{kind=link}

UNDERSTANDING YOUR EXPENSES WILL BETTER YOUR BUDGET SUCCESS

When creating your budget spreadsheet there are critical expenses that you always want to account for.

Unfortunately, your budget will never consist of exclusive controllable expenses because we don’t dictate costs for everything we own.

A reader wanted to share her experience with a family member and how she explained to her mother-in-law that the costs of owning her home are expensive.

She wasn’t understanding that there were more expenses other than her $800 allowance and utility bills.

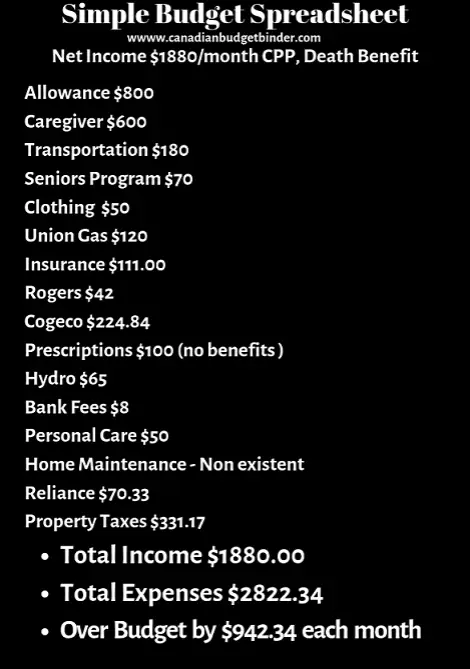

To help the reader we created a simple budget spreadsheet breakdown so she would understand there was more money being spent then there was eaned.

Sometimes asking for help from another source is easier to explain to a friend or family member who you think needs financial education.

In fact, the amount totalled close to $1000 and now we have to work on scaling back or eventually selling the house.

Let’s have a look at her simple budget spreadsheet, however keep in mind that her allowance takes care of her groceries and what she buys.

Like many people, she will be using the equity in her home for retirement savings which we are at least blessed that she has.

Like many people, she will be using the equity in her home for retirement savings which we are at least blessed that she has.

Her house was paid in full with a pension payout so that is one financial stress off her shoulders.

She has around 3 years left of savings until she runs dry and the $1000 overage will crush her budget.

Where the problem arises is that she sees her house as a goldmine of money if she sells and believes she will be fine financially.

She may well be but on a basic level which means there’s no going on holidays and her budget will be very tight.

She’s not alone as many homeowners and renters aren’t thinking about everything they need to cover when they create a budget spreadsheet.

Honestly, you can add whatever budget categories you want to make your budget look good but whether it balances correctly at the end of the month or year is another story.

Budget Spreadsheet Expenses

When looking at your budget spreadsheet expenses there are 4 expenses situations to consider.

Daily Expenses

- Daily expenses are those that you spend each day. These may include day to day expenses such as your morning coffee, lunch, parking or anything else you pay for daily.

Weekly Expenses

- Weekly expenses are those that you spend once a week. These types of expenses may be gas for your vehicle, car wash, groceries, and even weekly rent or mortgage payments.

Monthly Expenses

- Monthly expenses are those costs that you pay for once on a monthly basis. These types of expenses could be property taxes, mortgage, rent, groceries, utilities, etc.

Yearly Expenses

- Yearly expenses are those that you pay for once a year. These expenses may include home maintenance, vehicle maintenance, license renewals, sports tickets, etc.

When it comes to the above 4 expenses that most people experience throughout the year it’s important to break them down further into budget spreadsheet categories.

Related: How many budget categories should I have?

Now, this is where lots of people go wrong with their budget especially if they are looking to get a detailed summary of their financial expenses.

If you’re someone who wants to do the least amount of work with a budget then you may not care to include these expense categories on your budget spreadsheet.

I highly recommend doing a throughout financial analysis each month if you are deep in debt or trying to build credit in Canada.

Understanding Budget Spreadsheet Fixed and Variable Expenses

What are considered expenses?

What are considered expenses?

Any time you have to reach into your pocket, bank account or investments for the money you have an expense.

Expenses can result from anything from food to housing and each fall under different expense categories as I discuss below.

So for example, your budge is a snapshot of income vs. expenses.

Money coming in vs. Money going out.

1. Fixed Expenses

Fixed expenses are those that you can’t control because the amount is dictated by those providing the service.

Some examples of fixed expenses would be;

- Mortgage or Rent

- Loans

- Utility Bills

- Insurance

- Property Taxes

2. Variable Expenses

Variable expenses are those costs in your budget that go up and down and all around each month. You often won’t pay the same amount on a daily, monthly, weekly or yearly basis.

These are what some people like to call controllable expenses or flexible expenses since you have more control over how much you spend.

Some examples of variable expenses would be;

Miscellaneous Expenses

Each year we end up with miscellaneous expenses on our budget spreadsheet which happens because we didn’t expect them or they didn’t have a budget category set up for them.

You WILL NEVER have a perfect BUDGET and where you chose to put your “extra expenses” is up to you.

I’ve had one reader complain about our miscellaneous category and the amount of money we have spent over the years.

My response is that this is the way we designed our budget where we take what we can’t control and funnel it back into the budget the following year.

In other words, it becomes an added expense that we know might pop up so we budget for it. If we use it we use it if we don’t we have spare cash kicking around.

For example, We bought my mother-in-law 2 jackets and 3 pairs of shoes from Value Village which wasn’t a budgeted expense for us.

We’ve noticed that we spend money on her when we visit since she is alone now and we like to take her out shopping or to eat.

These expenses come out of our pocket and have not been designated so they go to our miscellaneous category which is also a projected expense for us.

Moving forward for 2020 we will allow these expenses in our budget and add them to either a gifts category, mother-in-law expenses or increase our clothing allowance.

How you designate your miscellaneous expenses is up to you but I can promise you that every year you will have them which is why collecting receipts and taking notes is so important.

Projected Expenses

Projected expenses are those that you know you will have to pay for at some point during the year so you save for them on a monthly basis in a spending account.

We have our projected expenses bank account with Simplii Financial and we use the money as needed throughout the year to pay for bills.

Projected Expenses Example:

Once a year $500 payment for parking fees at work payable in January.

500/12= $41.66 each month to be saved as an ongoing projected expense.

When the bill comes due you pay the money and continue to save the same amount all year.

Not all projected expenses will be paid up in your account on time and many will overlap.

This means money will be coming and going however it’s critical to make sure you have enough to cover the expenses or base your monthly savings calculations on the payment date.

The best part is how we no longer have stress about using our emergency savings for stuff we should be saving for.

Emergency Savings

I know lots of people like to cram everything not listed on their budget spreadsheet into the emergency savings category but it’s not something I suggest.

Ideally, your emergency savings are meant for emergencies like you need a hotel room for the night or your basement flooded.

Until any insurance money comes in it’s nice to have a financial cushion set aside.

I suggest saving 3-6 months of your monthly budget expenses for a rainy day.

So, if your monthly budget expenses total $5000 then you should save 3 to 6 times that amount or $15,000-$30,000.

Stop thinking that an emergency savings account is an account to pick up the tab for expenses that should be directed elsewhere on your budget spreadsheet.

Car Maintenence Expenses

This is one I hear about ALL the time.

- My car broke down.

- I can’t afford to fix it.

- Insurance deductible is too high.

The reality is that when you own a vehicle like a house you must pay costs to maintain it.

That means scheduled oil changes, fluid changes, tire rotations, new tires, brake job and so forth.

If you can’t afford your deductible or any basic car maintenance expenses then perhaps taking a cheaper form of transportation might suit your budget.

Oh, and before you buy a car tap into the costs of repairs and spare parts.

Just because you found a bargain on BMW doesn’t mean you can afford the upkeep.

Healthcare Expenses

Not all health and medical expenses are covered in Canada even if you have a Health plan through your employer.

The readers mother does not qualify for Trillum until her back income tax reports are completed as she missed two years.

Until then she is paying out of pocket for her medical expenses in full which means $100 every month or $1200 a year.

This is only for 3 medications but for some who take many more, the expenses can skyrocket.

If you are not covered by a health care plan for prescriptions then consider it part of your budget.

You can, however, claim Canada income tax medical expenses when you do your tax return but there is a minimum limit of $2302.

You can claim either 3% of your net income or $2302. In other words you will have to have medical expenses above $2302 to make any impact to your income tax return.

Dental expenses are so high for many Canadians that they choose not to go for regular check-ups unless they have health benefits.

Even then your health benefits plan may not cover the full amount of the visit which leaves you with budget expenses you must pay.

Braces are a huge expense and even with benefits, most benefits companies will only cover up to $2500 once in a lifetime.

It’s great if both partners have benefits to combine but even then you will still be paying money out-of-pocket.

Eye Care, for the most part, is not overly pricey and you can find glasses at bargain prices all over the price.

It’s when you don’t have health benefits to cover your eye exam or the expenses to buy new glasses where you must be prepared financially.

Also, if you desire designer glasses they come at a premium price as we found out last month.

Even though my benefits cover each of us for $400 every two years to get eyeglasses Mrs. CBB picked a pair out that totalled $650.

That meant we would end up paying $250 above our benefits coverage.

If you’re lucky some opticians will bill your benefits company by splitting the costs between people so all of the expenses or at least most get covered.

Never bet on it though or choose glasses that fit your health budget.

Don’t worry Mrs. CBB didn’t buy those designer eyeglasses and I didn’t get my Gucci specs either.

Home Maintenance

Home repairs are almost always underestimated or overlooked when creating a budget spreadsheet.

Your budget spreadsheet is like a daily expenses app where you input what you’ve spent for the day with the receipts you’ve collected.

Home maintenance savings should be at least save 1 to 3 % of your home’s purchase price on a yearly basis.

If for example, you paid $200,000 for your home you will need to save $2000 a year at 1%.

We do this as a projected expense.

Budget Right The First Time

There are enough free advice and blog articles by budget professionals online to teach you about budgeting.

When you fail at a budget category figure out why and work on improving what expenses you can control.

Discussion: What budget spreadsheet expenses do you need to improve on?

Leave me your comments and questions below and I’ll be happy to reply.

Mr.CBB

Thanks for the recap. Every time I read your article s on budgeting I get new ideas and try to implement them. Me and my husband are retired but spend alot on our grandchildren . Which I budget for but never stick to it, but READING your articles pulls me back to reality.