{kind=link}

Estimated reading time: 13 minutes

To increase wealth in our 40s, we’ve learned a few ways to change our lifestyle and investments to achieve our overall goals.

Your 40’s Is The Time To Ramp Up Your Financial Goals

If you want to increase wealth, you have to plan, and your 40s is the home stretch before life settles down.

Leaving a legacy for our son is part of our retirement plan and making sure our lives are comfortable.

I’ve been told that by age 45, we should have saved at least three times our yearly income in savings.

Thankfully, we are on track, but it has taken discipline and finding ways to earn income above net pay from my employer.

Even if you are in your 40s and haven’t been working to increase wealth in your 20s and 30s, there’s no better time to start than now.

Emergency Fund

YES, you need one, and no, you don’t need a year’s worth of savings, but it’s nice to have for that extra padding of comfort.

You should save 3 to 6 months of your net income in a savings account or Tax-Free Savings Account for emergencies.

You may not see the urgency now, but you will thank yourself in the future for going the extra mile to save.

Estate Plan and Legal Will

If you’re in your 40s and still don’t have a Legal Will, I’d suggest getting one, especially if you have dependents.

We didn’t go frugal with our legal will and hired a top lawyer in town to ensure we didn’t miss a thing.

Our complete legal will cost us $1000, but it’s worth it to help our son figure things out when we are gone.

By not having a will it can cause complications that will end up costing your estate money.

Leave your life hassle-free for the person dealing with your death, as it’s already a time of sadness for them.

Ways To Increase Wealth In Your 40’s

You’ve been working hard up until your 40s and know that you’ll be retiring in approximately 25 years or less (or more).

To increase wealth during our 40s, we’ve learned that we need to change how we spend, earn, and invest our money.

Budgeting In Your 40’s

A budget will forever be on our list of financial tools that we must use to help us increase wealth.

Anyone who uses a budget will notice that year over year, there will be changes.

Sometimes for the good and other times not so good.

The game ensures you can balance your budget and incorporate savings and investments while paying off debt.

Even though you may think that saving a few dollars here and there is nothing, it will be something.

Passive Income

There are many types of passive income streams where you can earn money while you sleep.

In 2012, I started a blog and learned I could monetize years later.

That meant I wasted passive earning potential due to a lack of knowledge.

Now that I know better, I’ve monetized CBB over the past five years and earned a 5-figure income from this blog.

As I have a full-time job, I’m limited in the amount of time I spend on the blog, although I’m considering outsourcing help.

However, some full-time bloggers earn hundreds of thousands and even millions of dollars in passive income per year.

We’ve also rented a room to students and taken in international students for a month for cash.

If you have space in your house, this may be something you want to consider to earn extra cash on the side.

Another popular passive income stream is renting a parking space or garage on your property for a monthly fee.

If real estate investing intrigues you, buying a rental is a powerful way to pay off a mortgage using someone else’s money.

Remember that owning a rental home comes with headaches, but it’s money in your pocket if you’re up for the challenge.

- Start a blog or other hobby that you can monetize

- Purchase rental real estate

- Rent a room

- Parking space rental

Maybe another day, I’ll dive deeper into passive income streams to explore how many ways we can all increase wealth.

Reduce Spending To Increase Wealth

As we age, it will be apparent that you don’t need as much stuff as you thought.

In your 40s, slim down the stuff you own so it’s less work as you age.

Also, it’s a significant burden to leave on your children or power of attorney when your home is filled with stuff.

Also, during your 40s and into your 50s, reduce spending to increase wealth for future endeavors.

Watching where your dollars are going is far easier to save, especially when you limit buying what is unnecessary.

A spending plan or budget will help you reduce spending and set monthly goals.

Life Insurance

Life insurance is a must; if you don’t have it, consider your body worth nothing if you financially die.

You can incorporate life insurance into your budget in many ways, starting with Term or Whole Life Insurance.

Related: Life Insurance To Fund Your Retirement

Related: Should you buy term life insurance or mortgage life insurance?

Permanent Life Insurance

We transitioned from term life insurance at the beginning of 2020 to a permanent life insurance plan.

Permanent insurance can be desirable to those with discretionary cash flow, especially the tax-free accumulation of cash values.

Converting policies to permanent plans makes sense for several reasons:

- Estate Planning: Your life insurance is guaranteed to be paid out at some point in time in the future (tax-free), whereas term insurance will terminate at age 80

- Long-term cost: Converting your term life insurance now will avoid costly, unaffordable increases in premiums at the renewal points

- Medical Reasons: If your health is compromised and you no longer qualify for standard life insurance, converting your term insurance to a permanent plan will ensure your coverage remains in place for life

- Investment Diversification: Some permanent policies feature the ability to accumulate tax-free cash values. The growth rate of these cash values is similar to fixed income (bonds) investments, except that you can never have negative returns. That’s why some investors diversify their investment portfolio (generally allocated to bonds) to tax-free, positive-return permanent life insurance policies.

Critical Illness and disability insurance are two other insurance products you should consider, especially if you are the breadwinner in your home.

If something happens to your health or you sustain some form of disability, at least you will be covered.

It’s always best to be safe than sorry.

Debt Reduction Plan

In your 40s, you should better understand personal finance, especially if you’ve budgeted and saved money.

During your 40s, you may likely have a mortgage, vehicle loan, school loan, and other debts, as it’s not uncommon.

The main focus here is that you have a solid debt reduction plan to pay off these debts as quickly as possible.

You should also consider eliminating any further debt while paying off what you already owe.

During the ’40s, couples sold to buy a forever home with a larger mortgage or downsized based on future goals.

Consider how the increase in mortgage payments ties into your retirement goals and whether they are necessary.

Often, we think we need a bigger house when all we need is to enjoy what we already have.

If you plan on using the equity in your home to fund retirement, keep in mind you’ll need to sell.

This also means you’ll need to relocate, which could cost you more.

Ramp Up Retirement Investments

Many people contribute something to their retirement savings but have no idea what is happening.

You do not want to settle with the set-it-and-forget-it mindset when it comes to your golden years.

Once you hit 40 years old, it seems like retirement is around the corner. At least, it did for us.

We started discussing how we could increase wealth using other financial products.

This is the time to focus on maxing out your retirement portfolio, including that of your employer, if available.

Ideally, save 15% (or more) of your before-tax income into retirement savings.

Once you max out your retirement funds, turn to non-registered investments that continue to increase your wealth.

To do this, we had a full financial analysis completed by our financial advisor with Manulife Canada.

We learned we were on track to meet our retirement goals, including fully funding our son’s education.

As happy as we were, there are always possibilities of market volatility, as we’ve just recently seen during COVID-19.

You must meet with your advisor to review your retirement portfolio, especially if you are near retirement.

Your financial advisor should explain what is happening with your portfolio and any suggestions for changes.

New Career or Wage Increase

Professional growth is somewhat like graduation through the ranks of your career, which may also include a wage increase.

Even if you aren’t cascading up, ask your employer for a wage increase if they are not implementing one.

In your 40s, you’ve settled on a career you like; however, some people change jobs or even return to school.

Whatever your financial and personal goals are, it’s essential to balance what you love and what fits your lifestyle.

Overall, we feel we’ve been doing a decent job with our finances to increase wealth in our 40s even though we’ve seen a slight decline since Covid-19.

The moral of this story is that no matter what we do, there is always the possibility of something going wrong.

Be prepared with a backup financial plan and plan the best you can to protect yourself and your assets.

Discussion: What steps are you taking in your 40s to increase wealth?

Please share them below.

Mr.CBB

Net Worth Losses and Gains

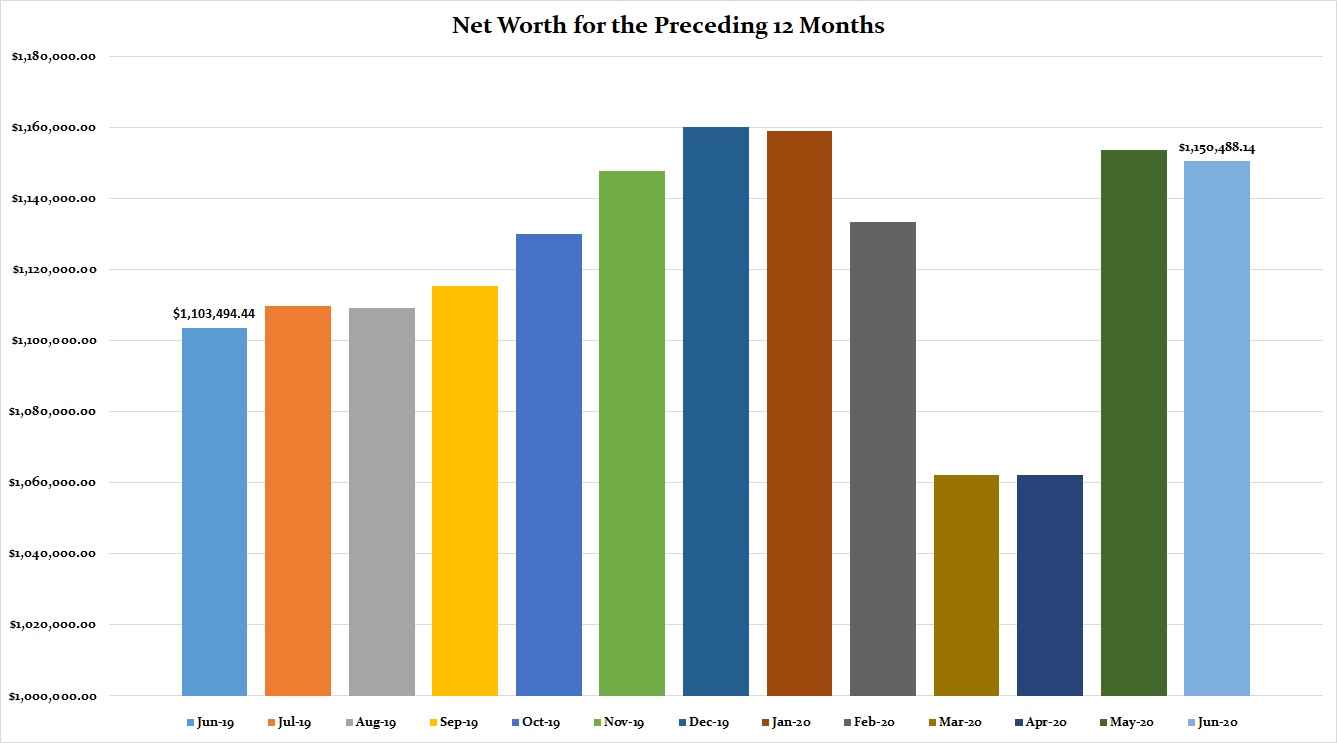

June 2020

What happened to our money in June?

Well, there wasn’t any one thing to blame this time for such a dismal net worth result.

Our vehicle had an unexpectedly high maintenance cost, yet nothing was fixed.

It was just routine maintenance that needed to be done to keep the warranty on the vehicle.

I feel more like I got done instead.

Additional expenses went to, or should I say, ongoing costs to the basement project in the house, which is almost near inspection (yes, it’s being done by the book).

Then, there are the unexpected house maintenance costs due to unforeseen circumstances.

Do you know when you open something to renovate and find another problem, well that’s what happened?

Finally, Mrs. CBB got a little carried away with clothing sales, although the long-term savings will be worth it.

Why not when new clothes are cheaper than second-hand?

That’s all for this month.

Let’s hope next month is a positive month.

P.S.- A house similar to ours on our street sold last week for $749,000.

Mr.CBB

Understanding Net Worth

What Does Individual Net Worth Mean?

Net Worth is a snapshot of your financial health, like a picture of debt to net assets.

In simple terms, it’s a total of the value of your assets minus your liabilities.

We credit our net worth growth due to patience, perseverance, using a monthly budget, and not giving up.

Your numbers may go up and down, but don’t let the numbers scare you. Instead, understand why and move on.

If you would like to use our budget, I offer a FREE downloadable budget that I created and that you can use.

I don’t charge for it because I want you to save money, not spend more!

There are many other free resources at Canadian Budget Binder to help you build your net worth.

Calculate Your Net Worth

Do you know how to calculate your own Net Worth?

We like calculating our monthly net worth to know if we are still on track.

Some people calculate it yearly or quarterly, but it’s up to you and how informed you want to stay.

Net Worth is only an estimate, and not everyone uses the same type of figures to tally it up.

Some of you may not include vehicles as we do or leave out assets inside the home as we have.

You might be that person who believes that your house should be excluded.

It depends on what you want to calculate or what you can sell today and make money for tomorrow.

Determining your net worth is relatively easy as long as you know your monthly financial numbers.

Net Worth is adding up all your assets (what you own) and then taking away your liabilities (what you owe), giving you a net worth number.

Understanding your net worth will help you determine if you are on track to meeting or beating your personal financial goals.

It doesn’t get any easier than that.

Determining Net Worth

Net Worth = Assets – Liabilities

Why not go ahead and calculate your own using our Free Money Saving Tool, Net Worth Calculator (Canadian Budget Binder 2012)

Financial Numbers

When budgeting, anything is possible; we are proof of that, although we still have a long way to go in our journey.

These are our numbers and our goals, not a means of comparison towards your own goals and others’ target goals.

We don’t care how much money others earn if they have a high net worth or lower than ours, as it’s not a competition.

I hope our experiences will help guide you along your financial path, working towards debt freedom.

Not everyone has the same path in life.

Some of you may have had to start over like I did or go to school again and now have OSAP loans to pay back.

Others may have divorced, lost money in the stock market or other investments, suffered job loss, fell ill, or injured, but you can’t let that stop you from achieving your financial goals.

You may have been given trust funds, paid-for homes, education, or other perks that give you a financial kick-start, and that’s OK, too.

Earn It, Save It, Invest It, Build It

Remember what I said, “It’s not about how much money you make; it’s how you save it.”

Some people accumulate wealth because they know how to save or invest, even if it is inherited or a lottery win.

The most minor improvements should mean significant strides in working towards reaching your goals.

Sometimes, we have to fail to learn, and we’ve all been there.

Money can be evil for some people, especially those with a negative attitude towards their financial situation.

Be optimistic and with determination; little by little, you should see improvements if you want that to happen.

Canadian Budget Binder Net Worth Updates 2020

Click the links below to read our net worth updates for the year.

- January 2020 Net Worth Update

- February 2020 Net Worth Update

- March 2020 Net Worth Update

- April- Oops, I forgot

- May 2020 Net Worth Update

That’s all for this month’s net worth update, but please check in the middle of August 2020 to see how we made out in July 2020 with our financial portfolio.

~Mr.CBB