{kind=link}

Estimated reading time: 29 minutes

Create a budget for debt reduction with a sample budget. Find Excel spreadsheets and budgeting tips from Canadian Budget Binder. Get motivated with these budgeting tips!

A sample budget is nothing more than offering ideas to the reader and a motivational mindset.

How many of you want out of debt forever and are ready to leap into the budgeting world?

When I began blogging at Canadian Budget Binder we decided to post our monthly budget update.

We didn’t have to do that but budgeting was a massive part of the structure of CBB.

As we began our budgeting journey with debt I went full-force creating budgets that we could use as well as our readers.

How Discovering A Budget Sample Helped Us

Like you, I scoured the web looking for a sample budget just to see what other families were doing.

Offering our free Excel spreadsheet was the tip of the iceberg and just what people wanted.

Then I learned that not everyone wants to use Excel or doesn’t know how to use the program.

From there we tooled with a printable bare-bones budget, cash budget, budget jars, student budget, and the budget envelope system all of which work for certain people.

Canadian Budget Binder is almost 10 years old and we continue to use our Excel spreadsheet.

It has gone through many facelifts but incredibly it’s a simple budget hitting all the right spots.

Today, I’m sharing an email from a reader who has struggled financially amid COVID-19 and would like to see a sample budget.

I think you’ll see just how much diving into a sample budget can offer you especially if you’re not using one.

Sample Budget To Get You Money Motivated

Dear Mr. CBB,

Over the past two years since the start of Covid-19, we’ve been struggling significantly with our money.

At the end of every month, I’m juggling what money we have to pay off our debts.

We do not have a budget and frankly have no idea where to begin with one.

Do you have a sample budget that we can look at to help us get started?

If it includes sample expenses that would also help me out to understand what I need and don’t need.

Thanks,

Malvine B. (St. Thomas, Ontario)

That’s a fantastic question Malvine and I want to thank you for taking the time to explore financial opportunities to make improvements.

Learning About Budgeting

If you are new to budgeting like Malvine I always suggest reading my 10 Step Budgeting Mini-Series.

This will give you the basics of budgeting and how we approach them in the CBB household.

Recently I blogged about the lockdown budget and how to approach it with strength.

The reason is that struggling to pay the bills including rent is hard for anyone in that position.

Currently, we use a zero-based budget which means that all of our money is accounted for or has a place to go.

Sample Budget To Study

Malvine was asking to view a sample budget with expenses as examples.

Although this may be interesting to read each one of you will have different expenses.

It will never be a case of, if we follow what Mr. CBB does with his budget then we can become debt-free.

If anything our budget categories will be where you may want to explore.

The idea is to design your budget based on your needs however we offer you the shell (the free budget).

12 Years Of Our Budget With Real Numbers

For those of you who don’t know I post our actual monthly budget which in essence is a sample budget for newbies.

I’ve logged every budget that we’ve done under the Monthly Budgets Page where you can travel back in time.

What I want to point out is that our budgeting journey has had highs and lows and we own them.

This is important to remember that budgeting will never be perfect as we all have weaknesses.

At the end of the day, we became debt-free and set our mortgage on fire.

That was our goal and we attained it with no financial help from anyone.

If you want it bad enough you’ll do anything (legal) to get it done.

Sample Budget For Low-Income Families

For starters, budgeting is for every budget even if you’re struggling or broke.

I remember emailing back and forth with a young lady in 2017 and she wanted to know if I had a budget for low-income families.

Related: How To Create A Budget When You’re Broke

It was then I realized that perhaps people thought that to use a budget you needed savings or little to no debt.

My answer to her was that a budget does not judge by your income or lack of income.

I eventually found out that she wanted more of a student budget sample so she could create one before going to University.

The only prerequisite to budgeting is to work with a realistic budget.

By this, I mean being honest with your money.

What Is A Budget?

A budget is a financial tool to help understand what money is coming in and going out.

You can work with a budget that is detailed or basic depending on goals, motivation, and time.

The right question should have been asking me to see a sample budget to review and try.

I know many of you have tested my free budgets and have shared your success and happiness.

So, no there is not a low-income sample budget, there’s just a budget.

Types Of Budget Sample Ideas On CBB

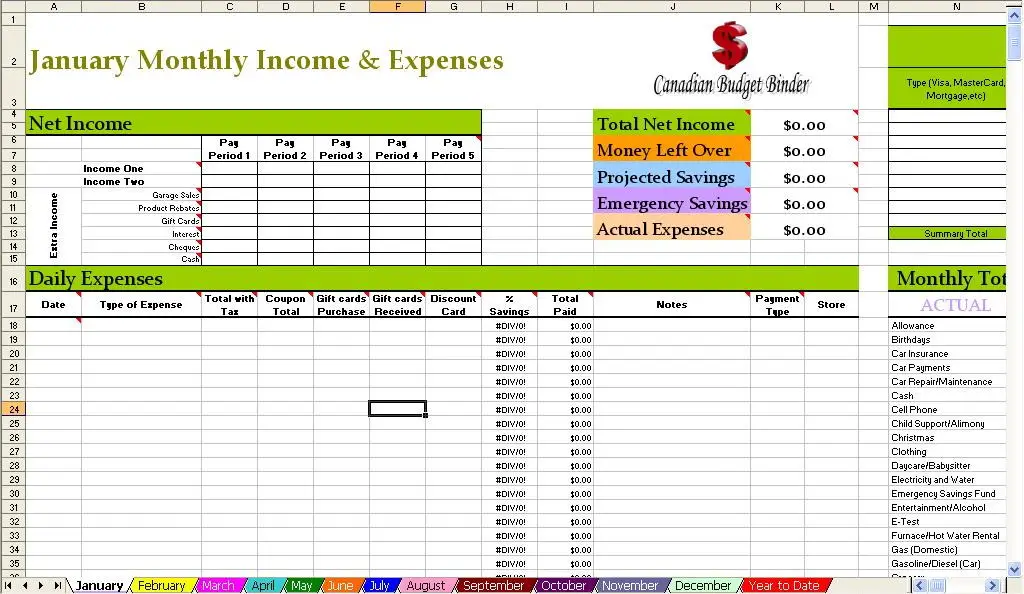

Once you subscribe to the blog you will have access to my free budgets on the resource page.

On this page, you will find two Excel budget spreadsheets which I will describe below.

Budget Sample Excel Spreadsheet 1 & 2

Excel Budget Spreadsheet #1- Click To Download> Monthly-Budget-with-ability-to-change-categories-2021

- You can use the pre-existing budget categories or use your own and you have the option to use projected expenses.

- Please read the notes for Quick Tips by holding your cursor in each cell with a note symbol.

Excel Budget Spreadsheet #2- Click To Download> Monthly-Budget-with-Yearly-Report-and-Graphs

- Everything is pre-set so you have to use the pre-defined budget categories but this budget will generate year-end budget figures where the other one won’t but you must use the categories already in this budget.

- NOTE: If you change anything you will mess up the formulas and year-end figures.

- Please read the Quick Tips by holding your cursor in each cell with a note symbol.

If you want to customize then you need to use Budget #1 but you won’t get year-end reports unless you create the charts yourself or use Budget #2 where it is all built for you.

All formulas are open which means if you break a formula then your numbers won’t add up.

If you are not sure what projected expenses are read Step 10 in our budgeting series below.

The Basic Budget Sample

A basic budget is all you need when you start your budgeting journey especially when you are learning how a budget works.

You could also jump into the Excel budget spreadsheet if you are comfortable with that.

Sample Budget Plans To Dig Into

Next, you’ll want to explore what type of budget plan you want to apply to your budget.

For us, a budget plan is how are we going to manage the budget and using what system.

These are the only budget sample systems that I have on CBB although there are many more to consider.

- Zero Based Budget

- Cash Budget

- Envelope Budget

- Budget Jars

- 50/30/20 Budget

- Budgeting Apps (Post coming soon on the best Canadian Budgeting Apps)

- KOHO is a reloadable prepaid Visa card attached to a budgeting app that assists the user in the budget, and manages money all the while earning cashback on their purchases.

Discussion: How many of you found this blog post because you wanted to look at a sample budget? If yes, comment below and tell me what you were trying to understand.

Thanks again to Malvine for writing in and I hope I’ve given you lots of resources to explore on Canadian Budget Binder.

Mr. CBB

CBB Family Income Report April 2021

Hi CBB Friends,

Where did all of our money go in April?

April was a unique month of expenses especially as we are in lockdown again.

We made a trip to Costco and doubled up on typical items that we buy.

This drove our grocery expenses far over budget but that was planned which we both agreed on.

In April we earned 71,000 PC Optimum points between Shoppers Drug Mart and Zehrs although we still get points from our PC MasterCard.

Most of my spare time has been outside in the garden as I purchased most of what I needed from Canadian Tire.

I also bought lights for each fence post in the back garden instead of wiring the ground lights.

Over the years outdoor animals have chewed through the wires so I couldn’t be bothered.

Lastly, as you may or may not know we have a new kitten and budget category for him.

Most of the expenses are one-time so we will see that category significantly reduce.

What we do need to do is add expenses for the kitten into projected expenses.

Pets are nice but also costly if a vet visit is in order.

That’s all for April.

Share in the comments below any comments or tell me about your budget.

At the end of this post, you can read 7 monthly budget updates from the participants in my 2021 Budget Challenge.

Feel free to comment on them as well.

Take care,

Mr. CBB

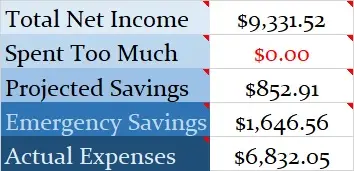

Family Budget Percentages

Our savings include investments as well as any savings for this month based on the net income of $9331.52.

Equally important is that we save money in our projected expenses for things that need to be paid for in the coming months such as Christmas.

All of the categories took 100% of our income which shows that we accounted for all of the income in April 2021.

This type of budget is a zero-based budget where all of the money has a home.

Monthly Budget Home Expenses

Below is a breakdown of our expenses which helps us to understand where all of our money goes.

- Chequing– This is the bank account where all of our debt gets paid. We use Simplii Financial, TD Canada Trust, and Tangerine Bank. Join Simplii Financial today!

- Emergency Savings Account– This is a high-interest savings account.

- Regular Savings Account– This is a savings account that holds our projected expenses.

- Monthly Budgeted Total: $6570.80

- Monthly Net Income Total: $9331.52

- (Check out our Ultimate Grocery Guide to see where our grocery money goes)

- Projected Expenses: These are expenses we know we will pay for throughout the year = $852.91

- Total Expenses Paid Out: $6832.05

- Total Expenses Paid Out: Calculated is $9331.52 (total net monthly income) – $852.91 (projected expenses) – $1646.56 (savings to emergency fund) = $6832.05

- Actual Cash Savings going into Emergency Savings: Calculated is $9331.52 (total monthly net income) – $6832.05 (actual expenses paid out for the month) – $852.91(projected expenses) = $1646.56

Monthly Budget and Actual Budget

Below you will see two tables, one is our monthly budget and the other is our actual budget.

This budget represents 2 adults and a 6-year-old son, plus retirement investments.

Budget colour chart: If highlighted in blue that means it is a projected expense.

Since May 2014 we’ve been mortgage-free so much of our money will be directed at savings, investments, and renovations.

I appreciate that you enjoy this budget update each month but I do hope you view this as an educational tool rather than comparing your financial numbers as our situations are all unique.

Spending less than we earn and budgeting has been the easiest way for us to pay down debt and save money.

Monthly Budgeted Amounts 2021

Actual April 2021 Budget Expenses

That’s a wrap for our April 2021 monthly budget update.

Be sure to check back in June to see how May turned out by subscribing to Canadian Budget Binder.

Thanks for stopping by,

MR.CBB

2021 Monthly Budget Challenge

Currently, we have 7 Budget Challengers for 2021.

Let’s see who can keep up for the entire year and who drops out of the challenge.

Feel free to comment about any of the challenger’s budget report in the comment section by using their Budget Participant Number.

Budget Participant #1

I thought when I was discharged from the hospital on March 19th that it would be smooth sailing ahead.

Unfortunately, the rest of March had oodles of medical appointments and on April 7th, I was back in the hospital for a NEW issue.

No sooner did we get that solved and I headed back into another round of surgery on April 15th.

The budget for us is working though and all these issues so I say thank goodness that we do budget…because the medical expenses have certainly been coming fast and furious!

This month we had crutches, a wheel chair a leg brace, and tensor bandages to pick up.

In between hospital stays I did manage to get our personal income tax filings to the accountant for the preparation of our 2020 returns.

Hubby handled the pick-up of the completed e-filed returns, paid our accounting fees, and paid his 2020 taxes owed at the bank on the way back.

My pending refund is sufficient to pay his taxes owing for the next 2 years so I will invest the funds so that they are available when needed.

I am still working on the March 2021 quarter-end statement and I have boatloads of corporate posting and returns to do – when I feel well enough.

Slow but surely is my motto this month.

Hi,

What a month for you both although I’m glad that you are home now and hopefully on the mend.

Medical expenses are costly especially if they are not covered under benefits.

It sounds like you have everything prepared so your husband knows what to do in case of an emergency.

Both Mrs. CBB and I know everything about our finances just in case something happens to one of us.

Take good care of yourself. x

Budget Participant #2

Hi all, April ended up being weird money-wise. ‘

My money situation should have looked quite a bit different but times being what they are, COVID restrictions can change things up greatly.

At the beginning of the month, I paid for a year-long gym pass.

I love going to the gym, I find it difficult some days, but with it being directly across the road from my work, I usually find it a great way to wind down at the end of the workday.

They had a great promotion if you joined then (save the building fee of $20 plus get a month free for $44ish) – on top of this if you paid for the year as a whole you’d save 10% – DONE!

I also spend just shy of $30 on some second-hand workout clothes which isn’t a normal thing for me. I would completely find this worthwhile….oh but yeah, COVID.

At the end of the month, everything was locked down and gyms closed, so no gym for me.

I’m assuming they will tag on extra time at the end of the year, but I’m not going to worry about it for now.

However, that leads me to some big savings and big spending.

Because of the lockdown, I went and bought a ton of groceries.

I don’t like to go out more than twice a month if at all possible. This led me to spend about $75-100 more than I normally do on food.

I saved about $20 on fast food compared to what I normally spend so that helps to offset it a bit.

Gas was also down a bit as I work in 2 different offices (one close to home and one not) and because of the lockdown I was supposed to work at my closest office, this saved me about $30.

The unfortunate thing about the lockdown was that I was supposed to help my mom pack and move.

Her move was scheduled for May, but I was going to go down on weekends and then rent a truck in early May to help her move.

You’ll hear more about that in the May update.

Lockdown is very strict and we have rules about where we can travel, my mom lives 2.5 hours from me so I was not able to do this.

I ended up saving money on the gas I would have spent going there each weekend to help her pack.

However, I will end up paying a lot more in May because I am paying for a moving truck to move her (she can’t drive).

I’m sure my back will be thanking me for saving it the strain, but my bank account won’t, it’s going to cost about $1200 more than I was expecting to do this.

I have also continued my counseling appointments.

Having an Autoimmune Disease, stress impacts me, and I have to be honest COVID still happening is burning me out.

The impacts of stress make me sick and I can’t process food properly which leads to a ton of issues.

I had hoped to be referred to the specialist clinic which has counseling built into the sessions, but apparently, they are “closed until COVID is over”.

When my doctor’s office called to tell me the referral had been sent back for that reason I was shocked.

The prevalence of Autoimmune disease is severely high in this province, so to shut down the only specialty in the clinic with no set reopen time shocks me.

But this was the long way of me saying I ended up paying $200 more than what I thought since I thought I would now be getting it free.

Nothing else really to report for May – the rest of my expenses have stayed the same this month.

Looking to the future, my goal in May is to cut down as much as I can to offset the cost of the move.

Depending on how long we are on lockdown, I won’t need as much gas money.

As well, I won’t be eating out (or if I do it will be minimal), and based on how much in groceries I purchased at the end of that month I shouldn’t need to buy much.

I believe I have property taxes next month so that’s another huge chunk coming up but at least that only happens twice a year.

Hi,

Health is so important and can really affect mental health when things are wrong.

My wife suffers from severe anxiety because of her disease and does have free counseling through our doctor’s office.

That’s nice that you are helping your mother with the move and I look forward to reading about it next month.

Mr. CBB

Budget Participant #3

Hi all!

April sucked and I don’t have a pretty way to put it. Welcome to my life, Budget #3

Let’s talk numbers, what went right and what went wrong.

First, the good news is that we’re all still employed and have stayed healthy.

We paid off any remaining soul-sucking credit card debt to the tune of $2,512.79.

My spouse decided to charge lots last month.

Paid off the motorcycle loan so that’s $316 I no longer have to plunk out each month – $4790 – That’s the end of the good.

Budget Expenses That Stayed The Same

- Cable at $232

- Groceries stayed on budget of $300

Now the ugly

Unfortunately, our truck died although I didn’t think my Mr would replace it so fast.

- $2500 down payment and a loan for $32,323 with monthly payments of $508

I don’t think I’m ever going to get ahead unless he gets on the same page as me.

We did sell the old truck with a plow for $4000 and the car he drove for work for $1300,

I won’t see that money until this month since one of the kids bought it and are waiting to pay.

I thought we would put the money from the aforementioned vehicles on the loan but Mr had other plans.

Then I found out if we put a snow plow on the new to us truck it voids the warranty so on to the next bad.

Sold the old tractor since it would cost more to put a snowplow blade or snow blower on it than it was worth – $4300 to the plus – Same day, bought a new tractor for $9600.

Since then we have spent over $2000 on various implements for said tractors.

There went all the vehicle money.

The electric company decided we have not been paying enough on our budget plan so upped my monthly payments by $27. This budget expense is now at $225 a month.

The phone bill is usually $58 for two lines, although this month with various work from home and internet outages the total bill was $116.

Things that evened out: My 401K finally got rolled over from my old job to my current 457 plan – My retirement is now at $110,000.

After cleaning my late mother-in-law’s apartment out and having a yard sale, I made $1800.

I put it on my student loans that are on hold until September.

Hi,

It sounds like you’ve been hard at work trying to balance your budget. Finance is a big struggle for everyone especially those with a high debt to income ratio.

If he didn’t buy the truck was there another vehicle you could have used in the meantime?

Did you talk about buying the truck first so he knew how you felt in terms of your financial health?

I found it interesting about the warranty on the truck if you were to add the snow plow. I’m not sure if it works like that in Canada but now I want to know.

Keep at it and keep crushing your budget goals and debt. Never give up.

Mr.CBB

Budget Participant #4

This month I got paid 3 times which was great.

I have been doing a lot of thinking about my finances and believe I’m doing better.

After finishing my budget I feel that I’m doing worse. although I’m not giving up.

I have sat my son down and talked to him about my budget.

We are going to make more changes next month and I’m happy to have started my TFSA.

I was sick for a week so I had my groceries delivered to the house..

I’ll need to make a phone call to check about life insurance as the other one has ended.

After calculating my lotto expenses I realized that I spend 80 dollars a month which is 960 dollars a year. Wow!

Next month I want to have a yard sale if I’m allowed because of Covid-19 restrictions.

I still have a full 3-bedroom house full of furniture in my 625 square foot house

I’m giving up lottery playing and reducing my budget expenses further next month.

I would also like to contribute to my registered retirement savings again.

This is not budget-related but I have entered into a 10 km run that is in June, but virtual.

I’m exercising and have lost 8 pounds so far.

May is going to be another adventure.

Hi,

Congratulations, I can tell that makes you feel great.

I like that you said you would not give up on your financial journey. Budgeting takes time to improve and you’ll get there. I encourage you to read my 10 Step Mini Budgeting Series for motivation.

Mr. CBB

Budget Participant #5

April was a busy month with work and life.

Carryover was $18.56 for the month which is not a lot but still something.

The first week of April leads to spending a lot on unnecessary items like Easter for 4 grandkids and getting my nails done.

I should have known better, ugh.

This frivolous spending cost me –$228.59.

Then I had my winter tires switched to my summer wheels and storage. –$144.30

This I do not consider an unnecessary spend as the other two things.

I’ve also started selling many unused items to earn extra cash.

Buying A Vehicle

I realised that my 2017 Tucson SUV has only 1 year left of warranty.

The mileage was great at less than 47,000 kms but I still owe -$23,000.00 (rounded)

My SUV has had three recalls already completed.

That had me thinking if it is a good idea to stay with her or trade her.

I decided to start looking about trading her in for something with a lot more warranty.

I’m not even sure if that was even possible to find with the same km or even less than.

It would be great if I could score, less of a monthly vehicle payment.

I ended up finding a new to me SUV with 4 extra years warranty.

It’s also the same year 2017 with 37,000 km (rounded) less payment and vehicle debt is –$21,312.51.

That becomes a bi-weekly $202.42 payment to a bi-weekly payment of $132.42 will give me a savings of $67.79 times two = $135.58 per month.

I will be applying the extra savings to the principle of my RBC line of credit (RBCLOC) each month.

My new payment starts on May 14th and continues bi-weekly.

The usual payment of $202.42 that would have come out on April 30th payday will be applied to RBCLOC.

It makes me incredibly happy that I continue with a secure vehicle.

I went from a Hyundai Tucson 2017 to a 2017 Buick Encore.

This is an incredible win in all aspects for me.

Fairstone’s charge was a NO interest purchase with ONLY three remaining payments of $119.94 each two for May and one June. YEAH me.

That equates to $119.92 x 2 per month = $239.84 which will be going straight to my RBCLOC snowball in June 2021.

Selling In A Sellers Market

My house mortgage is $115,877.00 also is bi-weekly $323.22.

With the baffling selling market for housing at this time, I even considered this.

However, I decided that it was not a smart move for me.

The selling aspect would be great but then my purchase aspect is not good.

Firstly, I have debt and if my house sold all that debt would be paid off and leaving me with not much buying power for a new home.

I discussed this with a few friends and both said this would not be a good decision at the moment.

My small home is perfect for us and perhaps can look again at this in a few years.

By then I won’t be so in debt and to purchase will be a bit reasonable. Right now, it is not a buyers market.

Other Expenses For April

This was a three payday month but regardless it mainly will go towards paying off debt.

I’m thankful my daughter was able to purchase a lot of groceries this time around.

Added expenses for April were CRA repayment at –$110.00 and this will be automated from the bank account until September 2021.

My dog Chloe’s dental surgery is one-time only –$423.90 paid on my Visa credit card.

My Hyundai SUV had tires switched and the winter tires were stored at a cost of –$144.30 at the beginning of April.

I am unsure if my stored winter tires can be used on my new SUV.

I will make an appt to see if they can determine this and if not, I will need to try and sell winter tires.

Investment Portfolio

I had a look at my investment savings and a few went up which is encouraging.

My employer has increased our match for the pension contribution.

At this time, I will stay with what I have and can change this at any time.

I do not believe I can afford to have another increased amount coming off my paycheck just yet.

As of now, I have increased from $25.00 to $50.00 for extra taxes so I won’t have to pay next year.

Although I know realistically my taxes should almost be a zero dollar or owing next to nothing or getting next to nothing back.

Grocery Expenses

Groceries are just a killer again.

I tried online grocery shopping and price matching and they are just expensive.

My daughter’s two children are not little people anymore where you can prepare 1 box of Annie’s mac/cheese and they will be content.

They are young teenagers and have what we call friggin bottomless stomachs.

We are entering May with a surplus of $234.00 and this is with items that have been sold and directly deposited.

The money that people pay cash with is still in the cup and been used to pay cash for like my haircut, etc.

I have moved the money that people e-transfer from my main bank account to emergency savings.

The idea is to build up the emergency savings after the unexpected furnace repair at the start of the year.

Again, I am grateful that I had the funds saved but sad to see it go.

Budget Participant #6

I have never run a marathon but I feel that this challenge is exactly that, a financial marathon.

April was a difficult budget month for many reasons, and all of them are because I just had trouble feeling motivated,

I had trouble controlling impulse spending, and truthfully, not really caring.

Maybe it’s COVID, maybe it’s because I felt that we would be in a different place by this time.

My work is tied into the COVID response and the vaccine rollout so I think I had built up a better April in my mind, or maybe it’s because it’s spring.

All that said, we have overspent in two budget categories.

Our grocery expenses were over budget by 336 dollars and clothing and gifts were over $457.22.

It was my mother’s birthday but I see the overspending as a reflection of the blues that I had noted earlier.

Looking at the recap, I am proud that we still recorded every single purchase.

In the past, that is maybe when I would have quit and stopped writing expenses down.

Another good highlight was the forecast for the garden supplies- we had saved money for that expense.

It was empowering to know that when I was in greenhouse bliss, we had the money saved (cue another metaphor on sowing the good financial roots now for future gains.)

One final comment of note is that we have received a tax refund, a total of $2,446.21.

In past years, when there was a tax refund, it would just go into spending.

This year, with the goals that we have, we are putting it towards savings.

Re-reading the recap, it doesn’t feel as dark as it feels as there were still gains.

We are still committed and in this marathon, need to refocus on our spending pace.

Hi,

It’s amazing to know that you’ve saved for something and are able to spend it.

This is why I created the projected expenses for our CBB budget in 2012.

Although we can’t predict every projected expense it has worked out beautifully for us.

Do you project expenses throughout the year and save for them monthly?

Mr. CBB

Budget Participant #7

Well, the month of April came and went so very fast.

We shifted into a third lockdown (yay Ontario) and from in-school learning to now online.

Was it a great month for us? Not this month at all!

This month we overspent by a lot although I didn’t mean to, but here we are.

I did not pay attention to my grocery bills and overshot my budget by $338 this month.

This shows me that by bringing my calculator (aka phone) into the store and tracking each thing that goes into the cart saves me money!

I also spent way over budget on my kids as well.

Of course, they needed new clothes for the spring/summer.

When shopping I made my way to out to our local used clothing store to “reduce, reuse, recycle”.

All of the kids’ old clothes have been sold or donated as well.

The last category I overspent was for birthdays.

My two boys’ birthdays are in May, my stepfather, grandmother, and brother are all in May as well.

When we included Mother’s day we are $131 over budget.

Related: Projected Expenses and How To Include Them In Your Budget

Ways I Will Be Cutting Back Expense

- Bringing my phone to the store with me to help calculate my final totals

- Watching for PC Optimum points on the normal things I buy

- Using Coupons

- Selling Items we no longer use in our household for extra income

Since May is birthday month, and I have already spent what I need to on birthdays, things should settle down in that department at least until September!

The kids already have their summer wardrobes ready to go, hoping my husband doesn’t need any “new” clothes either.

Even though we overspent, we are lucky enough to save our money to be able to have months like these.

I am not proud, but it is making me look back at mistakes and how to move forward.

Hoping for a wonderful month of May!

Hi,

I enjoyed reading about your failures and how you plan to make changes for the next month.

This is what I want to see because the only way to know where our money is going is to be mindful of it.

Tracking expenses and income along with budgeting is never a bad thing.

It won’t always be perfect but it’s better than not doing anything at all.

Keep at it.

Happy Birthday!!! – Mr. CBB