{kind=link}

A Financial Emergency Takes Its Toll On Many Canadians

Canadians have been instructed to stay home to stall the spread of the virus plaguing the world but with the health crisis comes a wide-spread financial emergency.

Please note: I’ve left out or removed the name of the virus (we all know what I’m talking about) for SEO purposes with Google.

I don’t think anyone was ready for this even though we’ve been through Severe Acute Respiratory Syndrome (SARS) in 2003 and other virus scares in the past.

Sometimes it’s easier to think it will never happen again and so we let our guards down.

Now we’ve been told to stay home and engage in keeping safe distances away from people which has taken its toll on many Canadians.

Just like personal health your financial health is critical for survival even though we have resources and tools available in Canada.

Living through tough times could take us through depression or recession and having little to no savings and scrambling to feed the family and pay the bills is a nightmare yet reality for many.

The good part is that Canada is supporting and looking after us so we must be proud of the country we live in.

Not every country will be as fortunate.

What is a financial emergency?

From a personal perspective which is what I’d like to discuss today, it’s about not having the means to balance your budget.

By this I mean you have no money saved in the bank for emergencies, you’ve lost your job or have been laid off or health problems have erupted and left you homebound or in hospital.

In this case, it’s obvious.

Although applying for Employment Insurance if you are sick or have the virus having emergency savings makes a big difference.

Service Canada is ready to support Canadians affected by this virus with the following support actions:

The one-week waiting period for EI sickness benefits will be waived for new claimants who are quarantined so they can be paid for the first week of their claim.

Your emergency savings should total at least 6 months to a year which allows you to pay what you need to pay while figuring out your situation.

I’ve said this over and over again over the past 8 years and this is a time where Canadians will really need to withdraw.

Panic Solves Nothing During A Financial Emergency

First of all, there was and still is no need to be hoarding toilet paper and other products in Canada which lit a fire under everyone’s butts.

No pun intended.

This act alone has sent people clearing grocery store shelves leaving many with nothing to buy for their families.

Premier Doug Ford addressed the toilet paper panic hoarding by ensuring that there was no need to buy it all.

Nothing seems to panic people more than going to the grocery store and seeing empty shelves,” he said, adding “I still can’t get my head around this toilet paper situation.”

Ford said he spoke with a local toilet manufacturer and there is plenty of supply.

In our basement cellar, we have toilet paper since we had a stash of 4-roll Majesta packages that we got for free using coupons years ago.

Nothing to brag about as it’s just toilet paper and we had no worries about running out even if we didn’t have it.

We had also just recently gone to Costco and purchased a package of Kirkland toilet paper.

Lessons Learned During This Outbreak

Even so, with so many people around the world contracting the virus and many lives were taken it has taught us some valuable lessons.

- Take Better Care Of Our Health

- Follow Health Warnings with Seriousness

- Save For The Future (Emergency Savings)

- Budget and Spend Less Than We Earn

- Pay Off The Mortgage

- Get Rid Of Debt

- Stockpile Products and Food Throughout The Year

- Monitor Investments Often And Don’t Jump the gun in the face of a stock market crash

- Avoid Listening To Fear Mongers

- Treat People With Kindness

Financial Emergency Preparedness

Over the last week, I’ve been reading Facebook posts, media articles and watching the news on television about Covid-19.

To be honest, it’s been hard to sleep and I’m working to keep Canadians on my social platforms informed as much as possible.

Amidst everything, the province of Ontario is in a state of emergency with Prime Minister Trudeau and Doug Ford urging Canadians abroad to come home.

As businesses, schools, churches and just about all businesses apart from essential services have been closed or limited, a financial emergency is a big topic.

Financial Emergency Examples

Canadians want to know how they will be able to pay the bills especially utilities, groceries, rent, and mortgage.

These are the basic necessities of life and although the province has promised to keep grocery stores, pharmacies and other essentials Canadians still went into panic mode.

Stop The Panic Shopping

As mentioned above there was limited to no toilet paper, wipes, sanitizer, and paper towel to be found in Ontario and across Canada.

Also, the amount of hoarding at grocery stores has left seniors and those with disabilities without the products they need.

Luckily many shops have opened their stores to seniors and those with disabilities to shop first thing in the morning without the masses of people.

Come to the end of the month when child tax benefits arrive many parents who haven’t been able to shop may face product shortages as well.

The good news is that shelves across Canada will slowly stock up again but for those in need now, it’s a rough patch.

It’s not just hitting Canadians hard it’s happening all over the world as this medical emergency sweeps across the land like a fierce tornado.

No one is immune to this virus and the effects have been emotionally frightening for everyone.

Not Everyone Can Stay Home

The front-line workers including all health-care, truck drivers, truck mechanics, car mechanics, and retail staff show up for work praying that they stay safe.

Parents fear for their children who are working at grocery stores, fast-food restaurants, and retail outlets among potentially dealing with a financial emergency at home.

I know I’m probably missing people such as those who work in the media to bring us updates and anyone else who is working hard for Canadians while we stay at home.

With my mother-in-law in long-term care which is on lock-down, we can only see her via Skype but we are thankful none the less.

Sent Home With No Pay From Employer

The hardest part is not knowing what will happen if your employer sends you home without pay.

Not all employers are prepared to pay their employees a wage while they have been instructed by the government to close up shop.

What this means is that these individuals will have to rely on the $82B Emergency Response Package for Canadians and Businesses.

Prime Minister Justin Trudeau has announced a massive $82-billion aid package to help Canadians and businesses cope including income supports, wage subsidies and tax deferrals.

The package includes $27 billion in direct supports and another $55 billion to help business liquidity through tax deferrals.

Canada’s 6 largest banks have stepped up due to economic consequences to help those in need of financial relief with mortgage payment deferrals for up to 6 months and other credit products.

Effective immediately, Bank of Montreal, CIBC, National Bank of Canada, RBC Royal Bank, Scotiabank and TD Bank have made a commitment to work with personal and small business banking customers on a case-by-case basis to provide flexible solutions to help them manage through challenges such as pay disruption due to the virus.

Good news for anyone who has a mortgage through the big 6 or credit card debt, loans or student loans they are unable to pay due to being sent home without pay.

If that’s you just contact your bank and let them know you are in need of help and contact anyone you owe money to but can’t pay to keep them updated.

I remind those that are not being paid and waiting for one of the government aid packages to kick in…contact all of your creditors and discuss you situation so you determine the best course of action available to you. – Mary C. (Facebook)

All of this is fine and dandy but it still doesn’t sit well and shouldn’t for everyone.

What if there was no financial emergency relief?

Ask yourself what you’ve learned from this and how you can better prepare for the next time because there will be a next time.

Support Offered During Virus- Financial Emergency

This is what we currently know so far, but keep in mind that it could change pending updates via the canada.ca website.

Direct Support By Boosting Tax Credits

Emergency Funds:

1. GST credit – $400 single adults – $600 for couples

2. Child Tax benefits Top up – $300 per child added on top of what you receive already.

3. Student loan payments deferred

-6-month timeframe

-no payments

-no interest accrual

4. Indigenous community-based support fund

5. $200 million provided for community resources

-Shelters/homeless needs

-Sexual assault/transition homes

6. 10% wage subsidy for small-medium sized businesses for employees.

-$25,000 per employer

7. Ensured Mortgage Protection Program

-50 billion provided

-payment deferrals

-special payment arrangements

8. Bank Supports

-auto loans – deferral of payments possible

-contact bank directly

-speak to your institutions

9. Personal Income Tax

-payment before September. 1st/2020 – extended deadline for income tax payments owed

-Filing deadline for Income Tax – June.1st/2020

10. Emergency support fund – $5 Billion

-more info to come

*Supply chains from groceries will maintain fair prices for Canadians

Financial Emergency Care Benefit

The Government of Canada says on its website it will start sending $900 every two weeks to some Canadians for up to 15 weeks starting in April (it needs to be passed by the House of Commons and receive royal assent first).

Once it’s available, you will have three ways to apply: through the Canada Revenue Agency website, through a My Services Canada account or by calling a toll free number (that hasn’t been announced yet). – Source

- People who are in isolation or are sick with COVID-19 but do not qualify for employment insurance (EI). This includes the self-employed, such as freelancers.

- Workers, including self-employed, who are unable to work because they are taking care of someone with the virus – but do not qualify for EI.

- Parents who need to take care of kids who are at home due to school closures and aren’t receiving a paycheck from work. The emergency care benefit still applies if such a parent also qualifies for EI.

The Face Of Health and Financial Emergency

I took to my Facebook page of near 10,000 followers to ask them these two questions below.

- Besides the obvious what worries you the most right now with what’s happening in the world? Covid-19

- Has this experience changed the way you will do things in the future?

My biggest worry is that my husband and I can’t isolate even though we want to. Yes, we are making a wage, but my husband works retail and has many people who are in his face throughout each day.

And customers openly admitting they were travelling outside of the country this week and they are shopping despite requirements to isolate no matter what.

People are not taking it seriously enough and it’s going to bring this to my home.

I have less respect for a lot of companies and people around me.

What can I do in the future? About this, nothing.

What are we doing now?

More laundry since I have a laundry station at our front door and we are changing immediately and showering when we each return. – Angela

Due to the amount of panic that has gone on we are now trying to buy items ahead.

Even though it may be weeks before we need them.

We aren’t excessively buying any one item at a time.

This definitely was an eye-opener to how crazy people have gotten. – Michelle

I always keep a well-stocked pantry, medicine cabinet and cleaning supply cabinet so I didn’t rush around like a lunatic buying everything in sight.

As I open the second to last item of anything I start looking for a sale to get an extra one or two.

The TP craze is mind-blowing! I have used an outhouse complete with magazines and catalogues before my Grandma had indoor plumbing.

Also I remember Mom having a diaper pail in the bathroom with diapers soaking in bleach until she did a load of laundry.

We all have the ability to use one of these two old-time methods if we have to. I know I certainly have a pail, old towels, and bleach!- Mary

I’ve been prepared food wise but not enough medically. Have a thermometer but no covers for it. – Karen

Response below to Karen from Mary with some good advice.

Karen, I know…I am a little medically light too except I do have the 12 prescriptions that I am on daily.

I plan to get a 2nd thermometer somewhere along the way so that we each have one to use and don’t have to fuss about having to share one.

That’s just for somewhere down the line.

For now, at least I have one.

Treating people with kindness

I’m offering to deliver to those in complete isolation in my area. Delivered a few dozen eggs yesterday, looking for hand san/wipes for someone who is immune-compromised and who can’t stay home all the time.

Even my secret store no longer has any. – Faith

Societal Reset

I hope the current situation is a blip, a reset for our society. Time to really rethink our way of life.

Some of us are lucky, have some resources, have the ability to cook and maintain their household.

I’m not going to shop on Friday, I’m back to work in my store after a week of bereavement leave.

- I now use the top of a pen to punch PIN numbers into a PIN pad.

- Depositing cheques through mobile banking.

- I wear gloves while shopping and carry a small amount of hand sanitizer in my car to rub as soon as I’m back to it.– Anne

Being Prepared but with health fears

I feel very fortunate that hubby and I are now both working from home.

My biggest fear is for the next time I have to see my doctor for a prescription renewal but that’s not until May.

I am a 60+ person with multiple immunity issues and just want to get thru this crisis alive until a vaccine is available.

I am extremely grateful I have a very happy marriage with someone that I enjoy self isolating with! LOL 🙂 Things I would do differently?

Not really but we’ll see if I change my mind about that when the financial dust settles and the markets quit crashing.

For now, we have enough and I am grateful.

I love the fact that we have a stationary bike in the games room and a set of stairs in the house so we can continue to get exercise within our home.

Should I even own up to the fact that I have some dance dvds that I can groove along to? Not a pretty mental picture huh? – Mary

In Summary – Financial Emergency Preparedness

Next to this world-wide health crisis we must fear financial emergencies at all times and get a financial plan in order.

Budgeting must be a priority even if you don’t think it will help you, it will but only if you commit to it.

If you have yet to start an emergency savings account, please do so even if you only save $5 a week.

Can’t find $5, well then start chopping unnecessary services and buy less, use coupons, cashback services, and coupon apps.

An even bolder approach would be to sell your house if your mortgage relies on two incomes and buy something smaller.

If you rent and your budget are so tight that you hardly get by try considering looking for something more affordable.

Do whatever you need to do (legally) to find money in your budget to save for an emergency situation.

I urge everyone to read the World Health Organization website for the most updated and accurate information.

Please note: I’ve left out or removed the name of the virus (we all know what I’m talking about) for SEO purposes with Google.

Discussion: Besides the obvious what worries you the most right now with what’s happening in the world? Covid-19 Has this experience changed the way you will do things in the future?

Share your comments below.

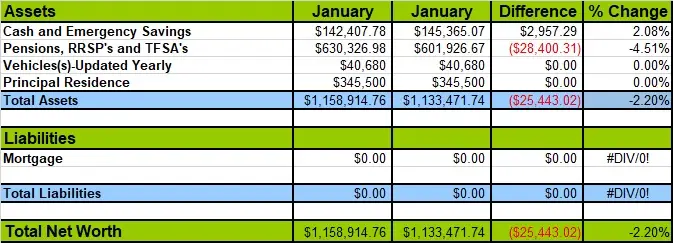

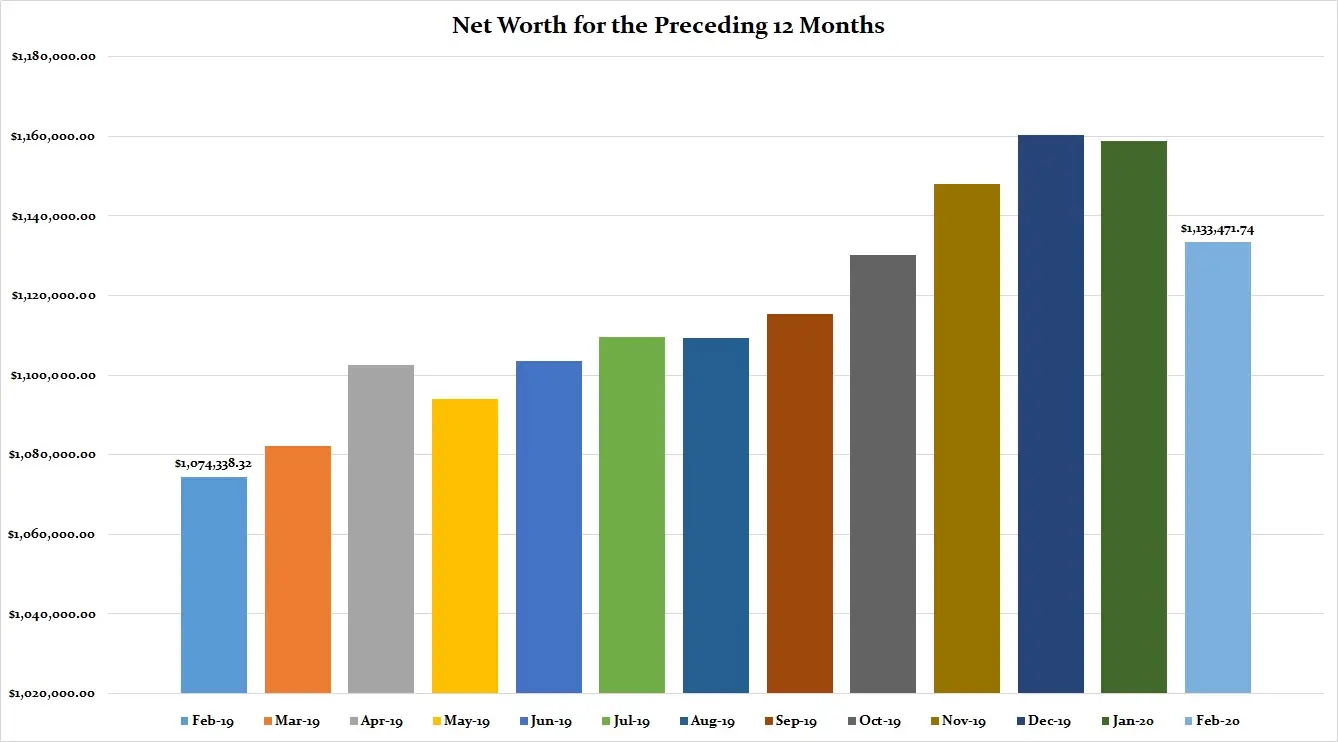

Net Worth Losses and Gains

February 2020

What happened to our money in February?

Besides the obvious market crash with the coronavirus, there’s not much more to say than our net worth has gone down even further since I took these figures.

This was our financial emergency however we aren’t panicking as we know things will get worse before they get better.

This is another good reason why you don’t want to put your eggs in one basket and why we paid our mortgage off first.

I’ve always said your mortgage is a sure-thing and investments can go up or down.

That’s my personal opinion but for those that have followed me for years you know, we took the balanced approach to retirement investing and mortgage paydown.

We also dropped some cash on Mrs. CBB to get laser hair removal surgery done and purchased a new washer and dryer.

Combined they both ran us about $3000 which was fine since we have the savings.

Let’s hope for a better tomorrow for everyone around the world.

Look after yourself,

Mr.CBB

Understanding Net Worth

What Does Individual Net Worth Mean?

Net Worth is a snapshot of your financial health sort of like a picture or debt to net assets.

In simple terms, it’s a total of the value of your assets minus your liabilities.

We credit the growth of our net worth due to patience, perseverance, using a monthly budget and not giving up.

Your numbers may go up and down but don’t let the numbers scare you rather understand why and move on.

If you would like to use our budget I offer a FREE downloadable budget which I created and that you can use at home just like we do.

I don’t charge for it because I want you to save money not spend more!

There are tonnes of other free resources at Canadian Budget Binder to help you build your net worth.

Calculate Your Net Worth

Do you know how to calculate your own Net Worth?

We like to calculate our net worth every month so we know if we are still on track.

Some people calculate it yearly or quarterly but it’s up to you and how informed you want to stay.

Net Worth is only an estimate and not everyone uses the same type of figures to tally it up.

Some of you may not include vehicles like we do or leave out assets inside the home as we have.

You might be that person that believes that your house should be excluded.

It depends on what you want to calculate or what you can sell today and make money on for tomorrow.

Figuring out net worth is fairly easy as long as you know your numbers or monthly finances which means you need to do your homework.

Net Worth is simply adding up all your assets (what you own) then taking away your liabilities (what you owe) which will give you a net worth number.

Understanding your net worth will help you determine if you are on track meeting or beating your personal financial goals.

It doesn’t get any easier than that.

Determining Net Worth

Net Worth = Assets – Liabilities

Why not go ahead and calculate your own using our Free Money saving Tool Net worth Calculator (Canadian Budget Binder 2012)

Financial Numbers

When budgeting anything is possible, we are proof of that although we still have a long way to go in our journey.

These are our numbers and our goals, not a means of comparison towards your own goals to others’ target goals.

We don’t care how much money others make or if they have a high net worth or if it is lower than ours as it’s not a competition.

I hope our experiences will help guide you along your financial path working towards debt freedom.

Not everyone has the same path in life.

Some of you may have had to start over like I did or go to school a second time and now have OSAP loans to pay back.

Others may have divorced, lost money in the stock market or other investments, suffered job loss, fell ill or injured on the job and so on but you can’t let that stop you from achieving your financial goals.

Some of you may have been given trust funds, paid-for homes, paid educations or perks in life that give you a financial kick-start and that’s OK too.

Earn It, Save It, Invest It, Build It

Remember what I said, “It’s not about how much money you make, it’s how you save it”.

The only reason people accumulate wealth is that they know how to save or invest it wisely even if they did inherit money or win the lottery.

The smallest improvements should mean big strides in working towards reaching your goals.

Sometimes we have to fail to learn and we’ve all been there.

Money can be an evil force for some people especially those who have a negative attitude towards their financial situation.

I urge you to be optimistic and little by little with determination you too should see improvements if you want that to happen.

Canadian Budget Binder Net Worth Updates 2020

Click the links below to read our net worth updates for the year.

That’s all for this month’s net worth update but please check in the middle of April 2020 to see how we made out in March 2020 with our financial portfolio.

~Mr.CBB

The net worth for your previous 12 months chart is hard to look at. I hate seeing the drop but on the plus side…there’s still a pretty significant bar remaining for Feb. 2020!

I do our net worth quarterly and I am really not looking forward to preparing my March 31st statement. It will be sad compared to the December statement. Once again, my love of government guaranteed Fixed Income vehicles will help us ride out this firestorm. In recent months, I had a broker’s assistant criticize my choice to go long on our laddered maturities…saying the short term rates were nearly as good. Who is laughing all the way to the bank now? Have you looked at the current rates? They are only going to get worse!

I have been thru several recessions but never a full on depression. This could well be the one but I sure hope not! I am getting far too close to retirement to recover from this stuff. I always stay on top of our assets though and make sure that anything we have invested is fully covered by CDIC and the Canadian Investor Protection Fund (CIPF) insurance. People have laughed along the way at my near obsessive tracking of our assets to make sure that they are as secure as they can be and that I minimize our risk by making sure that I don’t have all my eggs in one basket.

Although we do have an Emergency Account, we’ll see if it’s enough to ride this out. For now I am erring on the side of caution and eliminating any expense that I possibly can. Seeing the branch of my credit union close effective today tells me this could be a rather wild ride and that perhaps I need to hang onto every scrap of cash that I can as if my life depends on it!

Hi Mary,

Tell me about it. We don’t want to look at it either but we’re not the only ones in this position. I was talking to my dad today and was wondering if now was the time to buy. I still have 20 years before I retire so I’m keeping my spirits up on this one but for someone close to retirement this is not good.

I don’t blame you for being meticulous with your investments, heck if I knew half as much as you I’d be doing my own as well.

Sometimes I think people invest more in worrying about what other people are doing rather than worrying about their own backyard if you know what I mean.

So many people are crying for help now financially and like we’ve been saying all along, save your money, spend less than you earn, find new income sources. It’s not until we face these ordeals head-on that people WISH they had done things differently. I hope this is an eye-opener for many Canadians.

Thanks for your feedback and never stop tracking your money… it’s your life, right?