{kind=link}

Estimated reading time: 14 minutes

Financial freedom requires understanding your retirement needs. From creating a Will to investing, learn how we plan for retirement.

Our financial advisor told us once that our retirement savings plan looked suitable for our age.

We won’t know the future until we arrive, but planning today for tomorrow is critical, even if life is not guaranteed.

However, we knew there was a long way to go before we’d feel any thrill about our retirement plan.

Two Of Life’s Predictions

It’s hard to get excited about financial freedom when you don’t know what you need.

We knew we needed to keep our finances in order and ensure we had a legal Will.

They say taxes and death are the only certainty in life, and it’s true.

Most of my colleagues don’t often talk about retirement because we want to work and use our expertise, as this is what we want to do with our lives.

I remember working dead-end jobs or jobs I hated; retirement sounded good every morning, before and after coffee.

Retirement may not be a hot topic at work, but I’m sure behind-the-scenes money is being saved for when the time comes to say hello to a new way of life.

I’m only a newbie, so I suspect some long-standing employees make more than six figures yearly and have a decent defined retirement savings plan.

Debt-To-Income Ratio

Even though a significant income may be impressive, it may also mean lots of debt.

It’s just another way to calculate a debt-to-income ratio to understand better where one stands financially.

I’ve always credited myself for wanting a career I love over accepting a position just for the money.

I want to love what I do because the money is just a bonus to do stuff with.

This is why I work as hard as I do now, hoping the future will look brighter for my family.

You never know the dark secrets that lurk behind the eyes of success

Your income does not equal what you are worth.

It never has been and never will be because earnings are just numbers.

What you do with that number counts, especially when working out a retirement savings plan for down the road.

Preparing For The Worst

Those who work from home or own a business are not safe from the perils of losing grip on employment reality either.

You may be the boss, but with that comes even more responsibility.

Everything can come crashing down in an instant, and then what?

Many businesses did not survive Covid-19, and nobody was ready for that.

We all have to think ahead if we want to be somewhat prepared or face the consequences of the unknown head-on when it gets to us.

Should I Retire Early?

Since our son is so young and I’m no longer in my 20s or 30s, spending more time with the family would be great, even if I retire in the next ten years.

By then, our son would be coming up for 12 years, and we’d have the world at our fingertips.

We love to travel, even if it is a short road trip, but if I were to retire early, we’d have every opportunity to see the world.

That all sounds groovy, but then what?

Don’t get me wrong, I love leisure time and the potential to never work again or work for myself building this blog.

When you love what you do, it’s hard to say goodbye, especially when you know you are making a difference in many people’s lives.

For example, Mrs. CBB’s uncle still works as a lawyer in his 70s because he loves what he does.

Things I Don’t Want To Do During Retirement

- I don’t want to sit on a beach all day.

- I don’t want to golf.

- I don’t want another dog.

- I don’t want to travel non-stop.

- I don’t want to garden all day.

- I don’t want to renovate all day.

- I don’t want to blog all day *, haha, just kidding; I love blogging)

Not everyone will agree with my choice, but maybe you don’t like your career as much as I do.

I want to do what I set out to do: be the best I can be in my chosen career.

Would a doctor retire early after spending countless years and hundreds of thousands of dollars on school?

Probably not, and besides, the money is so lucrative.

Why would you stop doing something if your body tells you to keep going and you’re happy?

Retirement Plan Wants

- I do want to be successful in my career.

- Seeing my wife and son happy and spending time with them is essential.

- I want to provide financially for my family until the end.

- Most of all, I want to do what makes me happy!! If I’m unhappy, shifting positive vibes onto others is hard. It would be best to take care of yourself first, especially your health and well-being.

I see many retired people, especially in our neighborhood, who have a good pension and cash in the bank but are bored with life.

What you learn by taking the time to talk to older people who wish to have more company in their lives is amazing.

They are the best conversations.

Some of them golf or go on trips but for the most part we see them around the house puttering about.

They may enjoy this, but I wouldn’t, at least from my current age and perspective.

Maybe they aren’t investing enough into their day or maybe that’s all they can carry out due to health reasons.

I’m not sure what I’ll feel like in 10 years time so what I don’t think I’d like now might drastically change then.

In the meantime, I will ensure my retirement savings plan is in full swing so I have options when the time comes to decide whether to continue working or sleep a little longer every day.

Retirement Savings Plan

I’ve only lived in Canada for (honestly, I have to count every time I post this) coming up 9 years now, so investing in my retirement savings plan has been slow.

Remember that when I was earning $15 an hour in Canada, I contributed to my work retirement savings plan and very little to a Registered Retirement Savings Plan (RRSP).

Since I’m earning far more, I wasn’t earning enough money to sock away the cash I have started today.

This means I have lots of unused savings room, which I will hopefully catch up on by the end of 2016.

In June 2017, our net worth was estimated at around one million dollars, but honestly, a million dollars doesn’t get you much these days.

We paid our house off early and have been living frugally and saving money for today and tomorrow.

Related: How we became mortgage-free in 5 years

Securing A Financial Future

Although I may have a pension plan back home, I need to secure our financial future in Canada now while I still can.

Since Mrs. CBB is now a stay-at-home mom, it is even more critical for us to worry about our future savings.

A million dollars today is hardly anything, so even though it may seem a lot, that perspective always changes depending on where someone lives.

Unless we sell our house, which, on a positive note, comparable houses sell from $450-$500,000, our net income may increase. (We left our house estimate at $345,000).

If we were to move to a smaller town, we’d spend less on a house and have more for our retirement savings plan.

It seems like a legitimate thing to do, but then we think about our son, who may enjoy the bigger city with all the amenities nearby.

He’s still young now, and we know we have options, but we’re staying put in our current home, which we love.

If we don’t sell the house, that leaves us less than $345,000 of our current net worth, which is tied up because we need somewhere to live.

The good part is that we could downsize if needed, so we include it in our net worth update.

This only means we must work harder on our retirement savings plan so the money we do have on hand is liquid.

How Much Retirement Money Is Needed?

Your guess is as good as mine, so I’ll keep working, saving, and smiling for now.

I’m happy with life even though I’m always tired.

It’s certainly amazing what some people can live from when faced with few options.

We don’t need as much as we think to get by, but if you want to travel the world without worry, you may need a beefed-up retirement savings plan.

When the time comes and a retirement early option is available, and if our retirement savings plan is golden, maybe I’ll consider stepping away early.

Only time will tell, but don’t wait until it’s too late to invest in your future.

Nothing is ever guaranteed.

Discussion: Do you worry about your retirement savings plan and whether you are doing enough now for tomorrow?

Please leave me your comments below.

Thanks for reading,

Mr. CBB

Now, on to our Net Worth Update for the month.

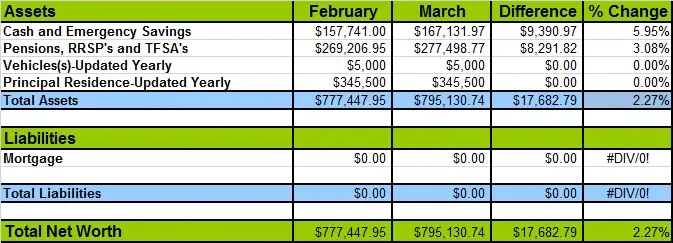

Net Worth 2016

RESP Contribution 2016: $208.33 a month.

Changes to our Net Worth in March

Absolutely nothing extraordinary happened this month.

The gains were due to increases in our investments, which got a little rebound from a mild improvement in the markets.

The markets have been so hit-and-miss lately that a guaranteed return is hard to predict.

We’ve taken a couple of hits in the investments over the last year, but nothing that the rebounds couldn’t compensate for afterward.

Seeing a steady monthly increase and watching our money work for us would be encouraging.

Unfortunately, investments always have their ups and their downs. Any costs this month went to living expenses almost exclusively.

We haven’t had the time to spend much on ourselves.

Understanding Net Worth

What Does Individual Net Worth Mean?

Net Worth is a snapshot of your financial health, like a picture of debt to net assets.

In simple terms, it’s a total of the value of your assets minus your liabilities.

We credit our net worth growth due to patience, perseverance, using a monthly budget, and not giving up.

Your numbers may go up and down, but don’t let the numbers scare you. Rather, understand why and move on.

If you would like to use our budget, I offer a FREE downloadable budget I created that you can use at home just like we do.

Canadian Budget Binder offers many other free printable lists to help you achieve some of those financial goals and build your net worth.

Now… what you need to do is determine just how much net worth you have and go from there….

Determining Net Worth

Figuring out net worth is fairly easy as long as you know your numbers or monthly finances, so you must do your homework.

Net Worth is simply adding up all your assets (what you own) and then taking away your liabilities (what you owe), giving you a net worth number.

Understanding your net worth will help you determine if you are on track to meeting or beating your personal financial goals. It doesn’t get any easier than that.

Net Worth = Assets – Liabilities

Calculate Net Worth

Do you know how to calculate your own Net Worth?

Now you can stop asking yourself the question, how do you find out your net worth?

It’s easy to determine. We like calculating our monthly net worth to know if we are still on track.

Some people calculate it yearly or quarterly.

It’s really up to you and how informed you want to stay regarding your financial health.

Net Worth is essentially an estimate; not everyone uses the same figures.

Some people don’t include vehicles like we do or may leave out the assets inside the home as we have.

It depends on what you want to calculate or what you can sell today and make money on.

Why not go ahead and calculate your own using the CBB Free Money Saving Tool,

Net Worth Calculator (Canadian Budget Binder)

Why You Should Set Goals

Setting goals is the only way we work towards achieving what we want to be done as a couple around the house and in our financial lives.

Without them, we would be flying by the seat of our pants, which wouldn’t work for us.

I find it’s much easier to be held accountable when I share what we need to do with all of you.

Mrs. CBB refers to the list when she asks what I plan to do next.

I’m not sure if that’s a good thing for me or not.

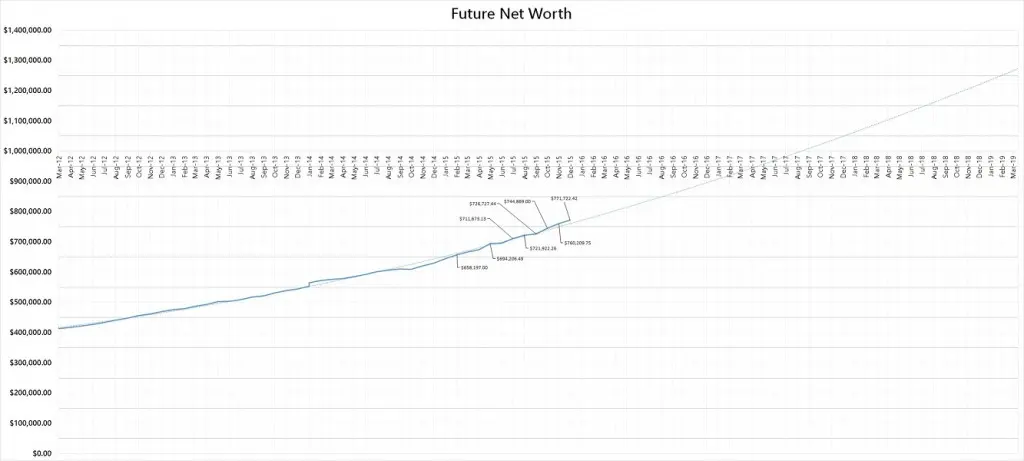

In the graphical representation below, I have used Excel to provide a prediction based on the past year’s monthly net worth figures.

Using figures from our actual net worth gains over the past 12 months (the solid blue line) it has suggested that by the end of this year (2016) we should be just shy of $900,000.00.

This can change over the years and is only a prediction based on known historical figures from our finances.

According to the chart, we should hit the million mark in June 2017.

This is nice to know, but anything can happen over the next year.

Hopefully, with careful planning, we can achieve this goal and go beyond it.

Do you set goals for the year?

CBB Financial Numbers

When budgeting, anything is possible, we are proof of that, although we still have a long way to go in our journey.

These are our numbers and goals, not a means of comparing your own goals and other’s target goals.

We don’t care how much money others make or if they have a high net worth, or if it is lower than ours as it’s not a competition.

I hope our experiences perhaps will help guide you along your financial path working towards debt freedom.

Different Financial Paths

Not everyone has the same path in life. Some of you may have had to start over like I did or go to school again and now have OSAP loans to pay back.

Others may have divorced, lost money in the stock market or other investments, suffered job loss, fell ill, etc., but you can’t let that stop you from achieving your financial goals.

Some of you may have been given trust funds, paid-for homes, paid educations, or perks in life that give you a financial kick-start, and that’s OK, too.

Remember, “It’s not about how much money you make; it’s how you save it.”

Focus on yourself, and don’t let the evil eye of money jealousy or keeping up with the Kardashians cloud your vision.

No one cares about your money as much as you do, so don’t waste your energy trying.

People accumulate wealth only because they know how to save or invest it wisely, even if they inherit money or win the lottery.

The smallest improvements should mean big strides in working towards reaching your goals.

Sometimes we have to fail to learn, and we’ve all been there.

Money can be an evil force for some people, especially those with a negative attitude towards their financial situation.

I urge you to be optimistic, and little by little, with determination, you should see improvements if you want that to happen.

Net Worth Updates

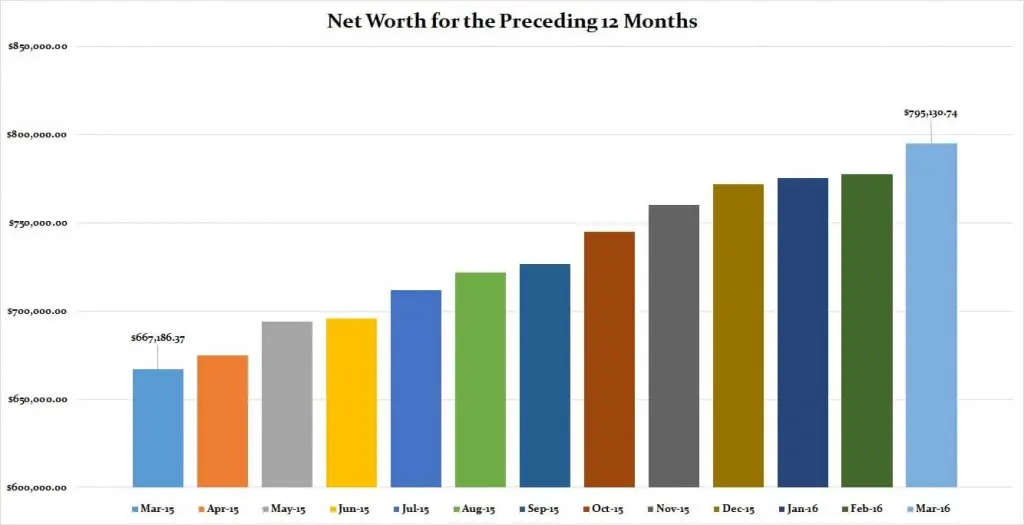

Below, you can click the links to read past 2016 net worth updates to see if we were on target or struggled with some of our numbers.

In the last year since March 2015, our net worth, according to our figures, has grown by $127,944.37

March 2016 $795,130.74 – March 2015 $667,186.37 = +$127,944.37

That’s all for this month’s net worth update, but please check in at the beginning of April 2016 to see how we made out in March 2016 and what has happened to our finances.

~Mr.CBB

Check out our past actual Monthly Budget Updates to see how much money we earned and where the money went for the month.

I’m curious about your cash and emergency savings line. $167K seems like an awfully large number to me. A common guideline for an emergency fund is 3 – 6 months worth of your household’s expenses. Without a mortgage, I would be inclined to think that your emergency fund would not need to be very large. So, are you saving up for a major purchase? Or is a significant portion of that money earmarked for your RRSP? If so, what’s holding you back from making systematic contributions right now (or from having already started several months ago)? You appear to have the available cash. I’m personally a big believer in automating RRSP contributions. My wife and I make monthly contributions and adjust the amount each year at around this time when the Notice of Assessments arrive. My apologies if you’ve already explained all this in an earlier blog post.

Let me also add that I agree that tracking household net worth is a worthwhile exercise. I started tracking ours in earnest about three years ago, and by digging through old records (including a bit of guesswork here and there to fill in the gaps) have set up a spreadsheet showing annual net worth going back to 1996. It’s rather encouraging to see that upward curve over time.

Thank you for the comments, it’s always good to hear other peoples opinions. Some of the money is earmarked for RRSP’s, the only reason it’s not gone in sooner is because it’s only the last 12 months that it’s worth while paying in to it for tax purposes. There will also be a large chunk going into my TFSA this coming year. Some of the rest is to pay for renovations I have yet to get into because of working 2 jobs. A basement to build up from nothing, a new kitchen and a sunroom revamp are just a couple of things that need to get done.

Looking good there!!!

One thing to consider about your retirement would be that now is the time to cultivate hobbies you enjoy. We saw this one with my late father-in-law. His life while working was work/drink/party for the most part. He took an early retirement back late 70’s to early 80’s (can’t remember the exact year)when GM offered it and found he had no hobbies so he was bored senseless….. He did buy into a cottage group with his brothers an a few friends/drinking buddies around then but it didn’t change much. There was some puttering around the cottage during the summers with a lot of drinking going on. He and Mom would be up there most of the summer as it took quite a while to get there as it was on Manitulin Island and they took the ferry over. The trip there or back took care of a day by itself. We went a few times over the years but the fact it took so long coming and going meant there were no trips up for the weekend type of thing. Plus I don’t have much patience dealing with drunks…sorry. My sisters-in-law sold the place after Mom and Dad died. So consider any hobbies and such as part of a retirement package.

Hi Christine,

I agree and once I sort out this employment situation of mine you can bet everything is going to be full-speed in our house. We are planning a trip to Europe this summer. Travelling used to be a hobby of mine and my wife loves to travel so we’re going to take a break from everything.

I do worry that we are not saving enough for retirement. We really started saving for retirement around age 30 (buying RRSP’s and I joined the pension plan at work). We have built up a decent amount in the last 15 years but I am concerned we did not start saving early enough (especially when you read all those articles about the magic of compound interest).

It has been helpful that we automated our savings. Our RRSP contributions come right out of our account right after our cheques go in. We have learned to live on what is left. We have concentrated our savings in RRSP’s to take advantage of the tax savings but by next year I will “catch up” to my limit.

When our mortgage is paid off in July we plan to contribute an amount equal to the mortgage payment right into a TFSA. We still have lots of unused TFSA contribution room.

We are aiming for retirement at 60. When I put our numbers into those retirement calculators it seems like we will be OK, but I still worry.

I really like your blog and what you are saying. I see some many of the “Retire when your 40 or 30” blogs that are crazy. Who wants to sit around for 50 years in retirement with no money? There is a balance between retiring early and not retiring at all. I’m 55 and should retire soon but want to work part-time. Not really full retirement I guess.

Saving more always helps, but there are limits. Make sure you have a life when working. I don’t know what you invest in but get some good solid dividend stocks and reinvest the dividends, or high-dividend ETFs. I really like SPHD. Even for a tax differed account this is a good plan. Companies with increasing dividends seem a bit boring, but should the market tank, you’ll be happy you have those companies. Bond funds are fine for maybe 30% – 40%. This is your emergency fund too.

I WOULDN’T count your house value as retirement funds. What your house is is a long-term care policy. If you have too, you can sell it and move to an apartment, but not until you can’t manage it anymore or need the money (health problems).

Stick to the plan, and set yourself up for a market crash NOW. Then if it happens don’t panic.

Hi,

I agree there are limits when saving money and working. I’m working on getting my dream job which will free up about 40 hours a week for me. Right now I’m on the fast train to get where I want to be for the next 25 years. I agree about the house value as retirement funds which so many people do. We do factor this into our net worth calculations only because if need be would could move, sell and downsize. I love the idea of setting yourself up for a market crash because if we aren’t aware of how it will affect us if it does happen and certainly may then we we’re in big trouble. Thanks for dropping by mate and for your kind words. Cheers

When I am older than 60 years, I still want to work more. I don’t want to stay at home or somewhere else. I just want to continue my lifestyle as much as I can while still enjoying my retirement savings.

I think for many people they want to keep busy and working doing something they love would be optimal. Thanks for popping by Jamie.

I really like this article. I especially liked how you spoke about retiring at 30 or 40. With life expectancy increasing I cannot fathom doing nothing for 50 or 60 years. Also, unless you are making millions at these ages it may not even be feasible to retire so young as Healthcare is rising along with many other cost. You made a good point by saying find something you love. Doing what you love makes retirement a fear instead of a goal and I hope to find this as I embark on my career!

I am a new reader to your blog and am really enjoying all the information you are posting especially about retirement. I am from Canada but currently living in Korea with my husband. Here they only have pensions nothing else that will help you retire and it is worrying me quite a bit. My husband who is Korean is never worried about retirement as he sees property as being your retirement and usually children take care of their parents here. Eventually we will move to Canada and I can’t help but wonder how far behind we will be in retirement.

Have you had this conversation with your husband? How old are you both? Will your children take care of you when you move to Canada? If the answer is no then I would consider your retirement seriously. Maybe chatting to a financial advisor in Canada might give you some insight into what might work best for your situation. The one thing I never do is rely on anyone to fund my bank account. Welcome to the blog! I hope to hear how things go for you.

My husband is 72 & still working. He is a welder & works in heat or cold. He has no plans of retiring.

He goes to the VA & he takes no medicine & nothing is wrong with him. I call him a workaholic. Lol !

He loves what he does. He says he’s not going to retire & sit down & grow old. Lol !!

Hey its working !! Everyone needs to think about how they plan to fill all those free hours. Better have enough money for sure or a great marriage could be strained. People have to look at the whole picture & get all their ducks in a row.

Hey Donna,

Thanks for popping by. My wife’s uncle is also in his 70’s and is a lawyer. He essentially said the same thing about sitting around even though he has money to travel. There’s only so much you can do too and he loves his job. I agree about the marriage. So many people say it’s not about the money but in the end most often, it is.