{kind=link}

YOUR MONEY IS JUST AS IMPORTANT AS YOUR HEALTH

I was retirement ready years ago but only because I’d rather not be working and instead of travelling.

However, I was not in any financial shape to say adios to my employer and honestly, I probably won’t until I’m in my 60’s.

With a defined benefits package I’m able to retire around age 60-62 and we’ll have a substantial retirement savings portfolio.

For others retiring early or on target age 65 for most Canadians means getting into financial shape early.

Some of you may not agree with me but money and health go hand-in-hand because living is not cheap, retirement comes fast and your health is not always 100% funded by the government.

That means that it’s your responsibility to save money today for tomorrow even if you don’t get the chance to use it all before you pass away.

Retirement Ready Means Freedom From Financial Stress

How much money will I need to retire at 65?

In June we met with our financial advisor and went over a custom detailed retirement plan based on how much we wanted to spend yearly.

Ideally, this is what you want from your financial advisor because using “rules of thumb” is not what you’d expect from a professional.

Our meeting lasted almost 2 hours to review in his office with a team of advisors which left us feeling positive about our future.

Thankfully, we are on track and our son will be more than set-up financially if we passed away today or at age 100.

We were hoping to spend between $70,000-$75,000 each year in retirement which may seem high but we’re talking 25 years into the future.

Perhaps, we won’t need $75,000 but for now, we picked this glowing number which may change as we age.

The idea is to live off of our investments so we don’t have to touch our savings.

The Four Percent Rule Of Thumb

The 4% rule is not going to be cut and dry but it’s certainly a great way to estimate how much money you will need to retire on.

The easiest way to calculate how much money you will need to be saved up to retire is to take what you would like to spend each year, divide that by 4 and that number is your retirement savings goal.

The 4% is he withdrawal rate of money that you can safely take out of your portfolio each year.

So if you have $100,000 and use the 4% rule of thumb you could safely remove around $4000 for approximately 30 years provided your investments were 50/50 stocks and bonds.

What this means is that you can safely remove around 4% of your portfolio each year without going broke for at least 30 years.

The only downfall is that you must earn at least 5% on your investments which is the bare minimum for the 4% rule to apply.

It seems simple enough but it doesn’t always work which means you’re taking a risk following it.

This also means you can’t just set up your retirement portfolio and let it ride out either.

You MUST review and adjust your plan to ensure you are meeting your retirement targets including inflation.

The 4% rule may be a historic generalized way of calculating how much money you will need to retire but again, it’s a general guideline.

Let’s have a quick look at a quick example of the 4% rule of thumb math.

If you want to spend $75,000 a year in your retirement to go on vacations or whatever your heart desires with-in budget this is what you’ll need to save.

- $75,000/ 4%= $1,875,000

Let’s say you want to spend $100,000 a year in retirement.

- $100,000/4%=$2,500,000

Spend Your Retirement Ready Money

Alternatively, you may end up with far more money than you anticipated so again living your best life while you can is important.

Although we want to make sure our son is a beneficiary to our wealth and is set-up financially in certain categories of life we want to enjoy it too.

Some people may end up leaving more money to their beneficiary because they fear going broke or something happening to their investments.

Just remember it’s your retirement and you earned the money and should be able to enjoy the best retirement possible.

Shape Up And Get Retirement Ready

For some of you, this may be common sense but not everyone grew up where money was the form of discipline to save for a rainy day.

In fact, most people that do come from homes where their parents were terrible with money to want to do better financially so they invest in educating themselves.

Then there are some that follow in their parent’s footsteps because they don’t know wrong from right with money and learn the hard way.

It’s only then they either take a broad look at where they are with their money, where they’d like to be and what they need to do in order to get there.

In saying that, everyone no matter what your basic financial knowledge is of budgeting successfully encompasses you should incorporate the following steps to become retirement ready.

1. Discipline

The hardest part about being disciplined with your money is when you are living paycheque to paycheque and are struggling to pay the bills.

In these moments you may feel hopeless that nothing you do will fix your financial situation and it’s depressing.

I’ve been there more than a few times in my life.

Here’s the thing.

No matter where I was financially I always made sure that my bills were paid, debt was paid and I had food on the table.

There was nothing more to my life apart from making sure the basic needs were met and anything extra went to my savings.

That’s where the financial high begins because as your savings grow you start to understand the positive side of financial depression.

Basically, you can be retirement ready with nothing in the bank or something in the bank.

The downside is training your brain to understand that even when you are financially high you can hit a low and to remember we all have to build our walls from scratch.

Sometimes our cake will flop and we have to start over but if you want the icing on the cake you need to keep building.

2. Budget

Without a doubt, budgeting is paramount for anyone who wants to become retirement ready and even sail through retirement years.

Not everyone will have a surplus of cash in their retirement portfolio which means you still need to budget.

Even my mother-in-law who has dementia still has a budget that is managed by us.

Without it, she would easily go broke during her retirement years.

This leads me to another good point that you should always have a WILL and Power of Attorney completed.

In the event, you can’t manage your retirement money and need someone to step in to help you will forever be grateful.

Finally, if you need to go into long-term care or need any form of help with your health not covered by the government it gets very costly.

If you are unable to drive any longer and need to hire a companion or driver the costs can add up.

Add participating in day programs when you retire if you aren’t in the best of health but want out of the house that costs too.

Investigate life insurance, critical illness insurance and anything else that may affect your future financial goals.

Trust me, you won’t want to sit at home staring at the walls day and night when you retire or if you are forced to retire early because of illness.

Having money saved up in our retirement or savings accounts will help get you over the hump financially.

3. Stop Throwing Money Away

No matter how old you are throwing money away on things you don’t need is a waste of your financial resources.

Getting retirement ready means you ask yourself how important something is today and whether you will need it tomorrow.

Many of our friends who are in their early 40’s are already downsizing their home and the stuff they have accumulated.

Trust me that as you age you won’t need half of what you think you need and I bet there are dust collectors already hanging around.

Buy what you need and will use, sell or donate what you want and take time before making any purchases little or big.

4. Pay Off Debt

Not everyone has the luxury of retiring with no debt but getting retirement ready means doing everything you can to avoid creating more.

You will want to pay off debt fast and if you are still paying debt such as a mortgage when you retire then work on getting rid of that.

Also, consider that if you do pass away what you are leaving behind for your executor to take care of.

Being debt-free is nice but getting there is a battle so;

- Stop creating debt,

- Pay debt off

- Find low-cost or free alternatives to fund what you can instead of using credit or loans

5. Invest Wisely

Obviously, if you want to be retirement ready you will need a financial plan and a good advisor along the way.

Perhaps you are your own advisor and manage your portfolio but also consider what would happen if you are not able to.

Then what happens to your investments? Just be on top of your financial game at all costs.

Saving money in a Tax-Free Savings Account or Registered Retirement Savings Fund from a young age is great.

I know some people who would rather buy real estate instead of buying into an investment portfolio.

Not everyone has the extra money to do so however do take advantage of any employer-matched programs.

Don’t throw money out the window when it’s free.

Get Retirement Ready or Retire In The Red

Whatever you do, don’t stash cash under your mattress.

Ultimately, if you do retire in the red you have to deal with the consequences and move forward the best you can.

Getting yourself into financial shape is not a set it and forget it retirement party that you hope is baked when the timer sounds.

Whatever your retirement ready game is making sure it is a solid plan and visit it often.

Discussion: What are you doing today to make sure you are retirement ready tomorrow?

Leave me your comments below.

Income Report July 2019

Where did the money go in July?

This month was filled with more renovation materials as we purchased two new bath and shower valves along with a sink tap, flooring, wall tiles and so on.

Our bathroom was a complete gut and we are hoping to complete the entire project around $5000-$6000.

The dentist once again took a chunk of money to pay for Mrs. CBB’s crown and hopefully the last one for the year.

Going into 2020 she will need two further crowns and that will complete updating her old large metal fillings.

A few other big expenses went towards buying a new garden hose, back to school clothing and Amazon Prime Day items.

Our petrol budget spiked as we have been travelling every two weeks or so to see my mother-in-law for a visit.

Investment costs have gone up significantly mainly our life insurance has changed which I will discuss in an upcoming blog post.

We are investing quite a bit more and our little guy has life insurance too!

That’s all for this month.

See you in August to recap where our money went.

Mr.CBB

Budget Percentages July 2019

Our savings of 25.61 % includes investments as well as any savings for this month based on the net income of $ 9835.75.

We put money away in our projected expenses for things that need to be paid for in the coming months.

All of the categories took 100% of our income which shows that we accounted for all of the income in the month of July.

Monthly Budget Expenses

Below is a breakdown of our expenses which helps us to understand where all of our money goes.

Since May 2014 we’ve been mortgage-free so much of our money will be directed at savings, investments, and renovations.

I appreciate that you enjoy this budget update each month but I do hope you view this as an educational tool rather than comparing your own financial numbers as our situations are all unique.

Spending less than we earn and budgeting our money has been the easiest way for us to pay down debt and save money.

It may be different for you.

- Chequing– This is the bank account where all of our debt gets paid from.

- Emergency Savings Account– This is a high-interest savings account.

- Regular Savings Account– This is a savings account that holds our projected expenses.

- Monthly Budgeted Total: $5873.93

- Monthly Net Income Total: $9835.75

- (Check out our Ultimate Grocery Guide to see where our grocery money goes)

- Projected Expenses: These are expenses we know we will pay for throughout the year = $324.98

- Total Expenses Actually Paid Out: $9988.11

- Total Expenses Actually Paid Out: Calculated is $9988.11(total net monthly income) – $324.98 (projected expenses) –$0 (savings to emergency fund) = We spent more than we earned!

- Actual Cash Savings going into Emergency Savings: Calculated is $9835.75 (total monthly net income) – $9988.11 (actual expenses paid out for the month) – $324.98 (projected expenses) = –$435.06

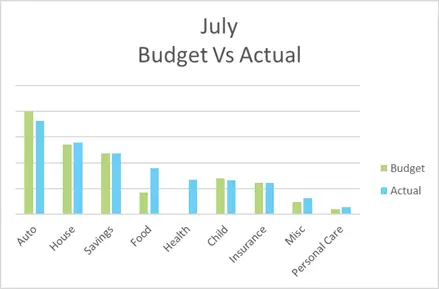

Monthly Budget Results

Time for the juicy category numbers and to see how we made out with our monthly budget.

Below you will see two tables, one is our monthly budget and the other is our actual budget for the month of July 2019.

Budgeted Amount

This budget represents 2 adults and a toddler plus retirement investments.

Budget colour chart: If highlighted in blue that means it is a projected expense.

Actual Expenses

10 Step Mini Budgeting Series

Do you want to learn to budget as we do?

Please take the time to read through our budgeting series plus read Budgeting in the New Year.

I hope the information will help stop you from making common budgeting mistakes.

Our Ultimate Budgeting Guide from A to Z has everything you need to know about budgeting in one blog post.

Over the years we’ve created a 10 Step Mini Budgeting Series that will help you understand how to start using a budget.

CBB Budget Updates Month By Month

Just in case you missed our budget updates and want to do a quick search I’ve compiled them all on one handy page: monthly budgets.

2019 Budget Challenge

When I was looking for people to join the CBB 2019 Budget Challenge back in December I had over 20 people interested in joining.

July 2019 Budget Challenge Update:

And then there were 3!

We started the year with 20 participants and are down to 3.

I’m so proud of these budgeteers!

As our budget challengers ventures along you may see their budget reports increase in data which I expect especially because it’s a learning experience for everyone.

The more you do a task the better you get at it and the more you learn about what you are doing.

The budget reports below will remain anonymous unless the writer chooses to use their name and each one will be unique.

They get to choose how they report their budget back to us.

Here we GO!!!

Budget #1

July is a relatively quiet month for us in terms of BIG payments…thank goodness!

After paying the property taxes last month, I need a little breathing room before the next round of annual payments come up in October, November and December…landscaping fees, house insurance, travel medical insurance, condo fees and taxes for our four timeshares not even mentioning the extra expenses that come up over the holiday season.

It never ends, does it?

We had a lovely Canada Day weekend with hubby cutting the grass and weed whacking on Saturday afternoon once it had dried up after the previous day’s rain.

It’s like a little competition on our street – one guy cuts his grass and the next thing you know, everybody is getting in on the action! LOL

On Sunday morning we made a quick trip to the US and scored some new summer shorts for hubby plus two of the 2-pack large stainless steel water bottles (also on sale) for when we are taking a road trip.

These were hubby’s first new shorts in nearly 20 years!

We’ve found swimming trunks on sale at the end of the season but generally, the nice shorts are gone by then so he was pretty happy to catch a sale at Costco US.

On Canada Day I got up super duper early (3:30 am) to deal with the month-end and quarter-end accounting before we headed off to the Canada Day festivities uptown that started at noon.

I made sure we had a good lunch at home though so that we were not tempted to go near the food trucks they always smell great if you are hungry but they sure put a ding in the wallet!

Our afternoon was filled with diverse entertainment, great bands, games, activities, and the tantalizing smells wafting from the assorted food trucks featuring all different cultures.

I love people watching and the kid’s mini-golf was particularly fun to watch but boy oh boy…were the bands ever loud!

We found a piece of shade between the 2 main stages but having 2 different bands playing at the same time it just sounded like noise.

I even had a wandering sax player, dressed in a cow costume, come up and play a song right in front of me.

The poor guy was melting in that get-up!

The weekend of the 5th, 6th, and 7th was really wet so we took advantage of the poor weather to enjoy just chilling out in the house and watching some movies we had taped on the PVR.

It was also the perfect excuse to drink a nice pot of tea too!

We tape movies all the time but rarely seem to sit down to actually watch them.

As a result, we have oodles to choose from including some Christmas in July offerings that have been on W Network.

I took advantage of the “Blue Friday” sale at Thrifty Foods this month to earn 246 Air Miles on a $127.23 shop.

That brings our 2019 air miles earnings to 743 of the 1,000 needed before December 31st to retain our Gold status.

I think I’ll start using my Air Miles Platinum AMEX again and it won’t take long to chalk up the remaining 257.

The weekend of the 12th, 13th and 14th brought grass cutting and visiting my sister in the hospital out in Abbotsford.

Every time hubby stepped outside though to try and continue his staining it started to rain.

Think somebody was trying to tell him something?

That’s 2 wet weekends in a row.

I remember how nasty it is to feel miserable health-wise and also feel like you are missing out on all the nice summer weather while cooped up in a hospital bed.

Back in 2015, I was there for the entire month of July.

At least I could tell my sister, she wasn’t missing nice weather it was raining again.

On the 20th we attended a Jack and Jill shower for my nephew and his fiancé.

My sister and my nieces hosted a terrific barbecue at their home in Delta for the couple and about 60 guests!

We gave the couple a Cerise (cherry red) 16 Quart Le Creuset Stockpot for their shower gift.

What else would a soup loving aunt give the soon to be a married couple? LOL

Our actual wedding gift for the engaged couple was a cheque to open a joint long term investment account.

My nephew is a whiz with his money, he’s a financial analyst for a living, so I have no doubt they’ll be growing our contribution in no time.

I wonder how much they can turn that cheque into before they retire?

They’ll have the power of nearly a half-century of compounding income.

Hubby continued his staining of the house every weekend that wasn’t raining.

The weather is so unpredictable, you have to do the staining as weather permits BUT for not too long if it’s scorching hot.

I get nervous having him on a 2-story ladder when it’s smoking hot outside!

I continued to top up the various savings accounts this month to get a little extra $$ in the bank accounts after my April sweeping investment of funds.

Last month the vacation accounts got the extra top-up.

This month I funneled any spare cash that I can scrape together into our accounts for personal taxes, car replacement, repairs & renovations, emergency money, entertainment & gifts and last but not least the appliance replacement account.

For August through December, the savings will once again be routed to the savings account designated for the annual transfer to our brokers back to our normal routine.

I did take advantage of a 50% off sale on Hilton points this month.

I guess that counts as vacation savings too, right?

I bought 80,000 points & got another 80,000 points for FREE ß there’s that word again! So, basically, I got 160,000 points for a cost of $800.00 USD.

For the sake of context, one of the places that we like to stay is 25,000 points a night so that 160,000 points will give us 6.4 pre-paid nights or a cost of roughly $125 USD per night.

Even using my BCAA discount, the cash price per night runs about $175-200 USD per night for that exact same room so basically the pre-payment using a points purchase will save us $50-$75 USD per night depending on the season that we travel.

These points are also great to have on hand when we take a road trip and there isn’t a Marriott property at our next destination – we have 10 times as many Marriott Bonvoy points as we do Hilton but using either one means a free stay.

I also transferred 240,000 Marriott Bonvoy points over to my Alaska Airlines account this month and got 80,000 miles with the conversion.

I now have enough miles in my airline account to fully pay for first-class return travel to anywhere in North America for both hubby and me next year.

BUT, it generally works out to be a better deal to book the “points + cash option” for the 4 tickets: my trip there, hubby’s trip there, my trip back and hubby’s trip back.

Alaska has a $200 USD limit per ticket on the discount achieved by using points so by booking each ticket individually, I save $800 USD and only use 1/3 of the points I would need to spend with the “points only” option.

In actual dollars and cents…a “$3,000 cash only” airfare for a trip could be either “$2,200 cash + 86,666 miles” or you could use “260,000 miles and $0 cash” for first-class return tickets for two to anywhere in North America.

The option I pick very much depends on how flush with cash we are in the vacation accounts at the time of my booking.

I also converted our 2019 allotment of 433,500 Vistana Signature Experience timeshare options into 711,150 Marriott Bonvoy Points so I won’t even miss those points that I converted to Alaska Airline miles. LOL,

There’s a 6-year expiry window on the converted points though so you need to keep track of what you need to use each year to avoid losing any points to an expiry.

Fortunately, they use an easy FIFO (First In, First Out) system and it is simple to track.

I have to use another 1,398,419 Marriott points before May 31, 2020, to avoid any expiries that will cover all but 2 weeks of our 2020 vacation.

For those 2 weeks, we are staying in assorted Vistana villas using some of our 2020 allotment of timeshare options.

We remain on track with our budgeting for July and have finished off our month with $2,607.84 in our vacation accounts towards the $3,000 budget that we are trying to achieve before year-end.

We’re getting there!

Budget #2

Hello,

Here’s my summary for July. Over halfway done with this year, I can’t believe it!

Current Status: 116% to budget.

Hello everyone! This month was a challenging month for us.

Our newborn caught a virus and got a UTI from it.

We spent a couple of days at the hospital so we ran up our parking and food expenses.

It was exhausting and I’m not sure we’re fully recovered from it.

Not to mention our little guy has colic and anyone who’s had a baby that has colic knows what a nightmare that is.

In fact, it was my worst nightmare going into this pregnancy which is something I’ve had to deal with.

Unfortunately for me, I have an anxiety disorder that is getting in the way of sticking to my budget.

I just want what is fast and easy so I haven’t been keeping up to our budget as well as I should.

I think though sometimes we just need a month to recharge without worrying about money.

We are super lucky that our government subsidy came in for our two children so it really helped keep our account in the green.

Wins:

Again we’re winning in the car department, even with the exorbitant amount of parking we had to pay this month.

Staying home really does make a difference, though not too much difference.

We also saved a little bit in the child department since we kept our older son home from daycare a few days early.

He’s staying home all of August with me and our new baby to save a bit on this cost then he’s going to school in September.

However, I would be remiss to say this wasn’t also eaten up by the baby stuff we had to buy this month (Diapers, wipes, etc).

Fails:

We “failed” in the food department badly. As I mentioned earlier this was due to the hospitalization of my baby and my anxiety creeping up on me.

I also was trying an elimination diet to see if perhaps my baby is sensitive to something in my diet so we had a couple of weeks of high grocery bill as I stocked up on some food that didn’t have the allergens.

We think he might be sensitive to milk products, but thankfully not allergic.

Budget #3

Here’s my budget for July.

This month has been extremely busy for us!

We had back to back mini-vacations at the beginning of July, which was a lot of fun, but exhausting.

I’m happy to say, they didn’t break the bank either.

We had some unexpected expenses this month our cat was showing signs that she may have been ill.

Thankfully it turned out she’s just a little stressed by our bathroom renovation.

We do have pet insurance, so the bill wasn’t too bad, but we have to pay upfront first and wait to be reimbursed, so that can be a pain sometimes.

I’m so glad we have pet insurance though, it has saved us a couple of times over the years.

Which leads me to our biggest challenge of the month our bathroom renovation which has been one setback after another.

I know most renovations have issues, but it just seems the progress has been incredibly slow.

To top it all off, we ended up spending an additional $1,000 due to miscommunication, so that was a huge hit to our wallets which we were not prepared for!

Our ‘Everything Else’ category this month included clothing, two donations, health, vacations, supplies for our bathroom renovation and other small miscellaneous items.

I found it hard to stay on budget this month as there seemed to be a lot of little things and a few big come up.

We’ll really have to watch it for the next few months to get back on track!

It just goes to show, even with the best of intentions and plans in place, finances are ever-changing.

- We had fun on our mini-vacations

- We officially started the bathroom reno

- Our bathroom reno put us $1,000 over budget

- We had some extra vet bills this month, but we should be reimbursed for most of it next month

- We ate out more this month and went to a few restaurants, so we’re over on our food budget

Hey Mr CBB… I have 2 questions:

1. In the retirement formula, is that for Gross or Net Income? The term “spending” confused me. I mean the

Desired Spending / 4% formula.

2. Is that retirement formula excluding the other revenue streams that you have and solely for calculating the funds we need to personally save?

Hubby will have a small pension, CPP, OAS and eventually at age 71 – 2 RRIF payments. My retirement is based solely on CPP, OAS and 2 RRIF’s…so I will delay starting the commencement of my payments until hubby, who is 6 years younger than I am, retires. I will base my RRIF payment on his age, rather than mine, to extend the life of my RRIF payments.

I had a fabulous suggestion from one broker, my smaller of the 2 RRIF payments could be deposited to our JOINT account at the brokerage house and then used to make our annual TFSA contributions. Basically moving my RRIF payment from one non-taxable account into another. Another tax saving tip! 🙂

Hi Mary,

I’m sharing a link for you that might help you learn more about the 4% rule from fellow Canadian investing blogger Retire Happy.

There are lots of tax tips I still have to learn about in Canada for retirement. That’s interesting the tax savings tips. I would have never thought of that but it does make sense.

Thanks Mr CBB… I will check it out!

You’re welcome Mary.