{kind=link}

Estimated reading time: 26 minutes

Learn about the advantages of having an economical budget and why it is essential for your financial well-being.

An economical budget helps people adopt a lifestyle that fits their financial needs.

I struggle to understand how anyone could spend money frivolously and without care.

I’ve never had a moment where I’d spend money that I didn’t have apart from a mortgage.

As a well-traveled man, I’d book many holidays while working in the UK but saved in advance.

I’d never go on holiday if I had a debt to pay that was not my mortgage or vehicle, even though I had no car payment.

Perhaps my mindset is different, and that’s ok because we all view lifestyles differently.

Today, I want to briefly discuss the benefits of having an economical budget and why it might work for you.

Economical Budget vs. Bare Bones Budget

What does being economical mean? Economical means that you work towards not wasting and using the resources that you do have.

You might be considered a thrifty if you’re economical and use what’s already on hand.

Perhaps you will shop for secondhand items instead of buying something new.

When you’re at the grocery store, you might consider products that are reduced in price.

On the contrary, having an economical budget doesn’t mean you are living a bare-bones lifestyle.

Where economics is watching your money, a bare-bones budget has little to no money to work with.

A bare-bones budget is basic and tight because every dollar is already spent and then some.

For example, we need milk and cereal but can only afford to buy one or the other.

Working with an economical budget allows you to make choices based on frugality rather than necessity.

For example, with a bare-bones budget, you may not have $5 to spend on a secondhand top this month, so you have to save for it.

With an economical budget, you likely have $5, but choose to spend as little as possible.

An economical budget is tightening the ropes to save money; with a bare budget, the strings are ready to snap.

So, which type of budget do you choose? That depends on your needs but, most of all, your income vs. debt.

Often, this is called your debt-to-income ratio, which is easy to calculate.

What’s important to remember here is the end goal, not what type of budget you use.

There’s no shame, only positivity if a budget is used correctly, and eventually, you can loosen the reigns.

Take Caution When Using Credit

Indeed, there are credit cards, bank loans, and other means to obtain cash that needs to be paid back if there are no emergency savings.

Be prepared to understand not only the monthly debt but the overall cost of the loan or debt based on interest and the term.

A holiday on a credit card for $4000 at 19% interest and pay the minimum of $75 back each month.

It will take nine years and 11 months to pay off the balance. The total interest is $4,883.69.

That fun $4000 holiday will now cost you a whopping $8883.69.

Let’s say, for example, that you convince yourself that you’ll pay for the holiday over two years.

The repayment cost would be $201.63 monthly to pay off the balance in 2 years. For a total interest of $839.23.

For the same debt, you’d need $368.63 per month to pay off the balance in 1 year with a total interest of $423.52.

Economical Budget Success Tips

If using an economical budget is where you are financially, you still need to be frugal.

Although we have wiggle room, we tend to stick to an economical budget.

We try to keep things in perspective when we splurge because expenses can quickly get out of hand.

I can only offer success tips based on our zero-based budget experience.

Economical Budget Success Tip #1

Without Budget Management, A Budget Will Fail.

Continuously monitor and update your budget by reviewing it monthly while you input your data.

Economical Budget Success Tip #2

Always keep a thrift mindset and be resourceful with what you already have in your home.

Considerations range from food to clothing and other materials needed for projects.

Economical Budget Success Tip #3

Remove any triggers that might manipulate you into spending money you don’t have.

Economical Budget Success Tip #4

Understand why you are using an economical budget, and be careful not to waste money.

Perhaps you have a goal you are trying to attain, such as saving $4000 for a holiday.

Economical Budget Success Tip #5

Just because you use a budget doesn’t mean you are not successful with your money.

I’ve heard in the past that only people who are broke use a budget because they can’t manage their money.

Let me tell you that we are far from broke and will always use a budget.

Frankly, who cares what anyone thinks as long as you positively affect how you see your financial future?

Mr. CBB

Discussion: What does an economical budget mean, and how would you use one?

Please leave me your comments below.

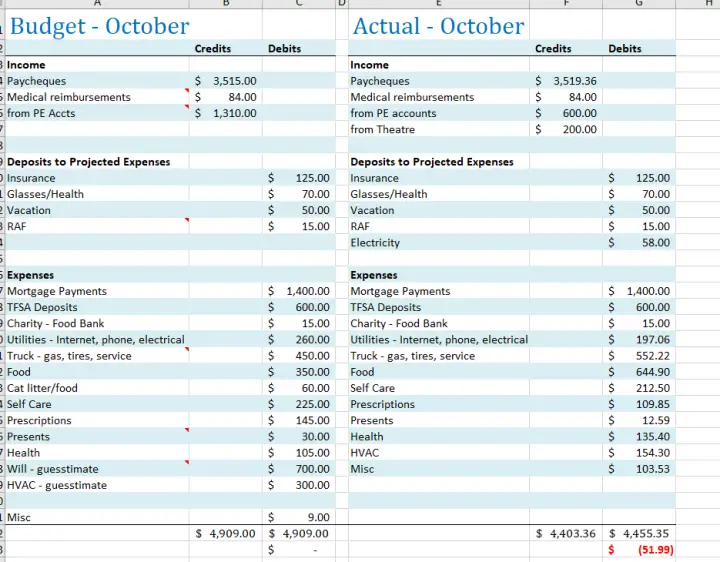

CBB Family Budget Report For October 2022

October Budget Summary

Hey Friends,

What a month October was, but ending the month with goblins and ghosts constantly improves things.

In October, we spent a lot of money on needed health and beauty products.

We also purchased new winter gear for our son and Mrs. CBB, who needed a second jacket.

She successfully found a secondhand winter jacket; however, it was not warm enough.

Just in time for the snow, our son has his new BOGS, which he loves.

We are working with him soon to learn how to tie his laces, but slip-on shoes and boots are perfect.

I don’t know about many of you, but we do more online shopping than ever.

We hardly ever go shopping at a physical store unless it’s for groceries, secondhand, Dollar store, or Shoppers Drug Mart.

We’ve lost our feel for shopping in person, although not 100%.

Do any of you ever feel this way?

Thanks for reading,

MR. CBB

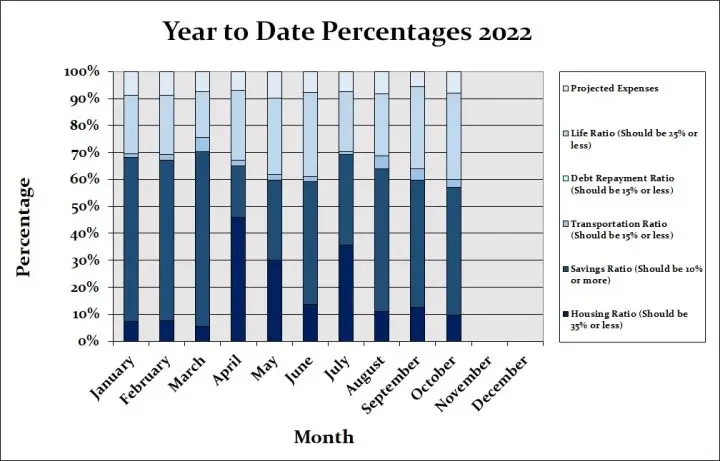

Year To Date Percentages 2022

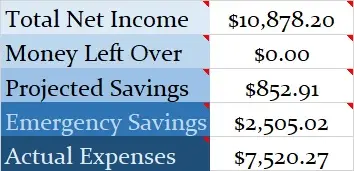

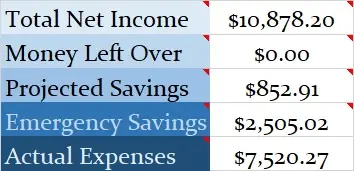

Our savings include investments and any savings for this month based on the net income of $10,878.20.

Equally important is saving money on our projected expenses in the coming months.

An example of projected expenses would be buying Christmas gifts in December or throughout the year.

All categories took 100% of our income, showing that we accounted for all the revenue in October 2022.

This type of budget is a zero-based budget where all the money has a home.

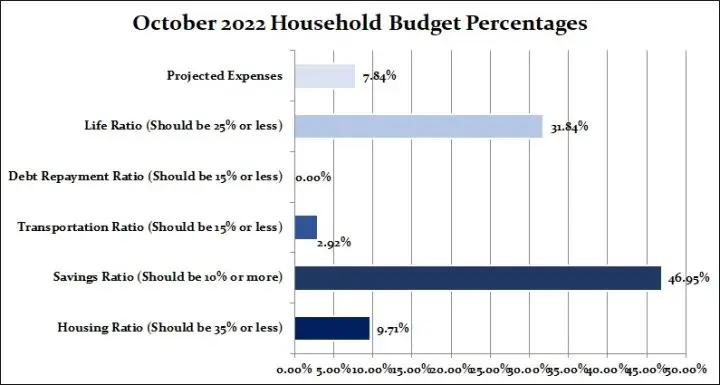

Budget Expenses Percentages For October 2022

Monthly Home Budget Breakdown

Below is a breakdown of our expenses, which helps us understand where our money goes.

- Chequing– This is the bank account from which we pay our household bills. We use Simplii Financial, TD Canada Trust, and Tangerine Bank. Join Simplii Financial today! Read more about the best Canadian online virtual banks.

- Emergency Savings Account– This money is in a laughable high-interest savings account.

- Regular Savings Account– This savings account holds our projected expenses.

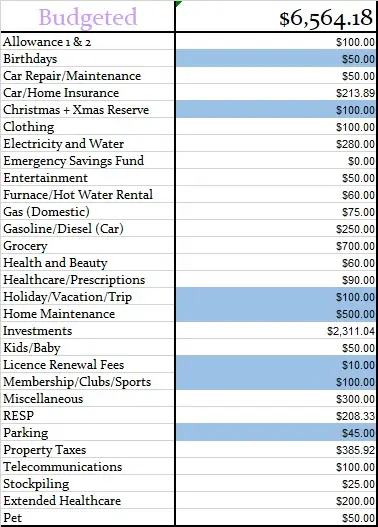

- Monthly Budgeted Total: $6564.18

- Monthly Net Income Total: $10,878.20

- (Check out the Ultimate Grocery Guide to see where our grocery money goes)

- Projected Expenses: These are expenses we know we will pay for throughout the year = $852.91

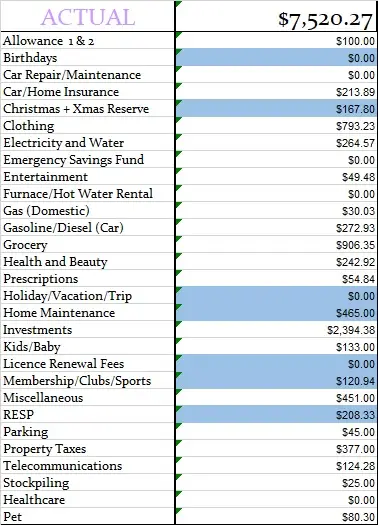

- Total Expenses Paid Out: $7,520.27

- Total Expenses Paid Out: Calculated is $10,878.20 (total net monthly income) – $852.91 (projected expenses) – $2505.02 (Savings to emergency fund) = $7,520.27

- Actual Cash Savings going into Emergency Savings: Calculated is $10,878.20 (total monthly net income) – $7,520.27 (actual expenses paid out for the month) – $852.91 projected costs) = $2505.02

Estimated Budget and Actual Budget

Below, you will see two tables: Our monthly and actual budgets.

Our monthly budget represents two adults and an 8-year-old boy.

Budget Colour Key: It is a projected expense when highlighted in blue.

Since May 2014, we’ve been mortgage-free, redirecting our money into investments and renovations.

Spending less than we earn and budgeting has been the easiest way to pay off our debt and save money.

Monthly Budget Amounts October 2022

Actual Monthly Budget October 2022

I’ll be back in December to share our November Budget Update.

Please read below to see how our 2022 Budget Challengers are doing with their monthly budget report.

Thanks for stopping by to read our budget update.

Mr.CBB

2022 Budget Challenge Canadian Budget Binder

Welcome to the 2022 Budget Challenge Reports.

This challenge has started over the past two years with many positive CBB readers who want to join.

For 2022, we began with six people ready to change their lives by challenging how they manage a budget.

As of October, we have four budget challengers for 2022.

Each budget summary will always fall under the same Budget Challenger number below.

If you leave comments about any of the budgets, always use the budget challenger number so they know it’s for them.

Budget Challenger #1

- Income Oct 14, 1092.32

- Oct 28, 1140.67

- Spousal support 700

- Sarcan 30

- V,s cell 95

- Net income =$ 3057.99

Expenses

- Income tax 100

- Car insurance 90

- Car repair 950

- Cells 266.26

- Elec/water/power 207

- TFSA 500

- RRSP 250

- Crave 16.70

- Wifi 80

- Gas 80

- Groceries 380

- Home Insurance 110

- Alarm 54.33

- S p.p. 50

- Water softener 30

- Water heater/ac/furnace 188

- Life insurance 75

- Lotto 7.50

- Entertainment 100

- Mortgage 560

- Parking 45

- Takeout 140

- Total expenses = $4279.79

- Total Income = $3057.99

- Total expenses = $4279.79

= – $1221.80

- September was + $22.00

- October I’m — $1199.80

October has been interesting as my son moved back in with me.

He has a different job now, and I want him to pay me back 200 dollars for the vaping he owes me.

I needed to buy new tires in October, which cost my budget 950 dollars.

On top of that, I was terrible and spent 100 dollars going out with friends.

Also, I spent 140 dollars on takeout food, which was not within my budget.

I’m supposed to be getting a 500-dollar cheque in November from the government, which I will put toward my debt.

Another potential good news is that I will get a raise of 1.30 dollars per hour at work.

I don’t know when that’s for sure, but it’s exciting, so I’ll tighten my bootstraps next month.

Hi,

Congratulations on getting a raise!!

Mr.CBB

Budget Challenger #5

Hi all, I hope everyone had a good October!

There’s not a lot to report for October. I didn’t pay my land tax fee on time because I got COVID-19 and forgot all about it, but that should hopefully be just a tiny fine next month!

October was a pretty easy month, and November has always been my big spend; so many extra fees fell on me that month, plus I’m going on vacation.

I bought a few small pieces of my vacation this month, but I’m trying to use my Airmiles to cover as much as possible.

As you’ll see, I joined the pool as well, but it’s cheaper to do the yearly membership, and I always get my money out of it, so I see it as a positive despite how much money it is in one go.

Fast food is higher than usual, but we did some traveling this month, both work and personal.

With my boyfriend not working, I am buying for him. I also took my mom to eat twice while in town with her.

There is nothing else to report this month; stay tuned for next month when I cry over how much of a workout I give my Visa!

Fast food 172.97

Groceries 377.5

Gas 303.31

Entertainment 26.45

Internet 110

Vacation 371.32

Car 192.50

Pool 283.35

Savings 200

Insurance 165.66

Xmas gifts 12.87

Phone 72.94

Hi,

I’m sorry you got COVID-19. I’m glad you’re doing better.

I am happy you are getting into the pool and taking good care of your health.

Enjoy your vacation.

Mr. CBB

Budget Challenger #3

October,

Nothing too nutty for October month. Our little boy turned 4, so there were some extra toys and birthday planning.

My husband took the kids to the city for a weekend; he goes with another dad and his two kids of similar age.

They rent a hotel, go to the Science Center, and do whatever else they can get up to.

We also got a 3-month swim membership and hired a former lifeguard to get our kids more comfortable with swimming.

Next month, he has some significant car issues and will change to winter tires.

Our student also vacated the suite downstairs as he decided school was not for him, so we are currently trying to find someone for January 2023.

Budget Challenger #4

Greetings from the Yukon, CBB!

What can I tell you about October other than the red ($51.99) in my tally is accurate – I overspent by 52 dollars this month.

The biggest culprit was food spending – there were several reasons for that (bulk buying meat, pantry staples that needed refilling, wackadoodle junk food purchases).

I was working on a show at our local community theatre, so I had to plan meals well. And I was good…up until I ran out of baby spinach.

Who knew baby spinach was one of the pillars of my budget?

Right at the end of October, I was struck ill with a non-Covid plague – there will be more evidence of that in November’s numbers with a week of unpaid leave.

I’m regrouping and looking forward to finishing 2022 as economically as possible. We’ll see what November’s numbers bring.

(As always, if there are any areas you would like to explain more in-depth, just let me know.)

Hi,

I’m sorry you aren’t feeling well and lost a week’s pay. Our son was sick for a week, as was most of his school.

Our grocery budget is always the worst category as we stockpile, and it’s the hardest to say no to, especially in-store deals.

We continue to monitor our spending habits. Good luck with your November and December. I’m sure you will crush it.

Mr. CBB