PAY ATTENTION TO THE NUMBERS

It’s inevitable that mistakes will happen whether they are by human error or computer generated mistakes that for the odd occasion can cause problems when it comes to your finances.

How to pay your bills?

There are so many ways to pay your bills these days whether it be in person to the organization, at the bank, with a credit card (for points), online bill payments and I’m sure there are a host of other ways to pay your bills.

The key is to pay them once and to pay them on time while making sure you are paying for the services you used.

We have a bill payment calendar set up on the computer in excel so we know exactly when our bills are due and the general amount they are unless they are fixed as that would be the same amount such as the mortgage payment each week.

Just when we thought we were an organized couple financially we go and make an error this week that I wanted to briefly touch on this month because for some it may not be a huge deal but for those that might have limited funds it may be a huge deal.

Bill payments

When the bills come due we have always been pretty strict about paying them on time to avoid any form of interest or late fee charges which is money blown out the window in our opinion.

Typically one of us pays the bills each month and we look over our payment calendar and then head to the appropriate website to view our bill, the payment and the due date to double check the information. After that point we make monthly payments for the most part based on that data and everything works out fine.

I know all of you that have your bills automated are shaking their heads thinking that this is far too much work and you would never do it and that’s fine we enjoy manually paying for our bills.

The automated bill payment services definition to me means that whatever they deem your bill to be during a particular period in time they will remove that money from your bank account because you have allowed them the access to do so.

We were never big on allowing companies to pull out money from our bank without us first reading the bill and making sure the numbers all made sense.

Most of the time in the UK I paid each bill individually by cheque as and when it arrived in the post. This then got gradually changed over time to direct debit as most UK companies ran a scheme where they would give you a discount if you signed up. It’s a shame they don’t run a similar scheme here, I’d be all over that.

If you are someone who lives pay cheque to pay cheque or doesn’t have enough money to get to the end of the month or to pay all of the bills an extra bill payment, an incorrect bill automated or doubling up by accident manually could mean big consequences in the form of extra fees, cancelled services or even to your Canadian credit report which you can order once per year for free.

The issue

A Reliance energy online payment was made twice by accident this month because we not only received the bill in the mail we received the email prompting us to pay.

We were so busy the past few weeks that it slipped our mind that the bill was paid. Now, we could add a feature in our budget to show us that our bill has been paid which I may end up doing to stop that from happening again or I can add something to our payment calendar although I do like the thought of the information being available at the budget level where we spend most of our time each week adding data.

What should we have done?

Well, common sense dictates that we should have checked our bank account first to see if the payment was made but we failed to do that. I guess we just weren’t thinking with our thinking caps were we but that’s ok mistakes do happen.

It only taught us that we must be more diligent and organized when it comes to the bill paying process otherwise simple errors like this could happen again even though the money will be credited to our account.

The problem is now our money is not working for us it’s working for Reliance which is what we don’t want to do. You may think $116 is not lots of money but what if the bill was much higher. Sure we could request to have the money transferred back but I’m sure they would charge us for this reversal and it might take time.

If you rely on every dollar in your bank account this could be a costly error. Then again if a company over-charges you through an automated bill payment it may also be costly and take time to sort out.

How about if you have an automated pay from your employer and you are short changed? It’s imperative to read, read, read and keep organized. Automation is not free from error and you are your own quality control manager of your financial account.

Will we ever win?

Probably not but the best defense is to stay organized, read any bills that come in thoroughly and stay on top of our finances so we don’t run into this issue again.

So, Reliance now has 2 bill payments made online through our bank which means we are paid up for the next 6 months not including the increase of charges starting in 2014 which we will still owe.

Have you ever paid your bills twice by accident or had an automated bill payment with incorrect figures which cost you more money then you were supposed to pay and was debited from your account?

Get your free budget

I’m currently offering 2 versions of my budget and the reason behind it is simple. Firstly, read the disclaimer because what you do with it is your own business so if you mess it up you need to sort that out.

I have not closed off any cells so you can make all the changes you like to the budget to reflect your lifestyle which is what the fans wanted.

Although I would love to help every single fan with their budget I am unable to do so but I am always willing to answer any emails you send me so don’t be shy.

The 2 Budget Spreadsheet versions are as follows below but I will be updating the below budgets for the 2014 year in December based on any issues that might come up from all of you so please take a moment to download the budget of choice and let me know how it goes and any further feedback you can give me.

I’m always open to feedback but be polite as you don’t want to hurt my feelings lol. I’m a sensitive guy you know.

This was after all meant to be our personal budget and although I would love to customize it for every fan that wants to use it but, I’m afraid I cannot.

I’m not selling this budget or hope to make any money from it so enjoy this free budget and I hope that it works for you as much as it does for us.

Canadian Budget Binder Budget Spreadsheet

You can download the free budget spreadsheets here.

- Budget 1– You can use the pre-existing categories or you can use your own if you wish and you have the option to use projected expenses or not. Please read all notes left around the budget for tips.

- Budget 2-Everything is pre-set so you have to use the pre-defined categories but this budget will generate year-end budget figures whereas the other one won’t but you must use the categories already in this budget. If you change anything you will mess up the formulas and year-end figures. Please read all notes left around the budget for tips.

I’m always open to feedback but be polite as you don’t want to hurt my feelings ![]()

Get started and don’t procrastinate. Test it out for a month and see how it goes.

There is never any harm in trying something new in life. You either love it or hate it, that is a fact with anything.

What type of budget do you use?

Our budget plan

How we budget our monthly expenses

I often have fans ask me how to budget money and what we do in order to save so much money but the reply is that it’s not about the money it’s about the process involved. We don’t always save as much money as we would like every month but most importantly we are not going into debt because we are budgeting our money.

One of the most important things we did for our personal finances was that we never let the budget deter us from reaching our goals. Sure we’ve had crap months but we made up for it or we learned from our mistakes just like anyone else would.

Budget failure only occurs when you give up on the budget which should not happen as long as you give 100% into making sure you reach your goals. Sometimes fans email and ask me if living on a budget in Canada is any different from living in other countries. To be honest I’m going to say, probably not. If I still lived in the UK I could use this exact budget to meet all of my needs. Below are links to the budgeting series which I wrote while designing our spreadsheet.

I’m not a financial planner/advisor so I can’t tell you how you should budget but I can show you how we budget. I’m just a regular guy just like everyone else; some might call me a budget nerd. Please take the time to read through the budgeting series and I hope you take something away from the information.

- How We Designed Our Budget Step 1– Gathering All the information

- How We Designed Our Budget Step 2– Categories

- How We Designed Our Budget Step 3– Tracking Receipts

- How We Designed Our Budget Step 4- Note-taking

- How We Designed Our Budget Step 5– 5S Organization

- How We Designed Our Budget Step 6– Who Does What and When?

- How We Designed Our Budget Step 7– Balancing Our Budget

- How We Designed Our Budget Step 8– Knowing our Coupon Savings

- How We Designed Our Budget Step 9– Reading Our Bills

- How We Designed Our Budget Step 10– Projected Expenses

Budget changes

The only real changes to the budget this month came in the form of our telecommunications bill once yet again. When the bill came in we found out that we went over our long distance usage on the cell phone since I was away. I will talk more about this topic in my Wednesday post so you can read about what went wrong and what we’ve done to change our bill.

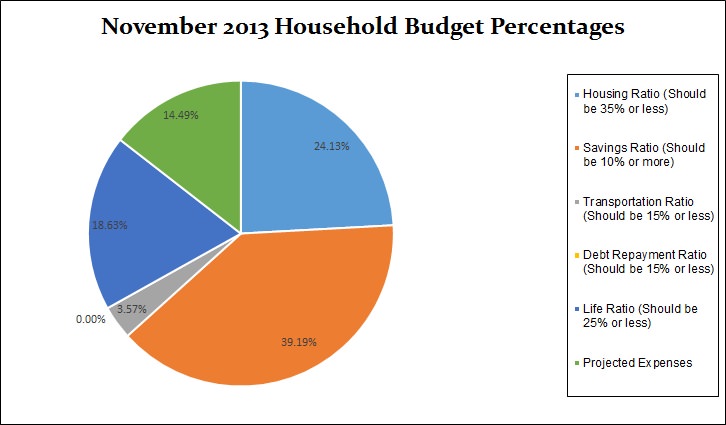

Budget percentages

Our savings of 39.19% includes savings and investments. I’ve also went ahead and added in our projected expenses this month at 14.49% which brings the total November 2013 Household Budget Percentages to 100%

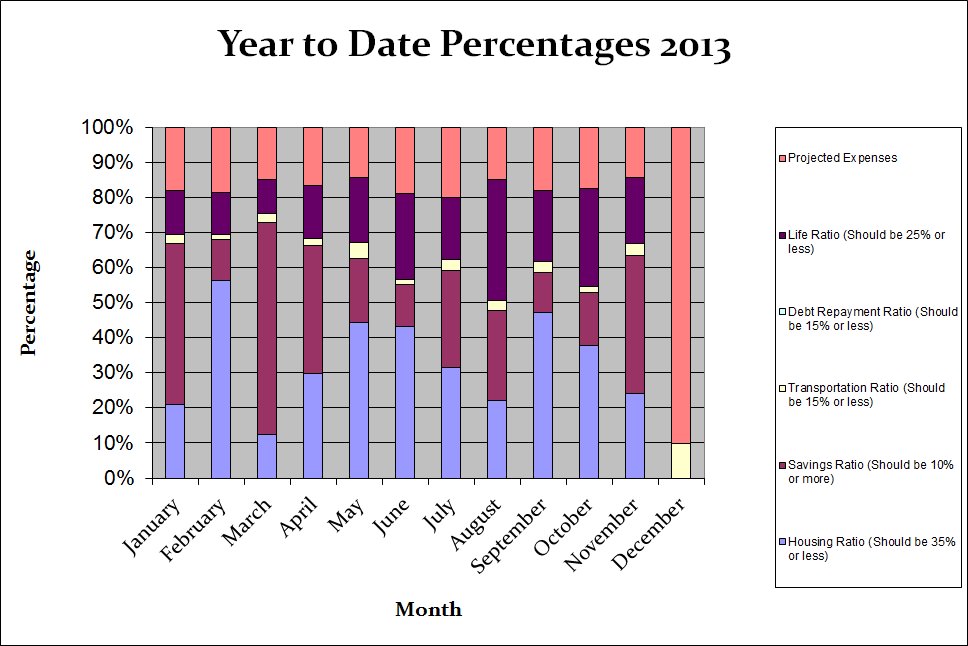

Budget percentages month by month

Expenses breakdown

This is simply a breakdown of our expenses which has helped us to understand where all of our money goes. I appreciate that you enjoy this budget update each month but I do hope you view this as an educational tool rather than comparing your own financial numbers as we are all unique. Sometimes we wish we had more money to budget with but understand that we only have what we earn and if we want more, we need to earn more. Spending less than we earn and budgeting our money has been the easiest way for us to pay down debt and save money.

- Chequing– This is the bank account where all of our debt gets paid from.

- Emergency Savings Account– This is a high-interest savings account.

- Regular Savings Account– This is a savings account that holds our projected expenses.

- Monthly Budget Total: $4400.18

- Monthly Net Income Total: $8209.33

- Total Coupons Used: includes every discount attained during the month = $55.96

- Projected Expenses: These are expenses we know we will pay for throughout the year = $1189.14

- Total Expenses Actually Paid Out: $4611.49

- Total Expenses Actually Paid Out: Calculated is $8209.33 (total net monthly income) – $2408.70 (emergency savings) – Projected expenses $1189.14 = $4611.49

- Actual Cash Savings Going Into Emergency Savings: Calculated is $8209.33 (total monthly net income) – $4611.49 (actual expenses paid out for the month) – $1189.14 (projected expenses) = $2408.70

Saving money

What are Projected Expenses? – We project expenses throughout the year so we have the money saved.

PE= A projected expense is money which is automatically saved each month so it is ready when the bill comes in or when you need it as in the example below. We review our projected expenses at the beginning of the year to set up our yearly budget and adjust as we go along if a new projected expense arises and needs to be added to the budget. Sometimes we remove a projected expense as well so it’s very important to keep an eye on your expenses.

This has happened on many occasions but it’s bound to happen as we can’t predict everything we have to pay for over the course of the year. The important part for us is that we are saving for these expenses and we no longer have to stress about taking money from our savings to pay for them. To learn more about projected expenses read Step 10 in my budgeting series.

When we spend the money in a projected expense category we move that money to our chequing account in order to pay for that incoming expense. We pay money into the projected expenses account continually throughout the year even when bills come due as it’s revolving so as one bill gets paid the money continues to come in from the other categories all year-long. So the $1189.14 gets paid into the projected expense account every month no matter what. It seems to be easier to track our money this way but you can do what works best for you.

Projected expense example

If for example our clothing category was a projected expense we have a budget of $50 per month for the two of us. If we spend $30 on clothes for the month that means we need to pull $30 from the projected expenses account to pay for this expense or we move only $20 to projected expenses for the month and leave the $30 in your chequing account.

It’s up to you how you do it as I mentioned above. I’m hoping to put together a projected expenses spreadsheet to track the expenses all year-long otherwise you need to do that to make sure you don’t overspend what you haven’t saved or will save over the course of the year.

It’s a fairly easy process and becomes a lifestyle change for your finances but the most important part is that the money is available and saved, which means potentially less stress. This means we should have $600.00 per year for clothing to spend.

We have to track that expense as we spend it manually but hopefully for our 2014 budget I can incorporate that into our spreadsheet so it tallies the numbers up as we go along. That way we will be able to know exactly what we’ve spent as an ongoing total.

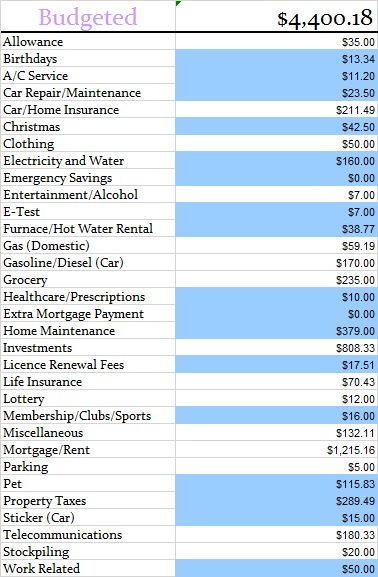

Budget for November 2013

If it is highlighted in blue that means it is a projected expense of ours. You will also see our budget does not include the emergency savings as this is factored in at the end.

Actual budget expenses for November 2013

December 2013 goals

- NEW! Update 2014 Canadian Budget Binder Budget Spreadsheet

- NEW! Reach 1350 Pinterest Followers

- Get organized with blog activities

- Learn more about affiliate marketing and blog advertising

- Complete and search out more freelance work

- Read more in my personal finance book

- Sort out and pay mortgage in full

- Move my money to Canada (watching exchange rate)

- Reach 6300 Facebook Fans

- Reach 2200 Twitter Followers

- Reach 1275 Blog Followers

- NEW! Make a pin for my universal weight machine

November 2013 goals

- Change vehicles for winter and swap to winter tires- PASS

- Put up Christmas decorations outside after Remembrance Day-PASS

- Get organized with blog activities- Somewhat FAIL

- Learn more about affiliate marketing and blog advertising– FAIL

- Do more freelance work (HIRE ME)- I did write one article but would like to do more

- Read more in my personal finance book- FAIL

- Sort out and pay mortgage in full- It has to be done by April 2014 but that exchange rate keeps going up …. decisions.

- Move my money to Canada (watching exchange rate)- see above FAIL

- Reach 6300 Facebook Fans- PASS (6327)

- Reach 2150 Twitter Followers- PASS (2214)

- Reach 1250 Blog Followers- PASS

- Start to tear main bathroom for renovations- PASS

- Train for 10k run and get my time down- Working on this

- Organize the basement- Working on this

- Plan the kitchen and double-check measurements and go to IKEA- FAIL

In case you missed our budget updates from the start of the year I will list them all here each month.

- January 2013

- February 2013

- March 2013

- April 2013

- May 2013

- June 2013

- July 2013

- August 2013

- September 2013

- October 2013

That’s all for this month check back at the beginning of January with our 2013 budget overview of the year and hopefully a 2014 budget update and who knows maybe some good news.

Are You New To Canadian Budget Binder?

- Follow Me on Social Media: Twitter, Facebook , Pinterest , Stumble Upon, Reddit and Google+

- Don’t forget to Subscribe to the blog so you get my daily email.

- If you need to get in touch with me the best way is on Facebook.

- Check out my new Free Recipe Index

- If you like FREE then click this link for my FREE Excel Budget Spreadsheet and all my Free Money Saving Lists!

- Check out my new Free Recipe Index

Related articles

- How To Overcome Laziness And Save Money In 5 Steps

- A Payday loan cost me double time

- A Man’s Ego and his Budget

- Tic Toc…. That’s the sound of your debt clock

- Family Finances: Somebody Is Watching You

- What My Life Is Like With Terrible Credit

- How I Reduced Our Grocery Budget From $1100 To $600 In 6 Months

- There And Back Again: A Spenders Financial Journey

I do pay bills automatically to ensure we pay on time and avoid any late fees. But like you said, there isn’t always a fail-proof plan. So many people do automatically pay bills, which on one hand is good – no late fees, but on the other hand, they rarely look at their bills and may miss errors or rate increases. Companies, of course, hope we do this so we don’t balk at increases and complain or leave them. I still try to make sure I look at the bills to make sure they are correct. And yes, I have paid a bill twice before. 🙂

I pay everything via direct debit. They rarely make a mistake and if they do, you just cancel the DD until they correct the mistake and they’ll be quick in doing it.

We pay some things with our credit card to get points.All of our bills are automatically paid each month from our on-line bank.

I have set up the amounts and dates of the payments, and I can change them at any time.Only the mortgages come out automatically. For bills like electricty, we go on a budget plan. I still pay extra each month anyways. The worse that can happen, I have a credit at the end of the year.That’s better than owing them.

Most of our monthly bills go on a credit card, so that usually works out well. However, we have paid our rental’s sewer bill twice before and felt really stupid.

Pretty much all of our bills go the automatic route. We have to pay MasterCard, Rogers and the Redi-line ourselves and hubby does those online. We get a paper bill for everything except M/C and Rogers. Those we have to run down online along with the bank statement. Not too happy about that!!! What we do is have everything in a drawer here. A paper bill comes in and gets parked in a clip labelled- To Be Paid. Once it’s paid (by us or automatically) the bill goes into the other clip…Paid. The next month’s bill comes in and we repeat the cycle with the old bill pulled and shredded. Things like the truck garage bills we pay and then the bill flips from one clip to the other. The ones we pay online we get a reference number from the bank to say we paid it. That number is written on the bill itself and in the chequebook register as the bill is paid. I run through the bills every Thursday as that’s when we take the weekly mortgage payment out. Might look a little crazy if you just look over the dates but it works for us.

We use the budget plan with Union Gas and the true up is Sept.’s payment. Last year We had over paid them so much thanks to the price they paid for natural gas that we didn’t pay a full month’s payment until Dec!!!! We could have had them send us the money back but I just figured I’d let the money pay the bills for a couple of months.

That over budget amount for the cell phone bill is not the worst I’ve seen. Back a number of years ago we had two of the three kids away from home for a few weeks in the summer. This was back when you could get a card from Bell that let any long distance calls go through at the direct dial rate instead of having the kids call home collect and we pay that rate….. I was going to get the two kids each a card for calling home but hubby refused to do that….didn’t want to encourage them to call home all the time. Nice try, we had two very homesick kids calling almost every day. The older boy was calling from CFB Borden (Basic training) and our daughter was calling from St Boniface Manitoba where she was on a second language immersion program!!!! Trust me… you don’t want to know what those phone bills were like!!!!! When the older boy was sent on course to Halifax a few months later I handed him the calling card right in front of hubby and hubby didn’t say a word this time. He didn’t dare.

Boy you really have a decision to make about when to move your money!!! At some point you will have to bite the bullet and move the funds but I don’t see any problem waiting a month or two there. I had to get the older boy to help me get at the budgets you have so I’ll be seeing how I can work things out. Just found out that the older boy is cleared for CPP-D so there is that figure to work in……

That stinks…I hear you with getting busy and forgetting that it’s already set up! Organization is key and slowing down for a minute or two.

I do a mix…this was our third month of being a month ahead and it makes things much easier. On the first of the month I pay any bills that I have the amounts for and pull out cash for the envelope categories we have the hardest time staying under budget with. My insurance bills, car payments and daycare bills come out automatically. I have never experienced errors from autodraft, but have made lots on my own! In my budget sheet I have a budget amount and actual amount. I am the only one in the house that handles the bills (hubby and I discuss and agree on everything, I just handle the work) so as soon as I pay the bill I enter the amount in the actual category. Most get done immediately at the beginning of the month and as the straggling autodrafts occur I enter them as spent so I know it’s done! Even though my bills come out automatically I still receive bills very month with the typical grace period before they come out. I watch them like a hawk…for example the cable bill arrived and surprise they hiked the bill by more than $20. They thought we’d be ok paying $85 for JUST internet! We were on the phone the next day and got it dropped to $53!

These last three months of being ahead have made a world of difference!

How do you like using the envelope budgeting system? I have found errors on the bills which I have to call to get removed and had I not have noticed we would have ended up paying for them. Watching them like a hawk is not a bad idea at all. Mr.CBB

I am a dinosaur in some ways but not in others when it comes to paying bills.

The only automatic payments I allow are the ones for our life insurance and our auto insurance but only for 12 months at a time at a rate set-out in a schedule at renewal time. I don’t like the idea of authorizing anyone to willy nilly take money from our account. Plus, I don’t earn any interest on our chequing account so I don’t keep any more in there than absolutely required and although we have a small line of credit on my chequing account…I am not interested in dipping into it and the associated fees because some creditor took more than expected.

I still pay our municipal property taxes with a cheque each year that I take right to the cashier at city hall and have it date stamped. I have a copy of the cancelled cheque (front and back) from my bank account to show proof of payment in the property tax file.

All of our bills with the exceptions of insurances and taxes are done by e-notification and I download the copies of the invoices. I prefer not to have mail coming to the house as we have a mail box outside our house. Junk mail and flyers can go in there but I really restrict how vulnerable we are to theft… especially at this time of year.

The only other cheques that I write are when I move money to other banks or brokerage houses and that includes paying our RRSP fees annually. My bank has free chequing privileges and my ATM deposits are also free – so I don’t incur any service charges this way. If I move the funds online…it’s 50 to 75 cents per transaction. That adds up fast over the course of a year. I am enough of a dinosaur that I would rather pay for a stamp and mail in my brokerage contributions than pay the service charges that would apply to move from bank to bank then bank to brokerage accounts. I know it’s not a lot but I hate to give the banks any service fees that I don’t absolutely have to. 🙂

My bills that can be paid annually by credit card are done that way so that we earn reward points on the transaction…examples of these are our out of country medical insurance, our house insurance, our accounting fees and our BCAA and MedicAlert memberships. Monthly bills that we pay using a credit card are things like groceries, parking, gasoline, car repairs, gifts, entertainment, travel expenses, timeshare condo fees and taxes, dining out, an annual purchase of AT&T gift cards to top up our cell phones, any new purchases, repairs around the house and our annual service contract with Orkin pest control company, our storage locker rental, haircuts, physiotherapy, massage, chiropractic appointments, the podiatrist, reflexology and any medical/dental expenses not covered by our extended medical. It’s good to have a full accounting of where we spent our money in a given month plus we earn oodles of rewards! I like having a digital copy of all the bills and the associated payments on hand too. If I have something to discuss with a firm while we are away…I have all our records with us. 🙂

Our telephone/internet, cable tv, Fortis gas, BC Hydro hydro, weekly garbage collection, credit cards and tax installments, when they are applicable, are the bills that I pay online each month that they are due. I print a copy of the payment confirmation and attach it to the bills after they have been paid. I pay these online strictly because each of those companies levies a surcharge to pay them by credit card. I know… I just hate paying anything extra that I don’t have to though. LOL

Not exactly straight forward but it gets the job done, earns us lots of rewards while eliminating almost all of the bank fees we pay in a year. My time is worth something but I haven’t factored that opportunity cost into the equation. 🙂

Hi Mary,

We are just like you and don’t like to let people have access to our account nor do we want to pay any fees or anything extra. I think it’s great you can pay your house insurance on your credit card and that’s something I’m going to look into. We only allow our investments, insurance and that’s about it to be automated and the rest we pay manually for the same reasons as you. I am working on getting rid of the mail that comes to the house as it’s not necessary with the internet that we have at home. It was a good point that you bring up about the surcharge on the credit cards because I’m sure many people don’t think of that but it’s extra money just to pay a bill which seems odd to do if one doesn’t have to. Geesh that could be a really good blog post you have above… well written Mary as always. Mr.CBB

Thanks Mr CBB!

You’re welcome Mary 🙂