")

{kind=link}

DON’T LET THE EMBARRASSMENT OF DEBT KEEP YOU FROM REALIZING YOUR FINANCIAL DREAMS

There are consequences of owning debt and for 30 year-old Margaret who is feeling the emotional effects of debt guilt there are things she can do to get over this hurdle.

Margaret isn’t the first person to email me about debt guilt and even myself at times felt guilty for owing money and had to pay it back as fast as possible. I remember the time my mom and dad gave me $5000 just before I moved to Canada. My house hadn’t sold yet and my money was tied up in my house equity and I needed to pay for Canadian Immigration documents, applications for permanent residence, medical assessments, flights to Canada, shipment containers and so on.

The money my parents gave me was helpful and the first time I’ve ever borrowed cash from them in my life. They knew I’d pay them back as did I but boy oh boy did I feel stressed that I had to ask them for money. I’ve since overcome that guilt because I’ve learned that our bodies all react differently to certain situations. Since I was the kid who thought he had it all down with finances it was tough going asking for help. Asking for help is one of the hardest things for humans to do.

Over the years I’ve managed to incorporate meditation, healthy eating habits along with daily exercise to help release stress from my body and it’s brought me to a better place. This was only one step in the process of getting rid of debt guilt, let me explain.

Dear Mr. CBB,

I am a 30 year old woman and I am ashamed of my debt which is why I hide it from everyone I know. Most of my friends have great jobs earning decent money as do I but I have no control over how I spend it.

Just recently I tallied up my debt and I owe over $5000 to one credit card which includes a holiday with friends and clothes that I purchased for a new job offer I accepted. When I think about how much money I owe to debt and my monthly expenses I get headaches and just overall feel depressed about my situation.

I feel my spending is spiraling out of control and I want to step back from my social life and clear up my debt and the emotional stress that it’s causing me. I feel my friends won’t understand my debt guilt but maybe someone out there might have some tips to help keep me grounded.

Thanks,

Margaret

Does credit card debt matter? It sure does! Does all debt matter? It sure does.

Any time you owe money to anyone it matters because this means you are in debt to someone or a company. If you let your debt increase it may also increase the emotional effects you feel as you must pay back what you owe. These emotional effects of debt guilt or shame can take it’s toll on your health.

Over the past few months of talking to random strangers about money which is what I do for some reason. I don’t do it on purpose as money talk seems to smell me from a mile away. At least that’s what I initially thought but in my quiet time I soon realized that people want to talk about money because they are interested in what other people have to say.

Related: Household Income in Canada – Key results from the 2016 Census

They may not divulge their personal situation but they have no qualms about how expensive everything is getting or unaffordable for the “Average Canadian”. Don’t ask me what that is but it came up in conversation with a guy at Costco while we were enjoying an ice-cream.

Perhaps he meant the average blue-collar Canadian couple or those earning a middle-class income which varies from province to province. To be a middle-class income earner in Canada your household income would reach $70,336 according to the 2015 Canadian Census. Middle-class income really depends on where you live.

The average Canadian owes $8,539.50 in consumer (non-mortgage) debt – Source

I often wonder if the people who talk to me about money the most whether they are the one’s who are suffering in silence the most. I can almost sense financial pain in conversations with people especially when they drop hints such as the lady I spoke to yesterday at swimming lessons for our son.

She was attending a free evening program for her child at the community centre and we got talking about swimming lessons and the costs involved. She told me she had to pull her son from swimming lessons at the YMCA because it was far too expensive and the costs of food were rising. It was in that moment I looked in her eyes and her facial expression changed as did her tone of voice. She also mentioned that the bus ride across town was proving to be too much with three kids in tow.

She did give me one tip that many of the local schools in our area offer swimming programs for the kids which her son participates in now. Sometimes just talking to people opens up avenues that you never knew existed.

Another gentleman I spoke to at Value Village on Tuesday night told me he brings his kids to the store to play with the toys instead of buying them new because he can’t afford it. He didn’t need to tell me this, but he did and perhaps this is what helps him deal with the financial burdens we all feel today in Canada. Big income or not that doesn’t mean we are all rich and free from debt.

Overcoming Debt Guilt

Everyone deals with finance differently whether they talk to strangers on the streets or looking for help from friends or even online nerds like myself. Most importantly overcoming debt guilt starts with conversation. Admitting your debt is getting the best of you is an important step that many people hide. Don’t for one second think that just because your neighbour has a good job that he or she is rich or free from debt guilt.

That’s not true because we become masters at hiding what we don’t want the world to see. It’s human nature but for those of us who suffer in silence it can take it’s toll on your relationship, family life and employment. Not only that but emotionally debt guilt can cause stress that may lead to depression, migraines or other body ailments. Taking care of yourself first is number one.

For Margaret her debt guilt is getting the best of her and she needs to a step back and focus on herself first. Margaret if I were in your shoes I’d pat myself on the back for talking about your debt guilt. Second, you will surpass this because you recognize what it is doing to you and you want to make changes happen.

Here’s my suggestions to release debt guilt and increase debt freedom prospects!

- Write down your thoughts and feelings along with some short and long-term goals.

- Learn to say no or find other activities that will take up your time so that you aren’t plagued with having to make up excuses to your friends. Not everyone likes to tell the world they are sitting in a pile of debt but you don’t need to feel shame about it. You know what? You’re not alone.

- Set a budget, stick to the budget and follow-through even after you pay your credit card debt off.

- Read and educate yourself about finance to better understand different outlets that might help you.

- Take time for yourself each day to meditate or enjoy a cup of tea on the front porch or in a comfortable spot in your home.

- Reflect on what positive has come from your debt repayment plan even if it is small.

- Find someone you are comfortable talking to about your debt even if it is a bank manager or financial advisor for guidance. Sometimes talking to strangers is a great way to release debt guilt too but be weary about any advice they may offer.

- See the positive in situations and cut out negative talk about your money as this only will set you back.

- If you aren’t earning enough money find other resources that can help boost your income.

- Incorporate healthy eating and exercise into your daily routine if possible

Don’t let debt guilt blanket your life with negative thoughts because the more you let that voice hamper your success the further down the hole you will go. YOU can get out of debt but it takes time and practice to be frugal and follow your financial steps from point A to Z.

Discussion: What other suggestions would you give to Margaret to help ease the debt guilt she feels?

Where our money went in June

Hey everyone!

Hey everyone!

June was another financially busy month for us as we’ve been working on ripping out the fence in our back garden. I’ve decided that I’m not hiring anyone to remove our 20+ year old wood fence and install a new one because I can save us thousands if I do it myself.

Once I get the post holes sorted the rest will be simple. Thankfully all but one of our neighbours will be pitching in to pay for and build the fence with me which is great news. I’ll likely write a blog post about the experience once the job is completed. The hardest part so far was approaching the neighbours looking for money.

This past month we’ve also been busy with soccer, baseball and swimming lessons along with some day trips to local farms, parks and splash pads. We hope that before the summer is over that we can be adventurous and explore more of what’s lurking behind the country roads in Ontario. So much to discover!

Budget mistake: I noticed that I have forgotten to move the Christmas reserve funds the past 2 months (actually Mrs. CBB caught this) so I will update that in July to reflect the past months that were missed.

A second mistake is that we are now paying for our property taxes monthly since paying the mortgage off which means we need to remove that number from our projected expenses. This will drop our PE significantly and something that was a big mistake on our part. It’s important to remember that we are all human and mistakes happen. Fix them and move on.

Have a great month everyone!!

Mr.CBB

Our FREE Simple Budgeting Series

Do you want to learn to budget like we do?

Do you want to learn to budget like we do?

Please take the time to read through our budgeting series plus read Budgeting in the New Year. I hope the information will help stop you from making common budgeting mistakes.

Our Ultimate Budgeting Guide from A to Z has everything you need to know about budgeting in one blog post.

- How We Designed Our Budget Step 1– Gathering All the information

- How We Designed Our Budget Step 2– Budget Categories

- How We Designed Our Budget Step 3– Tracking Receipts

- How We Designed Our Budget Step 4- Note-taking

- How We Designed Our Budget Step 5– 5S Organization

- How We Designed Our Budget Step 6– Who Does What and When?

- How We Designed Our Budget Step 7– Balancing Our Budget

- How We Designed Our Budget Step 8– Knowing our Coupon Savings

- How We Designed Our Budget Step 9– Reading Our Bills

- How We Designed Our Budget Step 10– Projected Expenses

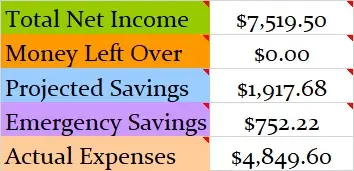

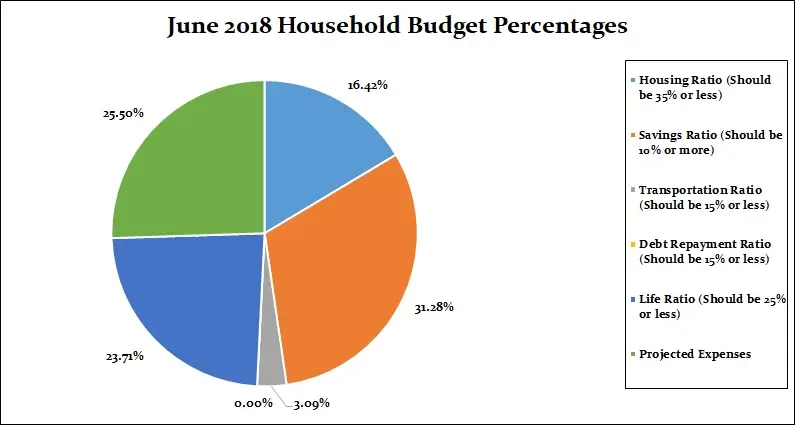

Budget percentages June 2018

Our savings of 31.28% includes investments as well as any savings for this month based on the income of $7,519.50. We put money away for the projected expenses for things that need to be paid for in the coming months. The other categories were fairly normal this month, even if the Life Ratio is a little high and close to the maximum. All of the categories took 100% of our income which shows that all the money we earned for the month is accounted for.

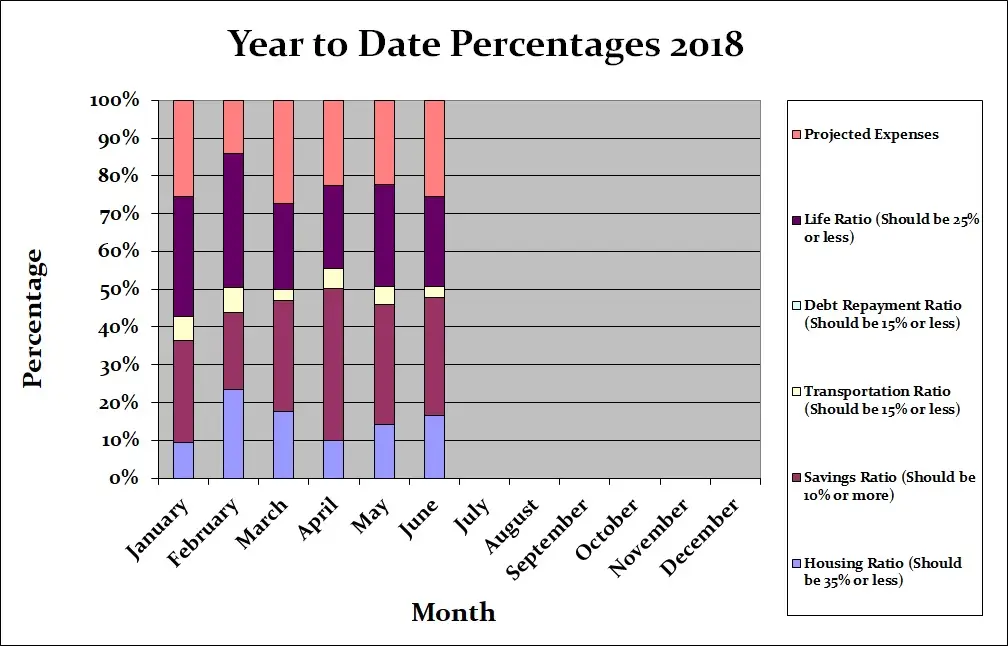

Budget percentages month by month

Breaking down expenses

Below is a breakdown of our expenses which helps us to understand where all of our money goes. Since May 2014 we’ve been mortgage free so much of our money will be directed at savings, investments and renovations.

I appreciate that you enjoy this budget update each month but I do hope you view this as an educational tool rather than comparing your own financial numbers as our situations are all unique. Spending less than we earn and budgeting our money has been the easiest way for us to pay down debt and save money. It may be different for you.

- Chequing– This is the bank account where all of our debt gets paid from.

- Emergency Savings Account– This is a high-interest savings account.

- Regular Savings Account– This is a savings account that holds our projected expenses.

- Monthly Budgeted Total: $5,376.40

- Monthly Net Income Total: $7,519.50

- (Check out our Ultimate Grocery Guide to see where our grocery money goes)

- Projected Expenses: These are expenses we know we will pay for throughout the year = $1,917.68

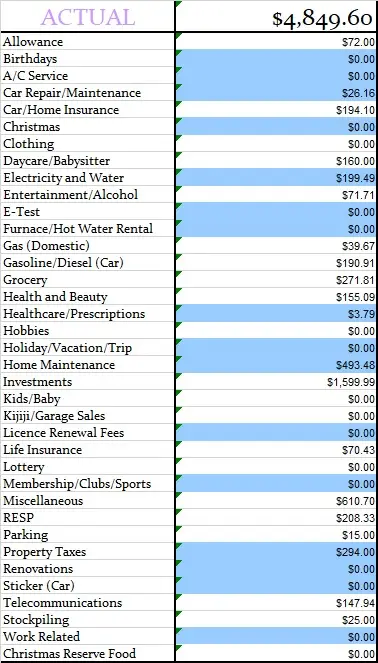

- Total Expenses Actually Paid Out: $4,849.60

- Total Expenses Actually Paid Out: Calculated is $7,519.50 (total net monthly income) – $1,917.68 (projected expenses) – $752.22 (savings in to emergency fund) = $4,849.60

- Actual Cash Savings going into Emergency Savings: Calculated is $7,519.50 (total monthly net income) – $4,849.60 (actual expenses paid out for the month) – $1,917.68 (projected expenses) = $752.22

Budget Results

Time for the juicy category numbers and to see how we made out with our monthly budget. Below you will see two tables, one is our monthly budget and the other is our actual budget for the month of June 2018.

This budget represents 2 adults and a toddler plus retirement investments.

Budget colour chart

If highlighted in blue that means it is a projected expense. You will also see our budget does not include the emergency savings as it’s factored in at the end.

Monthly Budget for June 2018

Actual budget expenses for June 2018

Budget updates month by month

Just in case you missed our budget updates and want to do a quick search I’ve compiled them all on one handy page: monthly budgets.

That’s all for this month check back at the beginning of August 2018 (sometimes in the middle) to see how we made out with our July budget.

Happy Budgeting CBB’ers!

Don’t Forget To Subscribe To The Blog and Activate Your Subscription!!

- Find me on Social Media by clicking any one of the links below

- Check out my new Free Recipe Index

- If you like FREE then click this link for my FREE Excel Budget Spreadsheet and all my Free Money Saving Lists!

- You can now have full access to my Ultimate Grocery Shopping Guide in Canada.

Mr CBB, it’s all well and good to say use a budget but you also need to look for every opportunity you can find to save money.

Every time I look at the actual spending of folks that are in debt there are some common denominators:

Are you eating out? If so, stop it or if you really must have a treat, make it lunch…not supper. It’s a lot cheaper!

Are you grocery shopping with a list? If not, do so! You can check the online flyers for the loss leader sales and build your meal plan around what’s cheap that week. Last night I picked up 2 packages of strawberries, 8 apricots, 5 MASSIVE yellow nectarines, 2 cauliflower, 1 cantaloupe, 1 honeydew melon, 2 huge beefsteak tomatoes, a package of grape tomatoes, an 11lb. watermelon, 2 iceberg lettuce for $25 total just by picking the sale items in 3 stores on my way home from a medical appointment. I used the car and it’s gas for more than one purpose too…another way to reduce costs. Guess which household will have some amazing fruit salads this week? Always buy whole fruit and do the slicing and dicing yourself as the stores will happily charge you oodles to chop it up for you! BTW, all this fruit can be used in smoothies, cold soups, juices, frozen as popsicles…it doesn’t have to be boring!

Offer to be the designated driver if you are going out with friends. A lot of bars will give you your pop/club soda etc FREE when you tell them and it guarantees your friends a safe ride home. Good for you, good for them and good for the bar as they won’t be charged with over-serving someone that was driving who had an accident. The best part is, you still get to go.

Consider hosting a wine and cheese tasting party…everyone brings a bottle of wine to share & you put out a cheese tray, crackers and perhaps a little fruit. It becomes a great opportunity to try lots of different wines and to choose a new favorite. Watch for cheese sales too…you can get an assortment of the ones on discount that week. In the same vein, potluck dinners can be fun…get your friends to each take a turn hosting ever month or two and you all get an evening out without all the clean-up except for the month you host.

Summer is great for freebies…invite your friends to join you for an outdoor concert in the park. We have them at least once a week in our area. Watch for festivals to wander around – the music and vendors are lots of fun to wander thru but leave your wallet at home. Just put a $5 in your pocket so you can buy something IF you really must. I always take my stainless steel water bottle so I have something to sip on but I have been known to split a tasty treat with my hubby…something I wouldn’t make at home.

Don’t buy that new book…get it free from your local library! They also have video/dvd rentals.

Do you really need cable or can you survive with a more economical Netflix?

How about that cell phone? Have you tried to negotiate a better package with your provider?

There’s a million little ways to find extra cash to drop right onto your debt & before you know it…that outstanding balance will be gone. Everytime you have a few extra bucks, make an online payment…you don’t have to only make one payment a month. For example, if you have $50 per week for groceries but you only spent $35 this week…$15 goes to the debt right away. Having cash kicking around encourages a lot of people to spend it. So don’t let it lay around – pay it on your debt. 🙂

These are just a few examples that I personally use but feel free to be far more creative with your reduction of expenses than I am. 🙂

Debt guilt queen here! I’m reminded of it less often now 4 years into my journey to kill the urge to splurge.

Rewind 4.25 years, it was a huge shock to realize the amount of unsecured debt I was carrying. Look at the interest tacked on every month, and you get nothing for your money. It’s a stone cold sinking feeling.

Biggest hurdle was clamping down on the unnecessary spending, and with 5 in the household it was a huge fight with 2 of them and still a struggle today. But they expect me to be resistant to spending on wants not needs. They are quite a bit more creative with how they tell me their “needs”. If you could reward persuasive storytelling then they’d get high marks. I’m also at fault for the situation, by not being strong and allowing it to happen. There’s the guilt.

Fast forward to today, I reflect on our family outing yesterday to the farmers market where I spent a grand total of $8.00 on a large bag of kettle cooked popcorn and 3 bottles of water for 6 adults and two dogs. We weren’t inclined to buy the produce as the prices were high. We admired the hand crafts and took business cards to reflect on what might fit into birthday giving. We petted the Percherons and walked the trails and waterfront. And I didn’t feel guilty at all.

You’ll kill the debt. It’s a given, now that you acknowledge it. And go forward armed with a resolution to keep yourself from accumulating unnecessary debt.

Side note, last week one of the young associates said “I’ll never retire with a million bucks.” I said “Not without starting now. Our employer matches contributions up to 3%. Start with $20 per week. I started 3years ago and now have over $8000.” The 16 year old in the room said “You’re rich!” I see more opportunities coming for advice. It’s all in the perspective.