budget and the reason behind it is simple. Firstly, read the CBB blog disclaimer because what you do with it is your own business so if you mess it up you need to sort that out.

I have not closed off any cells so you can make all the changes you like to the budget to reflect your lifestyle which is what you asked me for in your emails. (See I do listen and read your comments and emails)

Although I would love to help every single fan with their budget I am unable to do so but I am always willing to answer any emails you send me so don’t be shy.

This was after all meant to be our personal budget and although I would love to customize it for every fan that wants to use it but, I’m afraid I cannot.

I’m not selling this budget or hope to make any money from it so enjoy this free budget and I hope that it works for you as much as it does for us.

Our free budget spreadsheet

You can download the free budget spreadsheets here.

- Budget 1– You can use the pre-existing categories or you can use your own if you wish and you have the option to use projected expenses or not. Please read all notes left around the budget for tips.

- Budget 2– Everything is pre-set so you have to use the pre-defined categories but this budget will generate year-end budget figures where the other one won’t but you must use the categories already in this budget. If you change anything you will mess up the formulas and year-end figures.

- Please read all notes left around the budget for tips.

Test the budget for a few months and see how it goes. Trial and error, remember that.

Our family budget plan

How we budget our monthly expenses?

I often have fans ask me how to budget money on a low-income or they simply have a high debt load and want to kill it like my friend Tony who got rid of over $100,000 worth of debt by using a budget.

CBB fans want to know what we do in order to save so much money and the reply I give is simple>> It’s not about the money it’s about the process involved.

We are both money managers of our finances and with our relationship compatibility we have been able to get to where we are in 2016, debt free.

It doesn’t matter if you are using a cash only budget or you use your debit and credit cards, if your budget doesn’t balance you have budget issues you should check it pronto.

Learning how to be your own money manager is important because no one else will care about your money more than YOU!.

We don’t always save as much money as we would like every month but most importantly we are not going into debt but only because we are budgeting our money. In fact we are currently debt-free including the mortgage which means all we pay for is our monthly bills and expenses.

One of the most important things we did for our personal finances was that we never let the budget deter us from reaching our goals.

Sure we’ve had crap months but we’ve made up for it or we learned from our mistakes just like we should. Budget failure only occurs when you give up on your budget which should not happen as long as you truly want to reach your goals.

We didn’t always earn the income we do today but made do with what we were earning so we didn’t go into debt. That my friends is “living below your means”. The only science to becoming rich!

Sometimes fans email and ask me if living on a budget in Canada is any different from living and budgeting in other countries. To be honest I’m going to say, probably not.

If I still lived in the UK I could use this exact budget spreadsheet to meet all of my needs however the budget needs to be reviewed monthly.

Below are links to the budgeting series which I wrote while designing our excel budget spreadsheet which will give you an idea just how we designed our budget.

I’m not a financial planner/advisor so I can’t tell you how you should budget but I can show you how we budget. I’m just a regular guy just like everyone else; some might call me a budget or numbers nerd.

Learn how to budget with Mr.CBB

Our Budgeting Series

Do you want to learn to budget like we do?

We explain everything we do and more in this mini-series below all about budgeting.

Please take the time to read through our budgeting series plus read Budgeting in the New Year. I hope the information will help stop you from making common budgeting mistakes that I hear of often and that you take something away from the information and apply it to your financial situation.

If you have any questions about what we do with our budget money tracker feel free to email me.

- How We Designed Our Budget Step 1– Gathering All the information

- How We Designed Our Budget Step 2– Budget Categories

- How We Designed Our Budget Step 3– Tracking Receipts

- How We Designed Our Budget Step 4- Note-taking

- How We Designed Our Budget Step 5– 5S Organization

- How We Designed Our Budget Step 6– Who Does What and When?

- How We Designed Our Budget Step 7– Balancing Our Budget

- How We Designed Our Budget Step 8– Knowing our Coupon Savings

- How We Designed Our Budget Step 9– Reading Our Bills

- How We Designed Our Budget Step 10– Projected Expenses

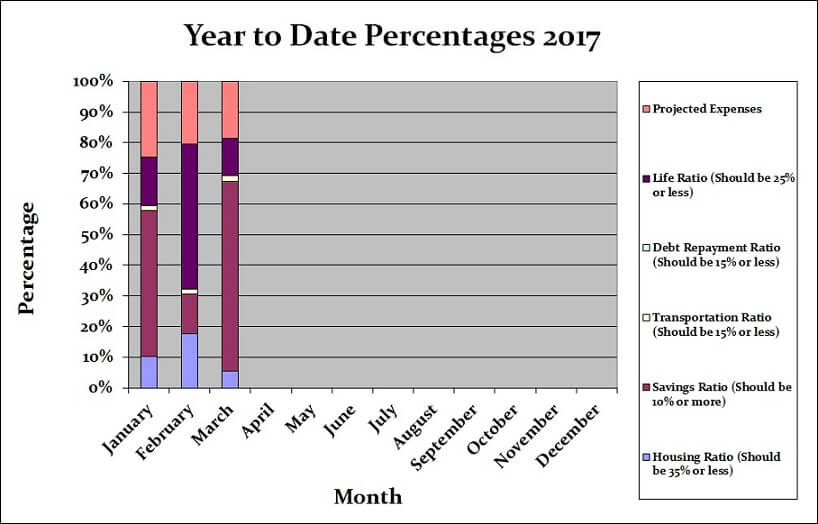

Budget percentages March 2017

Our savings of 62.04% includes savings and investments and emergency savings for this month. If you include the projected expenses savings, we actually saved 80.64% of our income. That’s $8531.81 going into savings or investments of some description or another.

The monthly totals comes to 100% which shows that we accounted for all of our income.

The other categories were well within the defined percentage limits. Our projected expenses this month is at 18.60%.

Budget percentages month by month

Breaking down expenses

This is simply a breakdown of our expenses which has helped us to understand where all of our money goes. Since May 2014 we have been mortgage free so much of our money will be directed at savings, investments and renovations.

I appreciate that you enjoy this budget update each month but I do hope you view this as an educational tool rather than comparing your own financial numbers as our situations are all unique.

Although I encourage your comments and love to hear what you have to say about our budget categories and expenses please don’t tell us to donate our money to charities because we have too much or are fortunate. We are hardly out of the clear with finances for the rest of our lives and have worked and sacrificed to get where we are. We do plan to enjoy the money we’ve saved now since we haven’t over the years with our son.

What we do with our “extra cash” is our business and although we do donate to a charity we won’t be putting it on display for the world to see as it defeats the purpose in my eyes. It is part of the budget as you see it. I hope that clears that up for those of you who had concerns about our extra money.

Just 10 years ago I started working in Canada making a bit over minimum wage and have since moved up the ladder. I’m now working very hard to secure my dream job with one foot in the door. We aren’t all lucky but if you do the best you can at least you can look back and say you gave it a shot.

Sometimes we wish we had more money to budget with but understand that we only have what we earn and if we want more, we need to earn more. Spending less than we earn and budgeting our money has been the easiest way for us to pay down debt and save money.

- Chequing– This is the bank account where all of our debt gets paid from.

- Emergency Savings Account– This is a high-interest savings account.

- Regular Savings Account– This is a savings account that holds our projected expenses.

- Monthly Budgeted Total: $5187.39

- Monthly Net Income Total: $10580.12

- (Check out our Ultimate Grocery Guide to see where our grocery money goes)

- Projected Expenses: These are expenses we know we will pay for throughout the year = $1967.68

- Total Expenses Actually Paid Out: $3290.43

- Total Expenses Actually Paid Out: Calculated is $10580.12 (total net monthly income) – $1,967.68 (projected expenses) – ($5322.01) (emergency savings) = $3290.43

- Actual Cash Savings going into Emergency Savings: Calculated is $10580.12 (total monthly net income) – $3290.43 (actual expenses paid out for the month) – $1967.68 (projected expenses) = $5322.01

How to save for future expenses

What are Projected Expenses? – We project expenses throughout the year so we have the money saved. PE= A projected expense is money automatically saved each month so it is ready when the bill comes in or when you need it as in the example below.

We review our projected expenses at the beginning of the year to set up our yearly budget and adjust as we go along if a new projected expense arises and needs to be added to the budget. Sometimes we remove a projected expense as well so it’s very important to keep an eye on your expenses.

This has happened on many occasions but it’s bound to happen as we can’t predict everything we have to pay for over the course of the year. The important part for us is that we are saving for these expenses and we no longer have to stress about taking money from our savings to pay for them. To learn more about projected expenses read Step 10 in my budgeting series.

When we spend the money in a projected expense category we move that money to our chequing account in order to pay for that incoming expense. So this means the numbers go up and down in the projected expenses account based on what we need to pay for that we saved for in the account over time.

The only thing you need to do is track your projected expenses each month manually as I can’t customize that for you in the excel budget spreadsheet as I don’t know what you will use for projected expenses.

For now we will have to manually track which means month after month we add up what we save in each projected expense category and minus what we spend so we know how much we have and what is left in each category. I have updated our personal excel budget spreadsheet for 2017.

We pay money into the projected expenses account continually throughout the year even when bills come due as its revolving so as one bill gets paid the money continues to come in from the other categories all year-long. This ensures that money is always available. It may not always be enough but having something ready is better than having nothing at all and having to use credit.

So the $1967.68 gets paid into the projected expense account every month no matter what. It seems to be easier to track our money this way but you can do what works best for you.

Example Projected Expense

If our clothing category was a projected expense we would have a budget of $50 per month for the two of us. If we spend $30 on clothes for the month that means we need to pull $30 from the projected expenses account to pay for this expense or we move only $20 to projected expenses for the month and leave the $30 in your chequing account.

It’s up to you how you do it as I mentioned above. My plan is to create a projected expenses spreadsheet to track the expenses all year-long otherwise you need to do it manually which we currently do in order to make sure we don’t overspend what we haven’t saved or will save over the course of the year.

It’s a fairly easy process essentially becoming a lifestyle change for your finances but the most important part is that the money is available and saved, which means potentially less stress.

This means we should have $600.00 per year for clothing to spend. We have to track that expense as we spend it manually but hopefully when I find some time I can incorporate that into our budget spreadsheet so it tallies the numbers up as we go along. That way we will be able to know exactly what we’ve spent as an ongoing total.

Budget Results

Time for the juicy category numbers and to see how we made out with our monthly budget. Below you will see two tables, one is our monthly budget and the other is our actual budget for the month of February 2017. This budget represents 2 adults and a toddler plus our investments.

Budget colours

If highlighted in blue that means it is a projected expense. You will also see our budget does not include the emergency savings as it is factored in at the end.

Budget for March 2017

There will be a few changes to the March budget such as my allowance bumped to $50/month Groceries $265/month, Car Insurance/House Insurance $168.79/month, Investments $1241.66/month, Rogers Telecommunications we’re waiting on a new billing amount.

Actual budget expenses for March 2017

April 2017 Goals

Here are our April 2017 goals along with whether we completed tasks from March 2017.

For the months of April and May we will keep our goals small because of our future plans in June and July coming up quickly. Once we are home for the summer we can tackle a bit more possibly hiring people to come in and get some of the renos started.

- Call around to lawyers to talk about getting a Will written up- Will is in process.

- Start revamping old blog posts: I completed 1 in March.

Finish the master bathroom shower- I will explain more about this later as we’ve had some changes.

- Buy a new blind for the garage- Now that garage season is here I’ll be on the look-out for something to fit the window.

- Finish revamping our sons room- We are almost there but still have plenty to do. Most of what we’ve focused on is selling stuff and organization.

- Start researching vacation spots for 2017- Booked but still looking for a 3 day mini-trip.

- Hang paintings and wrought iron decor on the walls- Waiting for renovations;

- Purge our sons clothes and sell- This is our April and May chore

- Start preparing for our holiday- We’ve mostly just talked about this for now.

- Find some nice friendly personal finance bloggers to guest post while I’m gone- So far we’ve got 3 personal finance bloggers who will be supporting CBB on vacation.

- Start cleaning up the soggy property from April showers-

- Take the winter tires off the vehicle and put the all-season back on-

- Clean out the vehicle and detail the outside-

Budget updates month by month

In case you missed our budget updates and want to do a quick search I’ve compiled them all on one handy page: monthly budgets. For the 2017 Year I will also keep track of each month below and update the monthly budgets page.

That’s all for this month check back at the beginning of May 2017 to see how we made out with our April 2017 budget.

Happy Budgeting CBB’ers!

Don’t Forget To Subscribe To The Blog and Activate Your Subscription!!

- Find me on Social Media by clicking any one of the links below

- Check out my new Free Recipe Index

- If you like FREE then click this link for my FREE Excel Budget Spreadsheet and all my Free Money Saving Lists!

- You can now have full access to my Ultimate Grocery Shopping Guide in Canada.

Wow! I hope one day I can put together a budgeting sheet like this. This is awesome. I’ll have to keep checking in to see your progress. Good luck on your financial journey.

Thanks David for the compliment and for stopping by. Mr.CBB