{kind=link}

THERE’S NO WAITING GAME WHEN YOU WANT TO MANAGE YOUR FINANCES EFFECTIVELY

Whether you are in debt or not managing money must begin today if you want to feel good about your financial future. Personal finance management starts with a positive mindset where you believe your situation will get better and not waiting for opportunity to knock.

Trust me, if I didn’t get my butt out there looking for a job when I moved to Canada or put myself back into school I’m not sure where I’d be today. I’d likely be working at a job I didn’t like but I would do it for the money. That’s the way the world goes but I certainly wouldn’t have ended my job search.

Perhaps some of you reading this today may feel you are stuck in the same or a similar circumstance and although it may not be your ideal situation managing money must be a part of your routine.

To App or Not

These days there are apps for just about anything when you want to manage your money. There’s an app for your banking, budget, spending tracker, allowance tracker and so on. Personally, I think these apps and online tools can be overwhelming for people who have never used a budget before.

I can appreciate the frustration especially since I’m not a smartphone owner and wouldn’t know where to begin. Call me historic if you wish but I prefer to manage finances with a budget spreadsheet, pencil, paper and an actual calculator.

I’m not one of those “figure it out in my head” kind of guys. I like to make sure the numbers add up. Put it this way, if you hire an accountant to do basic accounting for your business would you want them to do it in their head? You’d never know but the thought of someone managing money that way irks me to no end.

Managing Money is more than numbers

Trying to explain how managing money can change lives is one of the hardest things to do for anyone in the finance field who has experienced some form of money success. By this I mean they have successfully figured out how to make money work for them and continue to have people want to know the secret to their success.

I’m not sure why so many people view managing money as a numbers game when in reality it’s probably one of the most basic math skills you would have ever learned. Besides the numbers though it’s a mindset. Your budget is NOT going to work on numbers alone.

You have to be the driving force behind your money which means that if you have anyone in tow they need to be on board or you will suffer the consequences along the way. No person that I have chatted to in my years of finance blogging has been successful managing money on their own with just numbers. There are always secondary factors involved.

Sure, the math might work out and the budget balance every money but the resentment, financial loneliness and burden one person might feel is all to real for some people. This is why couples need to be on the same page when dealing with managing money and applying ground rules for budgeting.

Money planner

Managed funds are far better than just hoping that the money you have in the bank will pay the bills every month. It’s imperative that you know everything and anything about managing money that YOU earn. This also means digging deeper into the reasons why managing money has become so challenging for you.

Some of the reasons why people aren’t managing money from the moment they start earning an income varies depending on situation. When I was a kid I didn’t budget BUT I did have a savings account, piggy bank and motivation to save as much money as I could. That mindset was with me from a young age which then flourished into me being a frugal shopper to a budget enthusiast in my 30’s.

It’s a progression I believe should have happened sooner in my life which would have helped me accumulate wealth far greater than we have today. No reason to dwell on the past though rather focus on where you want to be next month, 6 months from now, one year from now or 5 to 10 years from now. Heck, dream about that retirement you want. It can’t happen unless YOU make it happen.

Don’t need it

I wish I had confidence to say managing money is not a big deal but I can’t. I suppose if it were not then you wouldn’t be here reading this blog anyhow. There will be people who are happy with the life they lead which may include living pay to pay. They may not care too much about retirement and are happy to live simply with what they have. This is conditioning of life where we get used to what life has given us. You don’t have to be wealthy to be happy comes to mind.

Although this may be true (even for us) when things start to happen or emergencies happen it’s not enough. Using money from your retirement savings to pay debt is frowned upon in these types of situations. Money will always play a role in our lives whether it’s serious or not. Living simple doesn’t mean you don’t need to save for tomorrow or think about tomorrow.

I know a family who earns very little every month but they still budget even though they can only save a few dollars here and there. It’s unreal to see how dedicated some people are to finding ways to make money work even if it is a fiver going into a savings account each month.

Unless you are very lucky in finance money won’t manage itself. You may earn enough money but you aren’t saving it effectively if you aren’t managing it. I know people who earn thousands of dollars each month and still can’t save money.

It’s not about how much money you make, it’s how you save it.

Spouse/Partner won’t participate

This is always a tough one because it’s so important when managing money that both partners participate in the budgeting process. Even if one spouse has no desire to learn how to manage basic numbers they MUST contribute to the success of managing money. This means they may have to get an allowance to curb overspending and talking over purchases and making sure you collect receipts along the way.

We don’t talk to each other about every single purchase but in the beginning setting ground rules is important to budgeting success and eventually it becomes a way of life. You just do it. Could I have my receipt please? Well, your brain will be automated and that’s what you want with budgeting.

Too Busy

Kids, Work, Fitness, Friends, Entertainment, Hobbies all take up too much of my time so managing money is out of the question. Does this sound like you?

Is managing money the first priority or the last priority on your day-to-day chores list? I’m not trying to put family on the back-burner here because I know how important it is to be a parent or care-giver but consider what would happen if you didn’t have the money to do so?

Money is an umbrella that will hover over us until we die whether we have lots of it or just enough. If you have time to check your social media accounts or watch television you have time to budget. No excuses. Not work, tired, sick, busy, nothing.

Make the time or accept how your finances grow in wealth or debt.

It won’t help

The only reason you believe it won’t help is because you haven’t lost a chunk of that debt right off the hop. Like dieting you must give your budget a chance. This may take a month to three months to start seeing improvements with paying down debt and getting all your finances in order.

You MUST believe. If you know that you need to earn more money, then do it or cut back. This may include moving to a smaller space, different city or coming up with some sort of practical plan that includes minimalist living. I wish there was an easier answer, but there isn’t. Complaining about it won’t work either, I’ve tried but it doesn’t pay debt or increase savings.

Lacking Financial Management Skills

Over the years I’ve done some research into the education system in Canada and how deep, if at all teachers are educating students about budgeting and basic financial management in the real world.

This is critical and for those of you who agree make your voice heard. Our children of the future deserve a chance by learning not only what they need to do in order to become someone they need to learn how to manage personal finances.

Like I mentioned earlier budgeting is basic, it really is which is why there is no excuse for it not to be part of a math curriculum in school. Once you have all of your numbers available to you the rest is a bumpy breeze but SO worth it. Understanding how to budget is a learning experience that even we continue to do year after year. If you can add, subtract, multiply and divide (with a calculator) you’re good to go with a basic budget.

Don’t feel as if you have to be some sort of math super-star to balance a budget because it’s not as bad as you think. The hardest part is trying to motivate yourself into believing that. The only way you will is to dive right in and start learning. You will make mistakes BUT you’re doing it and that’s what matters. You’ll see results if you keep at it.

Fear of failure

Whatever you do don’t go down this road if you can help it. I know it’s easier said then done but the fear of not being successful is why people are not. We put such a burden on our shoulders when it comes to being who we want to be instead of focusing on what should be.

One example I can give you is when I was in University my roommate was in awe how I was frugal with my money. He was the type of guy who wanted to be a ladies man and show off the bling he never had. He wanted to be successful but only appeared successful because he was in such a damn rush.

Are you one of those people who worry about what everyone thinks about you? Well, that was my roommate and although we were finishing up University it didn’t matter who he met a side of him came out that far from real, it was make-believe. You can act all you want but when the bills start rolling in there’s nowhere to hide.

You may well just fail at budgeting not once but twice or three times but remember if you don’t give up you haven’t lost anything, You’ve gained knowledge, experience and will be better armed the next time.

2017 was our transitional year

As you will see in our charts below with our end of year budgeting numbers we didn’t do so hot. We had many challenges to face in 2017 with my job changes which included lost income. We also spent a nice chunk of money on holidays back to the UK even though as much as we could was saved through projected expenses it still hit the net income. Renovations came into play in 2017 once again as did helping out the in-laws with a new roof and a few household improvements.

There were plenty of financial lessons in 2017 which gave us even more ammunition to make sure we are saving enough money for retirement and keeping our home well maintained via an emergency savings account, savings and projected expenses. The last thing we want is for our son to worry about his parents financial situation when he is trying to make a mark in this world.

We learn, we challenge and we move on!!! That’s how you conquer your finances. It won’t always be positive but take the good with the bad and find your solid ground.

Motivation and seeing your winning goals are what you need to keep going! If you are in a relationship then you both need to see this as a team effort. Money is not one-sided in love.

Start now!

This may be the year for you. If you are reading this post in June and are thinking it’s too late to get into the budgeting game or managing money until January, STOP! Do it now, don’t wait. Your future self deserves the chance to make it right.

Discussion Question: What other reasons do people come up with as to why they aren’t managing money effectively?

Where our money went in December

Not a particularly spectacular month at all. Too much spending actually broke us even this month to the penny, which is really weird. I know a lot of people go overboard at Christmas and feel the effect long after. For us, we had a blip on the radar and that was about it.

Our FREE Simple Budgeting Series

Do you want to learn to budget like we do?

We explain everything we do and more in this mini-series below all about budgeting.

Please take the time to read through our budgeting series plus read Budgeting in the New Year. I hope the information will help stop you from making common budgeting mistakes that I hear of often and that you take something away from the information and apply it to your financial situation.

If you have any questions about what we do with our budget money tracker feel free to email me.

- How We Designed Our Budget Step 1– Gathering All the information

- How We Designed Our Budget Step 2– Budget Categories

- How We Designed Our Budget Step 3– Tracking Receipts

- How We Designed Our Budget Step 4- Note-taking

- How We Designed Our Budget Step 5– 5S Organization

- How We Designed Our Budget Step 6– Who Does What and When?

- How We Designed Our Budget Step 7– Balancing Our Budget

- How We Designed Our Budget Step 8– Knowing our Coupon Savings

- How We Designed Our Budget Step 9– Reading Our Bills

- How We Designed Our Budget Step 10– Projected Expenses

Budget percentages December 2017

Our savings of 29.81% includes investments as well as any savings for this month based on the income of $8665.21. We put money away for the projected expenses for things that need to be paid for in the coming months. The other categories were fairly normal this month. All of the categories took 100% of our income which shows that all the money we earned for the month is accounted for..

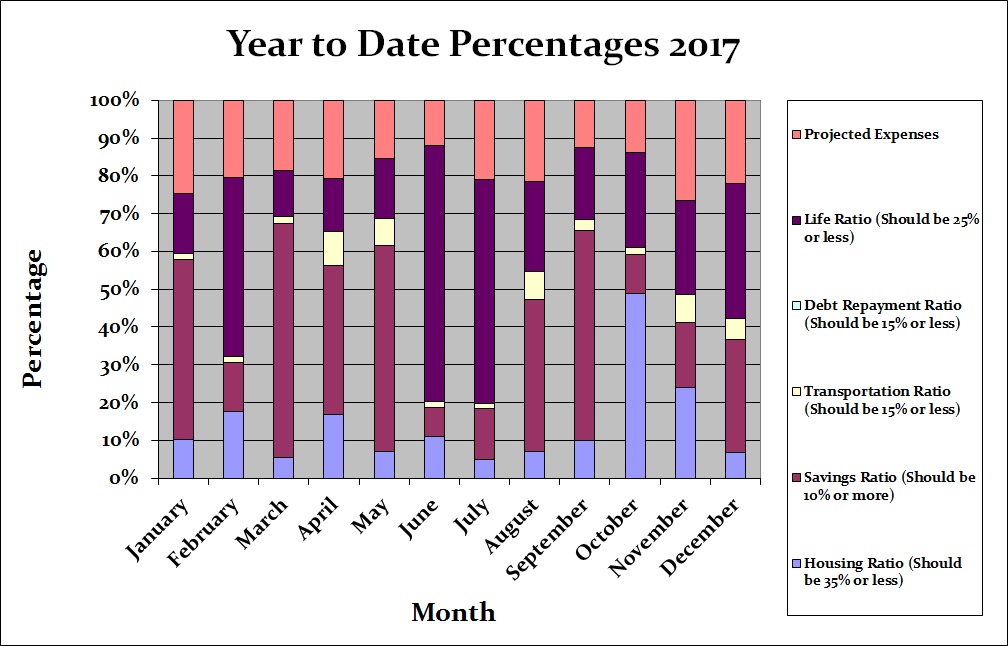

As you can see we had a tough 2017 for money in our life ratio category because of the amount of money we spent outside of what we thought we would save. The percentages actually add up to 122.77%, meaning we spent more money than we should have. As we have Projected Savings as well as our Savings ratio, we would have to deduct the extra percentage amount we are over from the savings category in order to make more sense.

By removing the 22.77 percent we were over we can see that our Savings ratio was actually 12.43%. I need to devise a way to eliminate this over percentage calculation in the next budget spreadsheet I am working on.

In 2018 we are going to work on that number although what we did spend in 2017 was more to help family members than it was for us. We did go on holidays and buy a new vehicle as well which cut into a large chunk of our money even though holidays fall under PE. You can’t predict everything when travelling.

Budget percentages month by month

Breaking down expenses

This is simply a breakdown of our expenses which has helped us to understand where all of our money goes. Since May 2014 we have been mortgage free so much of our money will be directed at savings, investments and renovations.

I appreciate that you enjoy this budget update each month but I do hope you view this as an educational tool rather than comparing your own financial numbers as our situations are all unique.

Although I encourage your comments and love to hear what you have to say about our budget categories and expenses please don’t tell us to donate our money to charities because we have too much or are fortunate. We are hardly out of the clear with finances for the rest of our lives and have worked and sacrificed to get where we are. We do plan to enjoy the money we’ve saved now since we haven’t over the years with our son.

What we do with our ‘extra cash’ is our business and although we do donate to a charity we won’t be putting it on display for the world to see as it defeats the purpose in my eyes. It is part of the budget as you see it. I hope that clears that up for those of you who had concerns about our extra money.

Just 10 years ago I started working in Canada making a bit over minimum wage and have since moved up the ladder. I’m now working very hard to secure my dream job with one foot in the door. We aren’t all lucky but if you do the best you can at least you can look back and say you gave it a shot.

Sometimes we wish we had more money to budget with but understand that we only have what we earn and if we want more, we need to earn more. Spending less than we earn and budgeting our money has been the easiest way for us to pay down debt and save money.

- Chequing– This is the bank account where all of our debt gets paid from.

- Emergency Savings Account– This is a high-interest savings account.

- Regular Savings Account– This is a savings account that holds our projected expenses.

- Monthly Budgeted Total: $5,187.39

- Monthly Net Income Total: $8,665.21

- (Check out our Ultimate Grocery Guide to see where our grocery money goes)

- Projected Expenses: These are expenses we know we will pay for throughout the year = $1917.68

- Total Expenses Actually Paid Out: $5,322.80

- Total Expenses Actually Paid Out: Calculated is $8,665.21 (total net monthly income) – $1,917.68 (projected expenses) – $0 (savings in to emergency fund) = $5,322.80

- Actual Cash Savings going into Emergency Savings: Calculated is $8,665.21 (total monthly net income) – $5,296.31 (actual expenses paid out for the month) – $1917.68 (projected expenses) = $0

Budget Results

Time for the juicy category numbers and to see how we made out with our monthly budget. Below you will see two tables, one is our monthly budget and the other is our actual budget for the month of December 2017. This budget represents 2 adults and a toddler plus our investments.

Budget colour chart

If highlighted in blue that means it is a projected expense. You will also see our budget does not include the emergency savings as it’s factored in at the end.

Budget for December 2017

Actual budget expenses for December 2017

Actual budget expenses for December 2017

Budget updates month by month

In case you missed our budget updates and want to do a quick search I’ve compiled them all on one handy page: monthly budgets. For the 2017 Year I will also keep track of each month below and update the monthly budgets page.

- January 2017

- February 2017

- March 2017

- April 2017

- May 2017

- June July August 2017

- September 2017

- October 2017

- November 2017

That’s all for this month check back at the beginning of February 2018 to see how we made out with our January budget.

Happy Budgeting CBB’ers!

Don’t Forget To Subscribe To The Blog and Activate Your Subscription!!

- Find me on Social Media by clicking any one of the links below

- Check out my new Free Recipe Index

- If you like FREE then click this link for my FREE Excel Budget Spreadsheet and all my Free Money Saving Lists!

- You can now have full access to my Ultimate Grocery Shopping Guide in Canada.