{kind=link}

Estimated reading time: 5 minutes

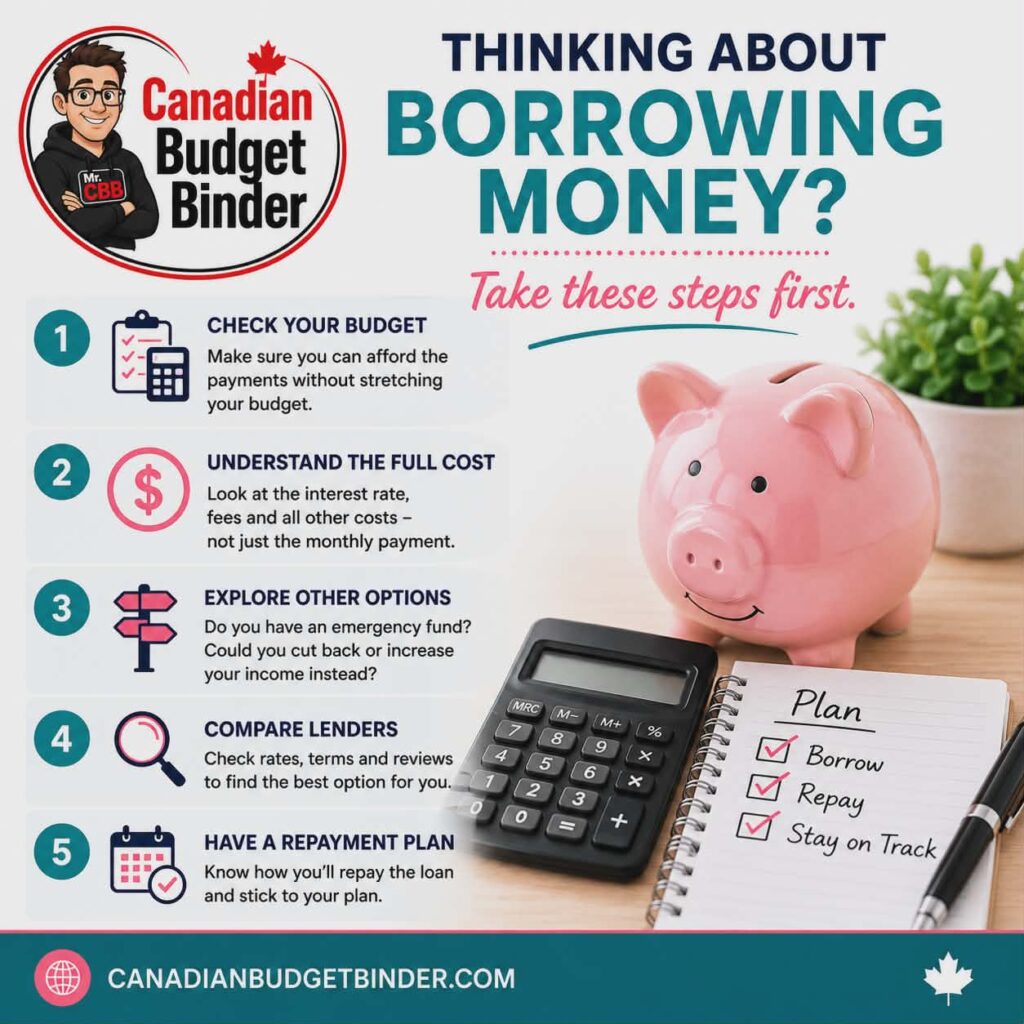

Before borrowing money, consider the crucial steps and factors involved. Discover your options for borrowing money today.

There are always different ways to request financial aid when you need it the most, provided you can pay it back.

Have you decided how and where you’ll be borrowing money?

The following tips are things you should consider before borrowing money.

How Much Money Are You Borrowing?

Once you borrow money, there are many things you can do, such as;

- Projects

- Make Expensive purchases

- Pay Off Debt

- Provide For Everyday Needs

- Help Family

When you borrow money, it must be enough to cover the expenses you need to pay immediately.

Compile, list, or estimate how much money you want to borrow.

Depending on where you plan to borrow, you might be offered the money you need or an estimate of what you can borrow.

Stick to the amount you need and can reasonably pay back.

Where will you be borrowing the Money From?

Another thing you need to consider is your lender. Who or where will you borrow?

Consider which will offer you the most convenience and the best possible offers, whether from a bank, a credit union, or even a cash advance lender.

For this reason, you can choose between your bank, credit unions (if you are a member of one), and lending companies, whether physical or online.

You can even borrow from someone you know if the amount you need isn’t that big.

If you borrow money from someone you know, such as a loved one, make sure you can trust them.

Let them know how you plan to spend the money and when you will repay them.

For your bank or credit union, you can always approach them to inquire about available offers, whether by email or in person.

For lending companies, confirm whether they are legitimate businesses unless you have already transacted with them.

If you want to try a lending company you haven’t heard of before, make sure it has a physical address you can visit, a secure website, and proof of registration, either in its office or on its website.

If you know it’s safe, consider how you can borrow money.

You can either go to their office for a more personalized transaction or for extra information.

You can also do it online for faster, more convenient deals.

How Long Do You Need the Money You’re Borrowing?

Time is essential to why and how you’re borrowing money.

You may have long-term commitments or projects you need to fund, or you may need to get by for a week, a month, or two until you get a better financial source.

Loans cater to both the long run and the short term.

How long will it take for you to use the money?

If you need it for a long time, you need to get a loan that will have your back for however long you need it.

Although if you want something fast and temporary, you can opt for short-term loans, though those tend to be more expensive.

How Much is the Interest Rate?

Another thing you might want to look out for is the loan interest.

Interest is the price lenders charge to lend money.

In other words, not only should you pay back the money you borrowed, but you also need to pay the interest rate given to you.

The amount varies depending on the loan type, the amount borrowed, and the loan duration.

Essentially, you would want to get a deal with a reasonable interest rate.

If you want a better look at your options, check each loan’s APR (annual percentage rate), which includes additional fees beyond the interest rate.

Consequently, you can also check how the loan calculates interest, which is simple and compound.

Simple Interest

What is simple interest?

Simple interest is multiplying the principal by the annual interest rate, and compound interest is adding the principal to the sum of 1 plus the annual interest rate raised to the power of the number of years in the loan, then subtracting the principal.

Does your Credit Score and DTI Ratio Pass the Application Requirement?

A crucial factor to consider is your eligibility to borrow money.

If you were personally borrowing from someone, you know there won’t be a problem.

However, borrowing money from financial institutions requires proof of your creditworthiness.

This is how lenders decide whether or not to give you a loan.

You can check your creditworthiness in two ways: your debt-to-income ratio and credit score.

A debt-to-income ratio is calculated by dividing your debt payments by your monthly income.

The result is the money you have that is meant to pay your debts. The lower the ratio is, the better.

Above all, a good ratio would be 36 percent or less.

A credit score is a number that indicates your creditworthiness.

Financial institutions assess this by looking at your credit history, primarily your debts, and whether you’ve paid them on time.

The credit score ranges from 300 to 900, with scores of 660 or higher considered good to excellent.

To Sum it Up

If you want to borrow money, plan.

You need to consider the amount of money you want to borrow, how long you need it for, where you want to borrow from, the interest rates, and your eligibility.

Therefore, as a result, you must get the best deals to make the most out of borrowing money.

Discussion: Have you ever needed to borrow money, and what process did you go through?

Please share your comments below.

Mr.CBB