{kind=link}

Estimated reading time: 12 minutes

New to Canada? Discover how to establish good credit and improve your credit rating for a brighter financial future.

Today, I want to talk about improving your credit rating or credit score and ways you can easily do this.

Build Your Credit Rating With Manageable Adjustments

The great thing about your credit rating is that you can build or rebuild it anytime, especially since our lives can be wonderful in one minute and fall apart in the next.

A few things come to mind when I think of employment, relationships, and newcomers to Canada.

For anyone new to Canada and wanting to understand credit better I’m sharing my experience with you.

Firstly, you need to know that a credit report and a credit score/credit rating are two different things.

Consider your credit report and your report card from elementary school, but the part that explains the marks you were given is a history.

A Credit Score, on the other hand, is the actual mark you get or score; in this case, it is three numbers long. (see photo below)

Since it’s the beginning of 2019 and this is our final net worth post for 2018, I thought we should discuss a credit rating in Canada and how you can improve yours.

Improving your credit rating in Canada boils down to one thing and one thing only: responsible credit use.

Canadian Credit Report Agencies

Two major credit bureaus in Canada are the hub of all things related to your credit rating, Trans Union of Canada and Equifax Canada Co.

Federal and Provincial laws in Canada govern both these credit bureaus, which are allowed to store and maintain credit information on Canadian consumers.

This information is used by those members of the Canadian credit reporting agency who need to find out how reliable YOU are with your money.

According to Equifax, the Canadian credit reporting agency’s leading members are retailers, banks, finance companies, auto leasing companies, and credit card companies.

The above agencies maintain a steadfast relationship with credit reporting agencies and will report how you keep your credit and payment activities.

Other sources of the information contained in your credit report can include public records from courthouses across the country and collection agencies.- Equifax Canada

Trans Union Canada is another great source for finding your credit score and getting your credit report.

Transunion and Equifax

Why Should You Care About Your Credit Report?

There are four types of credit-rating warriors;

- I don’t care about my credit rating or even know what one is.

- I need to improve my credit rating.

- I need to build a credit rating.

- I need to maintain my credit rating.

All four credit rating warriors bring something different to the finance world.

These are all targets of creditors, employers, and lenders, from mortgage companies to rental applications.

Your credit rating is not just any number. It’s an essential number whether you have debt or not.

Just because we are debt-free doesn’t mean we have an immaculate credit rating.

It’s essential to maintain some form of available credit (ex, credit card credit) on your credit report.

They are markers to show lenders that you are reliable when it comes to how you handle your money.

Example Scenario Buying A Bigger Home

What if we plan to sell our house in a few years to buy a bigger house?

This might mean a visit to a mortgage broker or bank for a loan unless we’ve saved up the cash.

Moving up in square footage is never a cheap endeavor, and not everyone has massive amounts of cash sitting in the bank.

Although our mortgage is paid in full, that might not mean anything to the lender if our credit score has tanked because we haven’t maintained it over the years.

Essentially, the lender needs something to evaluate; otherwise, they won’t hand over their money. Would you?

Allowing credit to appear on our credit report, using our credit cards, even if just a little, and paying it off on time shows the creditors that we are reliable.

That’s all they want to see.

Creditors don’t care how much money or little debt you don’t have.

They want to see action, and your credit report is like a bread trail from the minute you allow anyone in a position to obtain your credit report.

You are in control of your credit report, so it’s critical that you access it at least once a year to review what’s on it.

Even simple errors can cause your credit score to dip, and potentially impact your goals.

If you find an error, you must report it to the credit bureau for review and then follow up to ensure it has been taken care of.

Your credit report may show a debt or a bill you were late paying, but you were not late paying it.

It may seem harmless to skip a payment if you are short on cash.

However, any time you don’t pay, it gets documented and follows you like a bad smell.

Once you escalate a review of your credit report, it’s important to view it a second time to review any changes that have happened since.

Trust me, it will be worth it.

What Or Who Needs Access to Your Credit Report?

Not many people give thought to how their credit rating can impact their lives, but it can in significant ways, especially for newcomers to Canada like I was.

Just about anyone who will lend you money or requires a legal credit inquiry will affect not only your credit rating because they are seeking information but also how the information is used.

Are You Reliable?

When your credit history has to be viewed by agencies such as vehicle rental/purchase, credit card applications, landlord applications, employment offers, lenders, and banks, all they want to know is if you are reliable.

Anything such a bankruptcy, home or business foreclosures, secured loans, garnished wages or collections sticks around for a minimum of 6 years.

Inquiries account for 10% of your credit rating, called hard pulls or hard hits, where you might apply for credit or a new credit card.

These inquiries may last up to 3 years on your credit report, also called active seeking.

This means the person may be in financial hardship but not always, but this is still a brutal hit for Canadians.

This means that you will see who accessed your credit report when you read it, and so will everyone else who reads it.

You also must first give consent for an inquiry, so keep that in mind when signing documents or verbally agreeing to the inquiry.

Your credit score does not take into account requests a creditor has made for your credit file or credit score in order to make a pre-approved credit offer, or to review your account with them, nor does it take into account your own request for a copy of your credit history. These are some examples of “soft inquiries” or “soft pulls” of your credit.

– Equifax Canada Co.

If your unpaid bills go to a collection agency, you can bet that will impact your credit rating.

Pay your bills on time.

The term ‘reliable’ holds a heavy grip on our finances, especially when you need something the most.

Oh, and before you think you are let off the hook with a credit proposal or credit counseling that will also stain your credit report for at least 3 years before it goes away.

In all honesty, it makes sense because lenders need to protect themselves, and if your credit rating stinks, you need to work on improving it.

Sounds overwhelming, I know trust me because when I moved to Canada 10 years ago I had no idea how to use Canadian currency let alone what a credit rating was.

These days, my credit report and credit score are over the 660 threshold, which most lenders want to see, so I’m happy with the work I’ve put into building a credit rating in Canada.

Credit Score Chart Canada

What is a good credit score?

The low end of the credit score scale is 300, whereas the higher end is 900. Being somewhere in the middle is ideal, around 660.

How is your credit score calculated?

I’m sure this is a burning question that many Canadians have, even though I had it when I was learning about credit in Canada.

When your credit score is calculated,, a few main factors will be reviewed and impact your credit rating, according to Equifax Canada.

- Number of inquirers into your credit file 10%

- The length of your credit history is 15%

- Public Records 10%

- Used credit vs. Available credit 30% (this is a big one)

- Payment history- 35% (Again, another big impact on your credit score)

You may find different credit scores from various reporting agencies only because they have different ways of scoring you.

Also, lenders typically only go to one credit bureau when looking for info on you.

Simple ways to improve your Credit Rating/Credit Score

- Pay your bills on time and lower your credit balances. Pay off bills that are past due. (FREE printable Debt Repayment Plan)

- Order your credit report, review and correct any errors by reporting them (How to order your Credit Report in Canada for Free)

- Get a secured credit card to build or improve your credit (that’s what I did)

- Use your credit often and pay it but also watch your credit card balances (using too much and not paying it is a no-no)

- Set up automatic payments (this is great, especially if you miss payments by forgetting to pay them)

- Avoid applying for new credit cards for the perks (creditors will look at this as a potential red flag)

- Set up Canada Post mail redirection when you move. If you still request paper bills, change your address online via a portal or call all of your creditors to update your information. This will avoid unpaid bills because they didn’t reach your mailbox, including email addresses and phone numbers.

- Document your bills to know when they should arrive and when to pay them off. If you don’t get a bill in the mail, go online and check. A postal interruption is a good example.

The Bottom Line is RISK

At the end of the day, all creditors want to know is whether you are reliably paying your bills even if your credit rating slightly differs between reporting agencies.

Discussion: What other ways can you improve your credit rating?

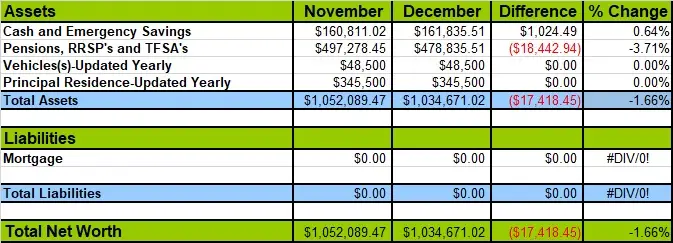

Our Net Worth December 2018

What happened with our portfolio this month?

Just when you thought you were moving up, you get crushed again, and the markets are disappointing again; however, we are not worried.

We may have dropped $17,418.45, but we are confident we will see that rise back up in 2019 and then some.

The year has been kind to us overall, with plenty of financial gains, mostly from our RRSP and TFSA accounts.

We haven’t increased it on the net worth chart above for years, but we can almost double that if we were to sell today.

The reason for that is that we are safe with the way the housing market bounces around.

Ideally, moving to a house on a bigger plot of land in a far less expensive community would be our final destination home.

I don’t know what 2019 will hold for us, but we will see renovations hitting our net worth as I work to get as much as I can do around here.

This is reflected in the savings we have in the bank, which is why it’s still there.

We’re still contemplating swapping our term life insurance policy for something more permanent with investments for the long haul.

If you had $100,000 in the bank what would you invest it in and why?

What would you do with your term life insurance?

Please share your comments below, as I’d like to hear what you say.

Mr. CBB

Understanding Net Worth

What Does Individual Net Worth Mean?

Net Worth is a snapshot of your financial health, like a picture of debt to net assets.

In simple terms, it’s the total value of your assets minus your liabilities.

Your numbers may go up and down, but don’t let the numbers scare you. Rather, understand why and move on.

Calculate Your Net Worth

Do you know how to calculate your own Net Worth?

We like to calculate our monthly net worth to know if we are still on track.

Some people calculate it yearly or quarterly, but it’s up to you and how informed you want to stay regarding your financial health.

Net Worth is only an estimate, and not everyone uses the same type of figures to tally it up.

Some of you may not include vehicles as we do or leave out assets inside the home as we have.

You might be that person who believes that your house should be excluded.

It depends on what you want to calculate or what you can sell today and make money on for tomorrow.

Net Worth is simply adding up all your assets (what you own) and then taking away your liabilities (what you owe), giving you a net worth number.

Understanding your net worth will help you determine if you are on track to meeting or beating your personal financial goals.

Net Worth = Assets – Liabilities

Net Worth Updates 2018

Click the links below to read 2017 net worth updates to see how we made out following our own budgeting and investing rules.

- January 2018

- February 2018

- March 2018

- April 2018

- May 2018

- June 2018

- July 2018

- August 2018

- September 2018 (oops missed this month’s update post)

- September/October 2018

- November 2018

That’s all for this month’s net worth update but please check-in at the beginning of February 2019 to see how we made out in January 2019 with our financial portfolio.

~Mr.CBB

“It’s Not About How Much Money You Make It’s How You Save It“

Don’t forget to Subscribe to CBB and Check out our > Monthly Budget Updates

I hope you can keep up with the updates. I find it quite interesting and I’ve learned a fair bit that will help me manage things down the road. My husbands health isn’t good as you know, we almost lost him last spring, so I’ve been working to be able to handles things alone when the enevitable happens. Plus I have guardianship over my Dads affairs and learning about investing in order to do the best I can for him. Again, eventually, I’ll be in sole charge of those funds after he goes. I’m in no rush, but I’m using this time to learn what I can to manage things better. You are one of the things I’m using to learn.

Awe thanks Christine for your feedback I appreciate that. I don’t know how you do it all as I know you’ve had some challenging years that aren’t getting any easier. Chin up and keep doing what your are doing. There is never a bad time to keep on educating ourselves right? Mr.CBB