{kind=link}

A MORTGAGE IS A HEAVY DEBT

Kissing our mortgage payments goodbye one year ago this month was one of the greatest accomplishments we’ve achieved financially as husband and wife.

Honestly it was my wife that reminded me that it has been a year since our final mortgage payments were processed. Time certainly does fly by but I’m certain since having our son time is just a big blur to the both of us.

Mortgage Payments are reality

Having no mortgage payments have not gone unnoticed though as our budget has shrunk and our net worth has jumped up to just under $700,000.

It would be nice to be worth a cool million before I turn 40 although that may be super optimistic of me. When we conquer one hurdle we set goals to conquer another.

Having mortgage payments will add bulk to any budget but it’s not the end of the world if you have one. The reality is that most people who have a mortgage pay for it until the end of their term unless they pay extra to shave a few years off here and there. That is great if you can do this as every little bit helps.

Have a look at your mortgage amortization schedule and you may notice that you will likely be paying for your house twice by the time your done your final mortgage payments. That’s the price we pay to borrow money. That really gave us a jolt to get paying if off.

For those of you who have been able to pay the mortgage down quickly you know it’s no easy task and it takes plenty of planning and budgeting doesn’t hurt either.

Some people roll consumer debt into their mortgage and others take out equity to complete renovations or even worse go on a holiday. Either way you will be paying more money for the mortgage the more you prolong the pay-down process.

Another reality is that most people will never be faced with the option to pay cash for their home so taking out a mortgage is the only way to go. This is what we did after saving our down-payment.

We have always wanted to learn how to manage debt so it wasn’t burdening our retirement and stopping us from enjoying our golden years. Owning a home was a large debt that we knew would likely be the biggest of our lives.

I know there are hard-core investors out there that may cringe at the fact that we paid our mortgage off but that’s their opinion.

We can’t control how much investments would make so taking control of the mortgage and eliminating our biggest financial hurdle seemed logical. Besides, it’s always going to be six of one and half a dozen of the other. Either way, you are aiming for the same retirement goal. Security.

There’s always going to be the mortgage pay down debate but if you are happy with your decision there’s not much to debate. Only 6 years after buying our home for $265,000 we can sell it for about $430,000-450,000 comparable to recent home sales in our area.

Saying you own a house may be true but you don’t really until you own it outright.

Like I said, debt is debt and all you have to do is miss one mortgage payment and Mr/Mrs. Banker may just step in and steal it away from you. Until then someone has a hold on your umbrella and if the bills aren’t paid that umbrella can easily close.

Security and Freedom

We weren’t taking the chance that something could happen to either of us and we had the cash so paying it off seemed natural to us. Other reasons we decided to become mortgage free besides being safe from foreclosure was…

- stress relief

- opportunity

- freedom

- more money to invest

Did we invest anything into our retirement savings? That’s always the popular question and the answer is simple.

Of course we were investing in our retirement along the way. The good news is now I am able to max out my RRSP as well as catch up with what I’ve missed out on since I started working in Canada.

Over the past year we’ve been able to save or invest $15,797.00 which would have been what we paid for our mortgage for one year.

It doesn’t sound like much but in time that will all add up and hopefully it will be a comfy retirement savings plan for the wife and I to enjoy when we finally say goodbye to the working world.

Do we think it was worth it for us to pay off our mortgage?

We’re not complaining and honestly although it’s been an odd feeling not having a mortgage to pay it’s the best feeling knowing that no one can take our house away from us now.

How long until you have your mortgage paid in full?

Where The Money Went

In May there was an extra pay period for us due to there being five Fridays’ in the month. Add that together with a second job and a tax refund cheque and you end up with a great month of income.

The tax refund will be going back into paying more RRSP’s for the 2015 tax year, not on a hot tub or something ridiculous.

Some extra spending on top of the normal expenses were accounted for and consist of getting the vehicle cleaned to get rid of the winter salt and plants for the baskets and pots outside of the house.

Nothing out of the ordinary happened in the month of May as I was still finishing off my second job contract. The forthcoming months will be different however, with renovation completions and days out enjoying some of the summer weather before it disappears for another year.

How was your budget month?

About our Free budget

I’m currently offering 2 versions of our budget and the reason behind it is simple. Firstly, read the CBB blog disclaimer because what you do with it is your own business so if you mess it up you need to sort that out.

I have not closed off any cells so you can make all the changes you like to the budget to reflect your lifestyle which is what you asked me for in your emails. (See I do listen and read your comments and emails)

Although I would love to help every single fan with their budget I am unable to do so but I am always willing to answer any emails you send me so don’t be shy.

This was after all meant to be our personal budget and although I would love to customize it for every fan that wants to use it but, I’m afraid I cannot.

I’m not selling this budget or hope to make any money from it so enjoy this free budget and I hope that it works for you as much as it does for us.

Our Free Budget Spreadsheet

You can download the free budget spreadsheets here.

- Budget 1– You can use the pre-existing categories or you can use your own if you wish and you have the option to use projected expenses or not. Please read all notes left around the budget for tips.

- Budget 2-Everything is pre-set so you have to use the pre-defined categories but this budget will generate year-end budget figures where the other one won’t but you must use the categories already in this budget. If you change anything you will mess up the formulas and year-end figures. Please read all notes left around the budget for tips.

I’m always open to feedback but be polite as you don’t want to hurt my feelings ![]() Test it out for a month and see how it goes. There is never any harm in trying something new.

Test it out for a month and see how it goes. There is never any harm in trying something new.

Our budget plan

How we budget our monthly expenses?

I often have fans ask me how to budget money on a low-income or they simply a high debt load and want to kill it like my friend Tony who got rid of over $100,000 worth of debt by using a budget.

CBB fans want to know what we do in order to save so much money and the reply I give is simple>> It’s not about the money it’s about the process involved.

We are both money managers of our finances and with our relationship compatibility we have been able to get to where we are in 2015, debt free.

It doesn’t matter if you are using a cash only budget or you use your debit and credit cards, if your budget doesn’t balance you have budget issues you should review it pronto.

Learning how to be your own money manager is important because no one else will care about your money more than YOU!.

We don’t always save as much money as we would like every month but most importantly we are not going into debt but only because we are budgeting our money. In fact we are currently debt-free including the mortgage which means all we pay for is our monthly bills and expenses.

One of the most important things we did for our personal finances was that we never let the budget deter us from reaching our goals.

Sure we’ve had crap months but we’ve made up for it or we learned from our mistakes just like we should. Budget failure only occurs when you give up on your budget which should not happen as long as you truly want to reach your goals.

We didn’t always earn the income we do today but made do with what we were earning so we didn’t go into debt. That my friends is called “living below your means”. The only science to becoming rich!

Sometimes fans email and ask me if living on a budget in Canada is any different from living and budgeting in other countries. To be honest I’m going to say, probably not.

If I still lived in the UK I could use this exact budget spreadsheet to meet all of my needs however the budget needs to be reviewed monthly.

Below are links to the budgeting series which I wrote while designing our excel budget spreadsheet which will give you an idea just how we designed our budget.

I’m not a financial planner/advisor so I can’t tell you how you should budget but I can show you how we budget our numbers. I’m just a regular guy just like everyone else; some might call me a budget or numbers nerd.

Learn How To Budget: Our budgeting series

Do you want to learn to budget like we do? We explain everything we do and more in this mini-series all about budgeting.

Please take the time to read through our budgeting series plus read Budgeting in the New Year. I hope the information will help stop you from making common budgeting mistakes that I hear of often and that you take something away from the information and apply it to your financial situation.

If you have any questions about what we do with our money tracker ie: The budget than feel free to email me. I may expand more on the topics as we go along and add some mini-series in 2015 detailing how we budget to break it down even further for you.

- How We Designed Our Budget Step 1– Gathering All the information

- How We Designed Our Budget Step 2– Categories

- How We Designed Our Budget Step 3– Tracking Receipts

- How We Designed Our Budget Step 4- Note-taking

- How We Designed Our Budget Step 5– 5S Organization

- How We Designed Our Budget Step 6– Who Does What and When?

- How We Designed Our Budget Step 7– Balancing Our Budget

- How We Designed Our Budget Step 8– Knowing our Coupon Savings

- How We Designed Our Budget Step 9– Reading Our Bills

- How We Designed Our Budget Step 10– Projected Expenses

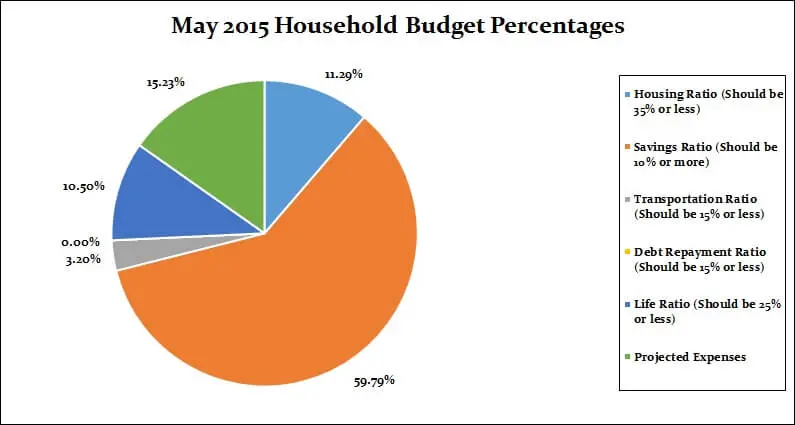

Budget percentages May

Our savings of 59.79% includes savings and investments and emergency savings for this month.

The monthly total spend comes to 100% which shows that we spent our income this month and used the rest as emergency savings.

The other categories were well within the defined percentage limits. Our projected expenses this month is at 15.23%.

Budget percentages month by month

Expenses breakdown

This is simply a breakdown of our expenses which has helped us to understand where all of our money goes. As of May 2014 we are mortgage free so much of our money will be directed at savings, investments and renovations.

I appreciate that you enjoy this budget update each month but I do hope you view this as an educational tool rather than comparing your own financial numbers as our situations are all unique.

Although I encourage your comments and love to hear what you have to say about our budget categories and expenses please don’t tell us to donate our money to charities because we have too much or are fortunate.

We are hardly out of the clear with finances for the rest of our lives and have worked and sacrificed to get where we are. We do plan to enjoy the money we’ve saved now since we haven’t over the years with our son.

What we do with our “extra cash” is our business and although we do donate to a charity we won’t be putting it on display for the world to see as it defeats the purpose in my eyes. It is part of the budget as you see it. I hope that clears that up for those of you who had concerns about our extra money.

Almost 7 years ago I started working in Canada making a bit over minimum wage and have since moved up the ladder. I’m now working very hard to secure my dream job with one foot in the door. We aren’t all lucky but if you do the best you can at least you can look back and say you gave it a shot.

Sometimes we wish we had more money to budget with but understand that we only have what we earn and if we want more, we need to earn more. Spending less than we earn and budgeting our money has been the easiest way for us to pay down debt and save money.

- Chequing– This is the bank account where all of our debt gets paid from.

- Emergency Savings Account– This is a high-interest savings account.

- Regular Savings Account– This is a savings account that holds our projected expenses.

- Monthly Budgeted Total: $4,916.82

- Monthly Net Income Total: $11,595.53

- (Check out our Ultimate Grocery Guide to see where our grocery money goes)

- Projected Expenses: These are expenses we know we will pay for throughout the year = $1,766.35

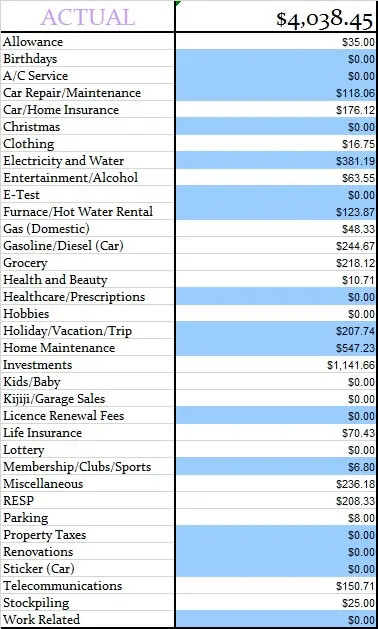

- Total Expenses Actually Paid Out: $4,038.45

- Total Expenses Actually Paid Out: Calculated is $11,595.53 (total net monthly income) – $1,766.35 (projected expenses) – $5790.73 (emergency savings) = $4,038.45

- Actual Cash Savings going into Emergency Savings: Calculated is $11,595.53 (total monthly net income) – $4,038.45 (actual expenses paid out for the month) – $1,766.35 (projected expenses) = $5,790.73

Saving money

What are Projected Expenses? – We project expenses throughout the year so we have the money saved. PE= A projected expense is money automatically saved each month so it is ready when the bill comes in or when you need it as in the example below.

We review our projected expenses at the beginning of the year to set up our yearly budget and adjust as we go along if a new projected expense arises and needs to be added to the budget. Sometimes we remove a projected expense as well so it’s very important to keep an eye on your expenses.

This has happened on many occasions but it’s bound to happen as we can’t predict everything we have to pay for over the course of the year. The important part for us is that we are saving for these expenses and we no longer have to stress about taking money from our savings to pay for them. To learn more about projected expenses read Step 10 in my budgeting series.

When we spend the money in a projected expense category we move that money to our chequing account in order to pay for that incoming expense. So this means the numbers go up and down in the projected expenses account based on what we need to pay for that we saved for in the account over time.

The only thing you need to do is track your projected expenses each month manually as I can’t customize that for you in the excel budget spreadsheet as I don’t know what you will use for projected expenses.

For now we will have to manually track which means month after month we add up what we save in each projected expense category and minus what we spend so we know how much we have and what is left in each category. I have updated our personal excel budget spreadsheet for 2015.

We pay money into the projected expenses account continually throughout the year even when bills come due as its revolving so as one bill gets paid the money continues to come in from the other categories all year-long. This ensures that money is always available. It may not always be enough but having something ready is better than having nothing at all and having to use credit.

So the $1766.35 gets paid into the projected expense account every month no matter what. It seems to be easier to track our money this way but you can do what works best for you.

Projected expense example

If our clothing category was a projected expense we have a budget of $50 per month for the two of us. If we spend $30 on clothes for the month that means we need to pull $30 from the projected expenses account to pay for this expense or we move only $20 to projected expenses for the month and leave the $30 in your chequing account.

It’s up to you how you do it as I mentioned above. I’m hoping to put together a projected expenses spreadsheet to track the expenses all year-long otherwise you need to do that to make sure you don’t overspend what you haven’t saved or will save over the course of the year.

It’s a fairly easy process and becomes a lifestyle change for your finances but the most important part is that the money is available and saved, which means potentially less stress.

This means we should have $600.00 per year for clothing to spend. We have to track that expense as we spend it manually but hopefully for our 2015 budget I can incorporate that into our spreadsheet so it tallies the numbers up as we go along. That way we will be able to know exactly what we’ve spent as an ongoing total.

(Note: I am working on this but slowly as I wasn’t anticipating all of the extra hours with my second job)

Budget for May 2015

Below you will see two tables, one is our monthly budget and the other is our actual budget for the month of May 2015.

This budget represents 2 adults and baby plus all of our investments.

If it is highlighted in blue that means it is a projected expense of ours. You will also see our budget does not include the emergency savings as this is factored in at the end.

Actual budget expenses for May 2015

May 2015 Goals Reviewed

- Install garden lighting- No but I have measured how much wire I need and will be purchasing it this month so hopefully I can get started on this.

- Plant herbs- Herbs are planted and coming up nicely. Piccies to follow in my Saturday Weekend Review posts so watch out for that.

- Plant and hang the hanging baskets around the house- These are done as well. We decided to stay away from flowers this year and went with greenery since it’s easier to maintain and doesn’t make the baskets look dead so quickly. We did add some colourful flowers to a couple of planters we have on the front porch table.

- Install garage door opener signal inside the house- This has been completed and it works beautifully. The discount was well worth the wait.

- Get the vehicle cleaned inside and out professionally- This has been completed and the vehicle looks as good as new.

- Bring up all the summer furniture- This was completed and the deck has been stained and cleaned.

- Use the BBQ- YES… I have used the BBQ a few times already.

- Reach 4200 Twitter Followers- Huge PASS~

- Reach 6550 Facebook Followers- YES…PASS!! Not by much but at the rate people see posts on FB these days unless you pay for advertising is slim so that’s great news for CBB.

- Reach 2000 Pinterest Followers- PASS!!

- Reach 3100 Followers The Free Recipe Depot Facebook- FAIL but close

- Reach 170 Followers Bloglovin- PASS!

- Finish the budget projected expenses- You’ve got to be kidding me. I’ll get there I promise.

- Help a new blogger with a task or question- Yes I did that

- Connect with a new blogger- Yes I did that too!

- Finish the bathroom shower- Not a chance. I’ll be starting on it again next week.

- Pick out new tiles for bathroom and accessories (mirror, towel bar holder etc.)-Fail

- Buy remainder of bathroom renovation materials-Fail

- Buy a new blind for the garage-Fail

- Finish the walls in the baby room-Not a priority but I’ll keep it on the list as it has to get done.

- Bring the plants out if the weather is warm enough- PASS This has been completed although I lost quite a few plants this year.

- Sand and stain the deck- PASS

- Research and get quotes for a new fence and gulp… talk to the neighbours about pitching in some cash-FAIL

- Spring gardening and clean-up-PASS thanks mum and dad for the help!

June 2015 Goals

- Install garden lighting-

- Reach 4350 Twitter Followers-

- Reach 6555 Facebook Followers-

- Reach 2070 Pinterest Followers-

- Reach 3100 Followers The Free Recipe Depot Facebook-

- Reach 171 Followers Bloglovin-

- Finish the budget projected expenses-

- Help a new blogger with a task or question-

- Connect with a new blogger-

- Finish the bathroom shower-

- Pick out new tiles for bathroom and accessories (mirror, towel bar holder etc.)-

- Buy remainder of bathroom renovation materials-

- Buy a new blind for the garage-

- Finish the walls in the baby room-

- Research and get quotes for a new fence and gulp… talk to the neighbours about pitching in some cash-

- Install weed barrier, river rock and mulch in back garden-

Budget updates month by month

In case you missed our budget updates and want to do a quick search I’ve compiled them all on one handy page: monthly budgets.

For the 2015 Year I will also keep track of each month just below.

I will start the list off with our end of year budget update from 2014 just in case you missed it.

That’s all for this month check back at the beginning of May 2015 to see how we made out with our June 2015 budget!

Happy Budgeting CBB’ers!

Are You New To Canadian Budget Binder?

- Find me on Social Media by clicking any one of the links below

- Check out my new Free Recipe Index

- If you like FREE then click this link for my FREE Excel Budget Spreadsheet and all my Free Money Saving Lists!

- You can now have full access to my Ultimate Grocery Shopping Guide in Canada.

It is nice that it is one whole year now mortgage free for you!!! Ours come up for renewal this fall. Not looking forward to that. Paying off that was important to you so that makes it the right thing for you to do in my books. We all have to do what makes us comfortable and that is just what you did. It has freed up funds for other uses and with your son now there are different priorities in life to be dealt with.

There will always be a to-do list to be worked on and we all have them. Good to hear your gardens are doing well. I have my 4 tomato plants in their grow bags on the deck and they look happy. Time will tell but I’m hopeful. I still have to get my few seed potatoes planted in grow bags yet but that will likely be by the weekend or do, weather permitting. The grow bags were easy enough to make using landscape fabric. If I get 2-3 years out of them I will be happy. We don’t have the room for a big garden but this is working so far. As well the weeding will be as the weather permits. I don’t do well in the hot sun so I pick my times to be outside working.

Hi Christine,

I wish more people had your mindset especially the one’s who are buying these McMansions because the interest rate is low. I pray that the day doesn’t come when they get the scare of their lives. It’s better to air on the side of caution with money but with risks. If you risk it all you must be prepared to pay the ultimate price.

The gardens are doing well, but like I mentioned we lost lots of our potted plants this year. We won’t be creating many more as we don’t have the time with the baby now to look after them. Once he gets a bit older we will do it again. I pray my wife’s fig tree comes back this year or I may be in the dog house over that one. lol.

Congrats on being 1 year mtg free! My mortgage is by far the biggest line item in my monthly budget and it’d be nice to be rid of it, but first I have to pay off the rest of my credit card debt.

Thanks Kayla!

How long until you finish paying your CC debt? Do you currently use a budget?

Wow, that is some serious net income. And congrats on being mortgage free, I can’t wait to get rid of our mortgage in the future

Thanks, we have been posting our actual budget and net worth updates in 2 separate posts since the blog started. It’s been fun to watch how things have progressed over the years.

It does feel good saving when we have no mortgage or credit cards or student loans to deal with. We can save as much as we can and we want as long as those basic needs are meet. And, one more thing is that it stops us from being in depth when our priority is saving for the future.

I think that’s part of what we did, we thought about our future which helped motivate the present.

Wow – no mortgage payments. Good for you! That must be a great feeling!! We have been free of our vehicle payment for 5 years now and I remember how great that felt. I don’t think we’ll ever buy a vehicle on credit again. It is crazy to think how much you ACTUALLY pay for your house over the full 25-year loan. Prior to baby we were aggressively paying our house down to, but then maternity leave hit and now I’m only back to work part-time. Hopefully with my newfound resource for couponing and budgeting 😉 , we will be back on track to have our house paid off before we turn 40.

That’s awesome Megan!! I know my wife bought a new vehicle although it was 0% interest but she sure was happy when she paid that off. Paying off the mortgage is one heck of a feeling and by the sounds of it you will feel that soon enough. Good for you. How long have you been budgeting now?