{kind=link}

The Scariest Household Budget Month Is Always December

We account for every dollar that we bring in and where it goes when it leaves our hands.

I’ve been told I’m a numbers nerd and they aren’t far off from the truth.

For 2020 we used a zero-based budget which worked out awesome for us.

If you’d like to read all of our household monthly budget reports to see how we did you can look under the monthly budget tab.

By the way, if you are new I just wanted to remind you that you have access to my free budget printables to make a budget binder.

I also wanted to point out that our excel budget is free as is our printable bare-bones budget.

This type of household budget is not new at all but it makes sure that all of your money has a home.

For the year 2020, we had four areas that we had to look at, groceries, clothing, Amazon, and Christmas.

Moving forward we will be making our goals for the year and the 4 budget areas will be adjusted.

Scared To Find Out How Well You Managed Your Money

You don’t need to be ashamed that you messed up a budget category you only have to mindful moving forward.

If you track your investments and household budget month to month the end of year numbers won’t be a surprise.

Once you get the hang of it you continue to improve and you see where you need to improve just as we do.

As you know groceries are on the rise for 2021 since the onset of the Coronavirus and it’s true.

It’s going to be a tough year for lots of Canadians but I have faith that if we plan a simple budget we can all do it.

At least that’s what we will be doing, especially with groceries the evil budget category for our family.

Food is love and so hard to turn away from which is why we are practicing mindfulness as you will read below.

Working From Home

I’m a price watcher and we must consider that it’s the winter and lots of produce are out of season.

We eat almost every day at home and hardly go out unless it’s through the McDonalds drive-thru or Tim Hortons.

I’ve been working from home since March and working to get ahead for the year since I have the opportunity.

Like most people, we spend too much on groceries even with a budget because it’s hard for us to leave an item we love at 50% off.

These expenses are factored into our grocery budget which is why we incorporated at $25 grocery emergency grocery stockpile.

I will be rolling out the new CBB Budget Binder shortly and I wanted to make sure that everything you need and my family needs are available.

Household Budget Mistakes

Some of the worst habits of people who budget unsuccessfully are that they eat out too much.

The second may revolve around holidays by going away too much without paying cash upfront.

Asking for deals may sound a bit too forward but you can’t score a deal if you ask for it.

For example, we negotiated with Rogers this year to lower our bill and they had no issue doing so.

I have posted so many cashback and savings websites for all of you to look into for more savings.

The boring part is signing up but the great part is getting money back or discounted from your order.

Some of my favorites are Rakuten and Great Canadian Rebates

Financial Update With Our Advisor

This is also the time of year we zoom with our financial advisor for 2021.

I think we will just drop the cash in our son’s education fund (RESP), our TFSA, and top up our other savings accounts with Manulife.

Overall we had a great year but I’m not saying anymore to jinx 2021.

Mindful Spending Is The Key

We all know that if we put our minds on the task at hand we will be mindful of what we are doing.

However, if you’re that type of person whose mind is racing with things you need to get done you won’t put much effort in.

For example, if we go grocery shopping we make our grocery list and buy what’s on the list.

During the year 2021, we plan on being mindful of our grocery shopping and clothing.

Discussion: What changes have you made or plan to make for your household budget?

Leave me your comments below.

Mr.CBB

Family Budget Final Household Budget Report December 2020

Where the money went

Our life budget category took a major hit in December however most of it fell under Christmas.

In 2021 we will most certainly focus on groceries again because we must do better at saving on food

We also paid out for our son’s Occupational therapy although my work benefits covered 85%.

As you see below we ended up hosting Christmas and bought some expensive toys for the boys.

This is another budget category that we chatted about increasing and work on less expensive toys.

I must say that the food and drinks I bought were delicious.

I’ll explain more in my Friday Newsletter.

How was your end of year monthly household budget?

Leave me your comments below as I enjoy reading them.

Mr.CBB

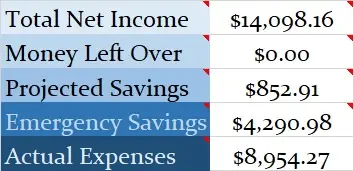

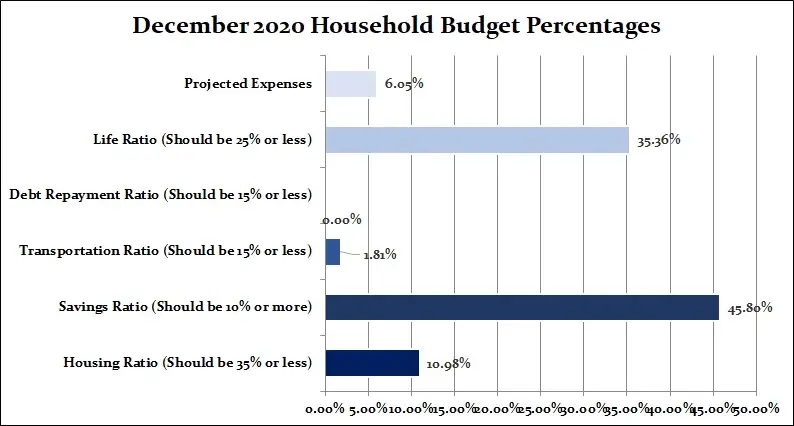

Family Household Budget Percentages

Our savings of 45.80% include investments as well as any savings for this month based on the net income of $14,098.16

We save money in our projected expenses for things that need to be paid for in the coming months such as Christmas.

All of the categories took 100% of our income which shows that we accounted for all of the income in December 2020.

This type of budget is a zero-based budget where all of the money has a home.

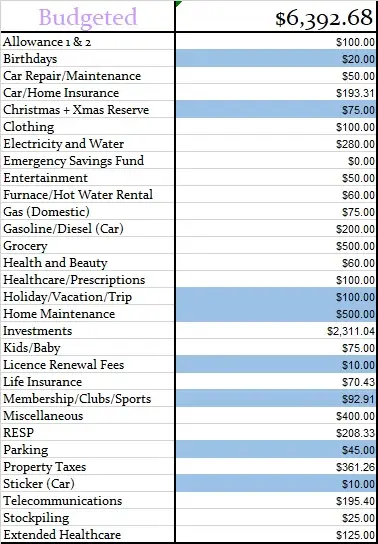

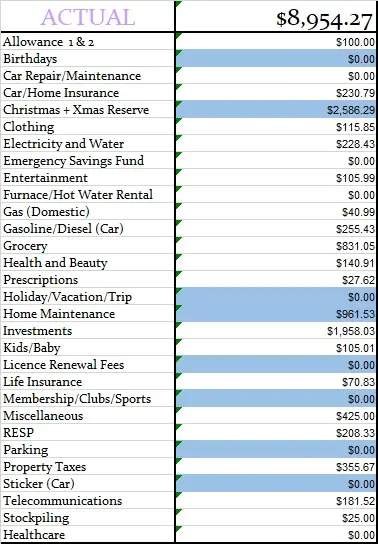

Monthly Household Budget Expenses

Below is a breakdown of our expenses which helps us to understand where all of our money goes.

- Chequing– This is the bank account where all of our debt gets paid from. We use Simplii Financial, TD Canada Trust, and Tangerine Bank.

- Emergency Savings Account– This is a high-interest savings account.

- Regular Savings Account– This is a savings account that holds our projected expenses.

- Monthly Budgeted Total: $6392.68

- Monthly Net Income Total: $14,098.16

- (Check out our Ultimate Grocery Guide to see where our grocery money goes)

- Projected Expenses: These are expenses we know we will pay for throughout the year = $852.91

- Total Expenses Paid Out: $ 8954.27

- Total Expenses Paid Out: Calculated is $14,098.16 (total net monthly income) – $852.91 (projected expenses) – $4290.98 (savings to emergency fund) = $8954.27

- Actual Cash Savings going into Emergency Savings: Calculated is $14,098.16 (total monthly net income) – $8954.27 (actual expenses paid out for the month) – $852.91 (projected expenses) = $ 4290.98

Monthly Household Budget and Actual Budget

Below you will see two tables, one is our monthly budget and the other is our actual budget.

This budget represents 2 adults and a 6-year-old son, plus retirement investments.

Budget colour chart: If highlighted in blue that means it is a projected expense.

Since May 2014 we’ve been mortgage-free so much of our money will be directed at savings, investments, and renovations.

I appreciate that you enjoy this budget update each month but I do hope you view this as an educational tool rather than comparing your financial numbers as our situations are all unique.

Spending less than we earn and budgeting has been the easiest way for us to pay down debt and save money.

Monthly Budgeted Amounts

Actual Monthly Household Budget Expenses

CBB Savers Budget Challenge Results for 2020

December Update: We are still 2 players in for the Budget Challenge 2020.

Congratulations to our two CBB friends who accomplished handing in 12 budget updates all of 2020.

You both inspire me because we had quite a few people who wanted to participate but

gave up or wasn’t able to.

It’s always nice to find financial lovers as I am because budgeting is very important for today and tomorrow.

This goes to show you that if you are determined to become debt-free and stick to a budget you can.

Let’s have a look at what happened with their monthly budgets in December.

To thank you both for budgeting along with me I’d like to send you a gift card, transfer, or cash through Paypal.

Message me your preference.

Mr.CBB

Budget Challenger #1

Our year is winding down and hubby was on vacation for the entire month! (Nice huh?)

We had a few RRSP maturities for me to re-invest this month.

However, I’m sure we won’t keep up with inflation at the current rates available on investments therefore we’ll have to cut our 2021 expenses even further to ensure we can save enough to keep up.

Do you see the penny pincher in me rising to the surface? I also need to keep working on trying to find new ways to save.

Again this month I added the money that I had budgeted for groceries and gasoline into our savings by using our gift cards and the cashback funds that were paid onto my Visa in November!

We got a not so pleasant Christmas gift on Dec 15th when I learned that the vast majority of our income stream has been permanently eliminated due to covid-19 and the closure of another Canadian business.

Going forward we’ll be working with 2/5 of the income that we enjoyed previously. Merry Ho Ho to us…NOT!

It could be worse though, at least we are both still alive and kicking!

I am sure glad I use a budget!!! I re-worked our budget on the morning of the 16th and let hubby know that we have a small monthly shortfall until I start collecting my CPP and OAS…six years from now.

Thank goodness we have an Emergency account!

The worst part of that shortfall is that I have already cut as many expenses as I could, eliminated all saving except for hubby’s annual RRSP contribution, and restricted our vacationing to once every 3-5 years. New purchases of any kind will be few and far between.

On the plus side, we are debt-free and aren’t trying to dig our way out of a deficit with such a reduced income.

Losing 3/5 of our income for the next 6 years constitutes a struggle but it’s time to get even more creative with working with anything I have on hand.

I actually turned 65 this month, so if it gets too hard for me to wiggle and jiggles the budget as prices continue to rise won’t wait until I turn 71 to draw my OAS payment.

I will still hold off on my CPP and RRIF payments though.

On Christmas Day we made a Rustic Cabbage, Potato, and White Bean Soup to have with some hot-out-of-the-oven Blueberry Gluten-Free Biscuits.

I already had all the fixings in the house so there were no costs involved. Woo hoo!

For my birthday, we used a couple of Olive Garden gift cards to pick up some take-out:

- a couple of half gallons of Zuppa Toscano Soup

- 2 Jumbo Family Sized Green Salads

- a couple of dozen breadsticks for my hubby only since they are not gluten-free and I can’t eat them.

What an inexpensive birthday celebration we had!

I had EVOO & a very nice Aged Balsamic Vinegar in the pantry for my sweetie to use when dipping his breadsticks.

We celebrated New Year’s Eve at home, as is our custom, and we used gift cards from The Keg for a second treat meal this month.

FREE is certainly an improvement over the cost of any New Years’ celebrations where we have gone out for the evening!

The big expenses this month were paying the condo fees and taxes on our 4 timeshares, renewing our BCAA VIP membership, and renewing the 3-year service contract for our heat pump and furnace. Sigh.

It’s a bit of a painful way to close out the year but we have a rule in our house, ABSOLUTELY NO expenses are ever carried from one year into the next.

It does leave you feeling rather broke on Dec 31st as you look at your bank account though.

With the cut to our income, I have to say that I am glad I am so diligent about setting money aside every single pay period to cover all those nasty payments!

If ever there was proof that a budget is the smartest thing you can do…this set of events with both reduced income and increased expenses!

On the plus side, we did earn LOTS of Marriott Bonvoy points with our year-end payments because I used my American Express Marriot Bonvoy credit card to pay them all.

After all the bills were paid, and the points were earned I paid off my credit card in full so that it was sitting at $0.00 at the year-end.

We can use these newly acquired points either for either travel or gift cards in 2021 I’m betting it will end up being more gift cards.

On another positive note, hubby got a rain check back in October for a half-price turkey breast and we threw it in the freezer for our holiday season.

I already had a fully cooked 1.2 kg ham in the fridge for New Years’ meaning that our grocery expenditures in December were really minimal!

We only bought a bottle of coffee creamer and a few loaves of bread this month (2 regular loaves and 1 gluten-free)!

I am extremely grateful for having had a wonderful month at home with my husband with both of us in relatively good health.

I feel a little more stressed than usual but I am assuring my sweetie that we can do this and that I am on top of the situation.

Bless him for trusting me to let him know if or when we have an issue that we need to address.

I wish you all the very best for 2021! It’s time to start our budgeting process over again – and our motto for the coming year will be SAVE, SAVE, SAVE!

Dear CBB Saver #1

Congratulations on finishing the budgeting year with us.

It sounds like you had a lovely, quiet Christmas and New Year’s together.

I loved the sound of that cabbage potato soup white bean soup.

One part that stood out to me was your rule of never carrying debt over to the new year.

Could you explain to me what it is when you have 4-time shares?

Any time there is a cut to income things have to change. I’ve been through it with Mrs. CBB having to leave her job.

However, I know you can do it.

Happy Belated Birthday! 🙂

Mr.CBB

Budget Challenger #2

Hi all, happy 2021! December was a bit rough but not too bad. My healthcare-related expenses were super high.

I was using up the last of my physio/osteo/massage appts so I had to pay out a bit towards those, but my osteo was billed incorrectly and I was charged full price.

I need to connect with my insurance company and get it fixed, then I will have a credit of $180 or $204 coming my way.

Things got a bit confusing so I’m not sure about the amount. I also bought glasses and because of my poor vision.

I pay a crazy amount so that was another $204 – and I only paid half so I’ll have the other half coming to me in January or early February.

But this is the first time I’ve bought glasses and loved them so, it is what it is.

My phone bill and fast food costs were also higher.

I had to make long-distance calls when my grandfather died.

However, I thought I had long-distance and didn’t.

I probably could have called and asked for credit for this as a long time customer, but I honestly figured I would break down balling and I figured it was worth my sanity to pay the extra $22ish dollars.

Fast food-wise, I paid for meals for my family while we were planning and working on my grandfather’s estate.

My fast food is always a high amount, but this seemed about $60 more than I normally would spend.

Christmas was pretty cheap. We all decided we didn’t want to do Christmas. At the last minute, I decided I was going to buy a few small gifts so that was approximately $137.

Now that I go back and look at the spreadsheet, I also had my wood stove cleaned which was $147.50 but I usually do it every 2 years so that’s not bad.

Year as a whole: as I’ve mentioned in previous posts, I try to put things into categories similar to how Gail Vax Oxlade talked about in her books.

I’ve broken it down a bit more here for review.

I’m not overly horrified by my amounts. 2020 was a weird year.

I think this would have looked totally different if I had been working in an office, working from home from March to July definitely saved me money.

Short term savings is money automatically deducted from my paycheque, whereas long-term is what I ended up being left with after all my bills were paid.

I feel that most things are super reasonable except for my fast food addiction and my internet cost.

There are cheaper internet providers here but everyone always complains about how slow they are the customer service issues or power outages.

I’d rather pay more to not have issues with those things.

If I were to take part in this again next year, I would like to see my fast food costs go down, but as of right now I think I’m doing well.

I don’t have a huge wage but I make sure that I don’t spend crazy (yes yes, except for my fast food addiction).

Not having a mortgage last year, and finishing out my car payments near the end of the year definitely helped and will help me with saving towards a new car, and household repairs that will be coming up including a new deck and working towards a metal roof.

CBB Saver 2 Household Budget Yearly Recap

Overall yearly totals:

- Power bills 1177.28

- Home and car insurance: 1736.52

- Home repairs and firewood: 1663.96

- Property tax: 797.96

- Groceries: 3575.06

- Fast Food: 1138.71

- Clothing: 254.56

- Phone: 723.80

- Internet: 1140

- Entertainment: 658.65

- Health appts and glasses: 525.70

- Pets: 371.17

- Vacation: 1238

- Gas: 768.72

- Car Payment: 3464.83

- Car Maintenance (regular and unexpected): 1010.15

- Gifts: 474.23

- Short term savings: 2200

- Long term savings: $16789.51

Dear CBB Saver 2

It sounds like you’ve had a great year of saving paying off your mortgage and car loan.

Now you know how awesome it feels to own something or at least we feel free knowing it’s ours and our truck.

I’m so excited for you but keep using your budget and stay in the debt-free zone as much as possible.

How do you plan to save money in 2021?

We have 4 Vistana Signature Experience timeshares on Westin properties…3 in Palm Desert, CA and 1 in Cancun, Mexico. I do not intend to use the Mexican timeshare. We simply bought the Mexican timeshare options, prior to the completion of the property, to extend our California stays at a low cost and reduced condo fees and taxes.

Each timeshare is a 2 bedroom lock-off for a 1 week stay. We can split the lock-off and extend our stays to between 8-12 weeks every year depending on what time of year that we choose to book and whether we take the large or small side of the 2 bedroom.

The great part of the timeshares is that we can book any of the Vistana properties, use the Interval timeshare worldwide booking system or simply convert our timeshare options into Marriott Bonvoy points with access to even more hotels, villas and private home rentals around the world with 30 different chains. If we choose not to travel, like this year, the points can be used for online shopping that includes merchandise, car rentals, services offered such as massages or golf fees, restaurants on their properties, car rentals or loads of assorted gift cards. Another option is to bank your options, for up to 2 years, and take one really extended vacation every 3 years! In our case, we could extend it to roughly 36 weeks!

We picked up our timeshares during the last recession when the US was in a deep dark place with mortgages and no one had the extra money to consider vacation investments. We picked up our holdings at roughly 1/3 of the price that they are today!

On the downside, you are pre-paying the condo fees and taxes for the following year each December. So, you need to be okay with having a year’s worth of accomodation costs in one fell swoop…budgeting becomes critical! We love our holdings and the flexibility they gives us!

Hi Mr. CBB, Do we let you know in advance that we want to complete the Budget Challenge for 2021 or just send you our budgets at the end of January to participate? Inquiring minds want to know.

I’ll let you know as I haven’t put a call out for it.

What I will do is ask the fans if they want to join on FB and in my newsletter tomorrow.

We can go from there.

Go ahead and email me or pm me on Facebook as I’m putting the list together

Lisa i posted the challenge today on my Facebook group Canadian Budget Binder. Could you please email from FB your name and I’ll add you to.the list and give you the rules

Well, this is a vastly different budget from last year because we lost 60% of our income stream to a Canadian company closure resulting from covid-19.

I think perhaps I NEED to do the Budget Challenge this year to keep myself on the straight and narrow. I am struggling trying to live on 50% of the grocery budget that we had last year…so count me in! 🙂

If you want to participate email me or send me a message on Facebook so I can get you added