Estimated reading time: 30 minutes

Achieve financial stability through responsibility and accountability. Learn how budgeting and cutting spending can help you save money and avoid debt in Canada in 2025.

Friends, it’s time to reset or start your 2025 budget, and with that comes review and education.

Responsibility and accountability are two powerful words in the finance world because, without them, you risk failure on a personal level.

Let’s talk about both so you better understand how to incorporate each into your Canadian savings journey.

When we think about responsibility, we think about taking out the trash, getting to appointments on time, and ensuring everything runs smoothly daily.

Take on 2025 with baby steps, especially if this is your first time budgeting or you’re stuck in a rut.

The last thing you want to do is overwhelm yourself with numbers and give up on the one thing that will bring you financial success.

Take your time reading this 2025 Savings Guide, and perhaps review or read my mini 10-Step Budgeting Guide for tips and inspiration.

Good luck with your 2025 Savings Journey, CBB Friends.

Our 2025 Low-Spend Year

I’ve noticed quite a few people on TikTok talking about a no-spend or low-spend year for 2025.

A low-spend year entails not spending money on specific budget categories, such as clothing or other items.

We’ve never participated in a no-spend year and plan on a 2025 low-spend year on clothing and food using coupons and other savings apps.

Doing a no-spend and low-spend year will help eliminate items you don’t use or need in your space.

Another thing a no-spend or low-spend year does is that it forces you to use what you already have instead of buying new.

Throughout 2025, I’ll update everyone about our journey in the monthly budget update posts.

Below are many ways to save money in 2025, starting with a budget.

Budgeting Your Money

What is a budget?

Budgeting, therefore, is the process of understanding dollars and cents and having a personal financial plan to help you pay back debt and stay out of further debt promptly.

Money management is a responsibility that every Canadian should take when it comes to accountability for their finances.

Why Budgeting?

You care about your money, don’t you?

It may no doubt to you yet, but once you start your budgeting journey, you’ll realize how much every dollar is and how fast those numbers can add up.

For example, your morning coffee at the local shop only costs $1.50, which seems reasonable for a cup of coffee, but if you get that coffee daily, it costs you $547.50 yearly.

Financial Awareness

What could you do with that coffee money instead?

I’m betting you could buy coffee, a coffee machine, and all the extras for far less and still have money to put towards your debt or investments.

The problem is that not everyone views money this way until they are knee-deep in debt; even then, it’s a stretch.

You have to be financially aware; until you are, all you see is that meager $1.50.

Keep in mind that $547 is only coffee.

That’s like pulling a hair, knowing that there are thousands more.

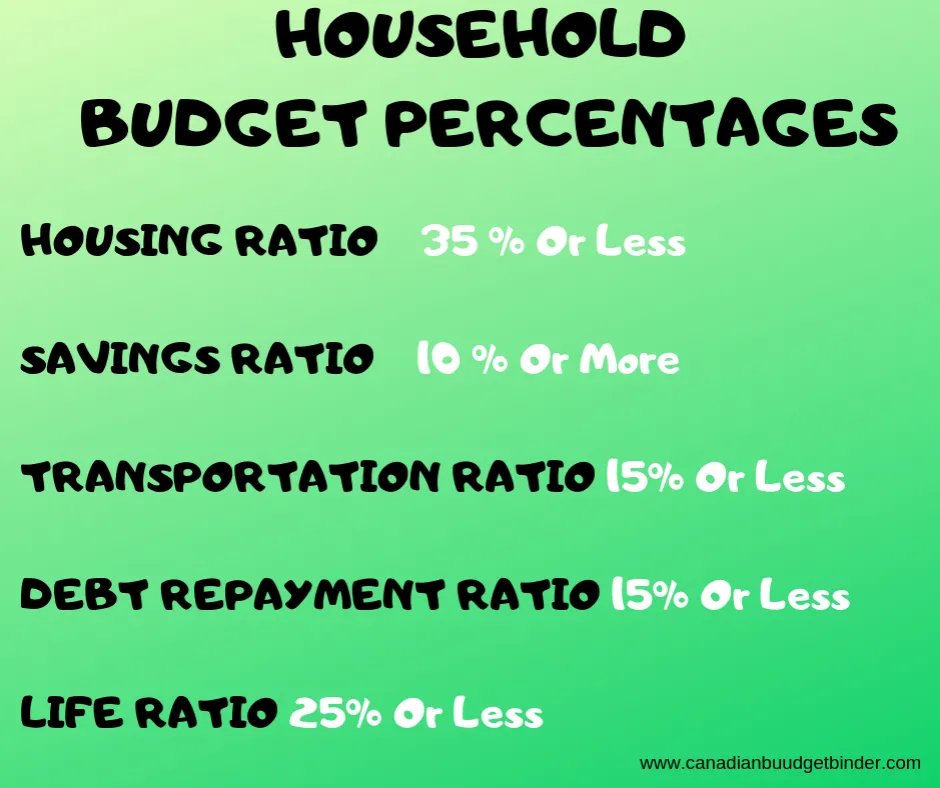

A Budget Is A Financial Journal

When you create your monthly budget, each category can be combined to fall into any one of five household percentage groups.

- Housing Ratio

- Savings Ratio

- Transportation Ratio

- Debt-Repayment Ratio

- Life Ratio

Your budget incorporates everything related to life that costs you cash, and I can bet there’s more than just coffee in there.

In this case, your budget functions as a revolving door for your money, meaning when you pluck one hair, another is waiting in its place.

Unless you get a grip on where the money is being spent or plucked, you’ll always struggle to balance the budget.

The choice is yours, but I assume you are budgeting from A to Z since you’ve come this far in reading.

Below, I want to show you how easy it is to save money with a few simple changes in your life.

Choosing The Right Budget

If you are new to money management and are not good with online budgeting apps or using Excel or Word programs, other types of budgets are available.

A simple or printable budget may be a better option, as you can use a 3-hole punch and insert it into a budget binder.

The idea is to pencil and erase your way through your monthly expenses and earnings.

You may have heard of the budgeting jar or the budget envelope system, which allows you to work with cash only and a paper budget.

These systems allow you to know where your money is going and how much you have to spend based on what’s left in the jars or envelopes.

Cash spending also helps reduce sporadic purchases since you don’t have the extra money to play with.

I’ve often called this the baby steps of budgeting because once you learn the basics, you’ll want to graduate to something more elite, such as a budget spreadsheet.

I’m a fan of the Excel budget, which has worked for us for many years.

Our home budget is a zero-based budget where all the money we earn has a home.

This means we should have a zero money balance at the end of the month because it’s accounted for.

Tracking Expenses

Nobody wants to collect receipts and track expenses, making this a tricky topic for those who want to save money, but it must be done.

You will lose sight of your goals if you don’t know where your money is going.

Besides, you’ve been tracking your expenses within a budget, which is not bad, especially if you set aside time each week to focus on your budget and input the data it needs to run.

It’s like putting gas in your car.

Let the tank run dry, and the car won’t.

Your budget works this way, so put in the time and effort to reap rewards.

Your Credit Score Matters

Due to popular demand, your credit score is essential for many reasons, one of which is to help you save money.

Companies will also look at your credit score when you apply for a loan, mortgage, or credit card.

A good credit score is 660, and anything above that is exceptional, which means the likelihood of lenders giving you a reasonable interest rate is attainable.

You also have more bargaining power when your credit score is good, especially with mortgage companies and credit cards.

When your credit score needs improvement or is on the cusp of sound, you may find your interest rates are higher, and many lenders will shy away from working with you.

They fear you won’t pay back the money they lend you on schedule, which means jumping through hoops.

Conversely, they make more money from you because they offer higher rates than your good credit score friend.

So, to save money, consider ordering your free credit report once a year to be examined through Equifax Canada or Trans Union.

If you find any discrepancies, work on getting them fixed right away.

Even if you are debt-free, reviewing your credit history yearly is essential because anything can happen behind your back with your money.

You always have to be on guard and look for ways to boost your credit score in Canada for the best money savings.

Secured Credit Cards

If you’re new to Canada and don’t have a credit score or history, I would advise you to get a secured credit card.

A secured credit card is where you give the credit card company money to secure it just in case you don’t pay your bill.

So, you give the credit card company $500, and they give you a credit card with a $500 credit limit.

View it as a trial to see how well you are with paying a credit card bill and work on a plan to keep you on track.

The more you use the credit card and pay it on time each month, the better your credit score gets.

Eventually, they will remove the security, and you will be alone, but that takes time.

They want to know you are reliable, and if you fail, they use the money they secured from you.

As a newbie in Canada, I had to go through this credit score increase process, so I know from experience.

Housing Options

Renting vs. Buying

I’m a fan of home buying because it has become a savings plan and requires my money.

On the other hand, renting isn’t so bad as long as you’re saving money simultaneously.

There are pros and cons to renting and buying, meaning everyone lives based on needs, preferences, and affordability.

Renting might not require a down payment, typically only the first and last month’s or other fees, such as parking, utilities, and rental insurance.

Owning a home requires maintenance, paying house insurance, property taxes, and potentially mortgage life insurance.

When you move as a renter, you get no return on investment from the deal.

However, when you sell a house, you earn what you put in and any increase in home value minus selling and legal fees.

The only thing with selling a house is that you may need to buy another, but you’ll almost always have the money you put back on your side of the court.

Stop Buying Overpriced Homes

On rare occasions, if you buy too high, you may be stuck with the house or have to sell at a loss.

For example, buyers who purchased a home in 2021 during the seller’s market and house prices were extraordinarily high, low interest rates and bidding wars may end badly for some homeowners.

Finding a buyer when house prices relax may be a struggle, or the homeowner may face loss.

Also, when it comes time to renew a mortgage, if the interest rates go up too high, a homeowner may be unable to afford the new mortgage.

If you buy something smaller that is less expensive or move to a town or city where home prices are lower, you can bank the extra cash as savings.

Save More For A Mortgage Down Payment

There is no rush to buy a house, so saving for a down payment can take as little or as long as you like, based on how much you’d like to save for your down payment.

When we bought our house, we saved 25% of $265,000, which helped lower our monthly mortgage and pay it off in 5 years.

We bought a home in our price range and not what we were told we could afford because those are two different situations.

Another situation we opted to steer clear of was getting involved in a price war.

As mentioned, buying too high can return to haunt you, as you’ll learn further.

You are the only person who knows what you can and can’t afford.

Steer clear of what others tell you to buy and base it on actual numbers, including any debt owed.

I think saving more for a down payment that would allow us to live comfortably is more appealing.

If you are a first-time home buyer, you can use some of your RRSPs for the down payment, but take caution; you must pay them back.

So, you might get a reduction on your down payment, but you will still have to pay for your mortgage and replace the RRSPs simultaneously.

Avoid Being House Poor

Never put yourself or your family in the position of having a tight budget when you don’t need to, especially when buying a home.

Becoming house-poor is not undone; it only happens because people overspend when buying a home.

Do yourself a favor and create a monthly budget; if you can afford a home on one income, that is even better.

If one person loses their job, it’s easier to tackle variable than fixed expenses.

I always suggest a mock budget that includes a mortgage and any expenses with home ownership.

If you can’t afford them while you are renting, you can’t afford them if you can’t find a house.

Keep that in mind.

If you find that you are pushing the homeowner limits with your budget, wait a bit longer until you feel comfortable talking about any financial emergencies that might come your way.

Oh, and if your real estate agent doubles as your financial advisor, then great, but otherwise, tread carefully about who you talk to about your money.

Toronto-based finance expert Barry Choi sums it up nicely in his post, “Your Realtor Is Not Your Financial Advisor.“

“Generally speaking, there are” only two things your realtor will know about your financial situation: How much you are approved for your mortgage and how much you can “afford” every month.“

Home Decor And Furniture (Minimalist Living)

One lesson I learned about home decor since buying our first home is that we didn’t need half the stuff we’ve purchased over the years.

Although I often don’t search for secondhand vintage items, consider keeping your space at home tidy by limiting how much you purchase.

When your space is cluttered, even with furniture, it can seem minor, and it’s also harder to keep clean because you have to move furniture weekly.

I also found that the more stuff we had, the more dust we’d accumulate.

It’s okay to refuse free stuff or donate regularly to needy people.

Related: How we furnished our first home for cheap

Investing and Saving Your Money

Anytime you invest your money in real estate, business opportunities, stocks, retirement savings, or life insurance investment plans, you risk losing it all.

Conversely, you can earn even more if the money sits in a high-interest savings bank account or TFSA.

Ask yourself whether your risk tolerance can handle the ups and downs of the financial market.

If the answer is yes, then investing money in any of the above with a financial plan may be the route for you.

If not, finding less stressful hiding spots, such as a traditional savings account or GIC, for your money to grow may be a better option.

Savings Account

Almost everyone has a savings account at a brick-and-mortar or online bank where money is deposited and earns interest.

Although the interest won’t be like striking gold, it’s better than under your mattress.

Saving money in a bank is a great way to build an emergency fund and have a cushion available without worrying about liquidity.

We use Simplii Financial, TD Canada Trust, and Tangerine Bank.

Registered Retirement Savings Plan (RRSP)

An RRSP was introduced in 1957 and is a savings plan in Canada that gets special treatment from the Canada Tax Revenue Agency.

The RRSP is one of the most popular ways Canadians can save retirement money.

The RRSP allows us to defer income tax that you would generally pay today to a time in the future.

So, when you remove your RRSP, you will get taxed then rather than today.

In the meantime, it allows your RRSP investments to grow tax-free, which means more savings.

Defined benefit plans are far and few, leaving Canadians responsible for saving money to retire.

Many employers in Canada offer an RRSP savings plan that matches up to a certain percentage if the employee invests x amount.

Take advantage of the free money, tax-free growth, and tax deferral opportunity.

If you can handle paying into the RRSP as a savings plan at and outside your employer, you’re well on your way to retirement savings.

Tax-Free Savings Account (TFSA)

The TFSA was introduced in 2009 and has increased in popularity ever since.

Unlike an RRSP, you do not get a tax refund when contributing to a TFSA.

As the name suggests, you do not need to pay taxes as it’s a tax-free account.

That means you can invest your money within a TFSA, and when it grows, so does your net worth.

Should you invest in a Tax-Free Savings Account?

The choice is yours, but I’d say yes if you have the extra money!

However, do your due diligence and talk to a trusted financial advisor.

Contributions to a tax-free savings account can be used for emergency or retirement savings.

For 2025, you can contribute $ 7,000 for the year to a TFSA as the government limits how much can be invested, which has varied since 2009.

Understanding Dividend Investing

Dividends are cash payments made to shareholders in a company, which means you invest your money in a company, and when they earn, you earn, too.

By investing in a company, you become a part-owner of that company, so any recognized profits become, in part, cash in your pocket.

Over at My Own Advisor, a blogger states the 5 Things You Need To Know About Dividend Paying Stocks.

- Immediate Return

- Safety Buffer

- Dividends Increase over time

- Dividends have a long history of being paid out

- Dividend yield can help you decide when to buy

Hang On To All Receipts

Number one savings tip for groceries and any other product you buy: please KEEP YOUR RECEIPTS! Yes, I’m yelling.

I can’t stress that loud enough because, without a receipt, you risk being able to return a product or get a price reduction if the item goes on sale within 14 days.

Some stores offer this deal, so look for store policies.

And not just grocery stores, keep receipts for everything you spend money on, big or small.

File them in your budget binder to track your monthly expenses.

If you collect e-receipts, create a folder on your computer or mobile phone where you store them month by month.

Being organized is part of the budget battle; you’ll thank yourself later.

We also keep the receipts for a year and longer if for expensive items or those with a time-sensitive warranty.

Grocery Savings

Save money on groceries with my Free Grocery Savings Budget Binder!

Whether you are a single shopper or a family, my Grocery Savings Budget Binder is for the frugal-minded consumer.

The Flashfood app Canada offers consumers savings of up to 50% off food products close to expiry from participating Loblaws stores such as RCSS, Zehrs, No Frills, and Dominion.

Please use my referral code, MOCD28ZN4, for a $3-5 credit.

Use the Flipp App for free to compare prices at grocery stores when creating your shopping list.

The Flipp app is a digital platform that puts local flyers and coupons in one place to access discounts and deals.

Finding the best coupons in Canada is one of my most popular blog posts for grocery savings.

Whenever you can use a coupon or app to save money on groceries and household items, do it!

Fight to change food costs with Grocery Apps and savings tips on pricey items such as dairy, meat, and produce.

- Tips To Help You Save Money When Buying Meat At The Grocery Store

- How To Save Money Buying Dairy Products At The Supermarket

Canadians need an edge to stay afloat, and Grocery Apps can provide budget-friendly options.

Also, like the Flashfood app, Food Hero is another food savings app that services Quebec and Montreal but not Ontario.

Users will find deep savings on produce, dairy, meat, and prepared foods with shorter lifespans on these apps.

However, you will also find dry goods, non-perishables, specialty items, household, health and beauty, and over-the-counter medication.

Sign Up Here: Free Sign Up For Food Hero. Use my code moc102 to get $5!

2024 Food Price Index Comparison

Below are just some of the 106 food items from the Stats Canada 2024 Consumer Price Index that detail average prices from June 2024 until October 2024.

As you can see, prices started strong but have slightly dropped over the past few months.

For example, 4 Litres of milk started at an average of $6.65 in June 2024 but decreased to $6.60 by October.

Whether this price decrease continues to be the trend into 2025, we’ll have to wait and see.

Nonetheless, using all available grocery-saving tools to reduce costs is essential.

| Milk, 4 litres4 | 6.65 | 6.58 | 6.65 | 6.64 | 6.60 |

|---|---|---|---|---|---|

| Soy milk, 1.89 litres5 | 4.47 | 4.52 | 4.68 | 4.36 | 4.34 |

| Nut milk, 1.89 litres5 | 4.31 | 4.31 | 4.34 | 4.27 | 4.16 |

| Cream, 1 litre4 | 4.67 | 4.69 | 4.74 | 4.65 | 4.51 |

| Butter, 454 grams4 | 6.02 | 6.30 | 5.76 | 5.49 | 5.71 |

| Margarine, 907 grams5 | 7.26 | 7.51 | 7.31 | 7.41 | 7.35 |

| Block cheese, 500 grams5 | 6.83 | 6.84 | 6.90 | 6.86 | 6.73 |

| Yogurt, 500 grams5 | 3.47 | 3.56 | 3.55 | 3.49 | 3.55 |

| Eggs, 1 dozen4 | 4.42 | 4.74 | 4.71 | 4.87 | 4.66 |

| Apples, per kilogram4 | 5.78 | 5.70 | 5.63 | 4.36 | 4.13 |

| Oranges, per kilogram4 | 4.18 | 3.98 | 4.31 | 4.55 | 4.75 |

| Oranges, 1.36 kilograms4, 5 | 5.34 | 5.04 | 5.65 | 5.57 | 5.98 |

| Bananas, per kilogram4 | 1.65 | 1.64 | 1.65 | 1.65 | 1.63 |

Cut Spending By Price Matching

Price matching is using either paper flyers or your mobile device app, where applicable to the cashier, to get the best price on a product you want.

For example, if you live close to a store that allows price matching, grab the identical item in a local grocery flyer and show the cashier that sale.

You no longer have to carry paper flyers if you have a mobile phone and can share the sale with the cashier.

They will apply the sale price, helping you save money by shopping in one store instead of travelling to multiple grocery stores.

The advantages of price matching are time and promoting savings awareness.

FYI, other stores besides the supermarket offer price matching.

Building A Stockpile To Cut Spending

Stockpiling is a great way to save money when you find a deal on a product you know you will use often.

Part of our grocery budget includes a stockpile budget of $25 each month tailored to accommodate any deals we can pick up at stockpile prices.

Our savings system allows us to focus on our central grocery budget for everyday needs and the stockpile budget for using coupons paired with flyer deals or in-store specials.

Having a stockpile budget also holds you accountable and gives you direction because you know you only have a set amount of money to spend.

A great example was when the GreenWorks products were on sale for 1.99 each but had a buy three save $5.00 coupon hanger on each bottle.

We were paying under $2 for three bottles of product that should have cost us around $18 at regular price with taxes.

It was like a never-ending stockpile of cleaning products we purchased that lasted over five years.

Buying In Bulk

Shopping in bulk can save you money only if you need the product and will use it before it expires.

You’ve compared the price in bulk to sales at your local grocery stores.

For example, you can buy a 5L jar of Bick’s Pickles for $4.99 at Costco and 1L at Zehrs for $4.99 at the regular price when it goes on sale.

You might even have a coupon to lower the price, but you won’t know that until you purchase.

It might be ideal to buy the 5L jar if you love to eat pickles.

Besides, pickles last long, so you wouldn’t have to rush to eat them fast.

Although buying larger quantities may not always be on sale, always do the math and consider the financial consequences if you don’t use the product.

Remember, a few dollars here and there all add up throughout your lifetime.

Rain Check Savings

Never leave a grocery store empty-handed when there is a sale and they are sold out.

Always ask customer service if they will offer you a rain cheque.

Suppose the store does offer a rain check; they typically allow you to get up to 4 of the sales the next time you shop, and they are in stock.

However, read the fine print on sales as it might say, “while supplies last,” which means no rain checks will be available.

Creating Organized Lists

Making a list is undoubtedly a great way to save money, whether you shop at a grocery store or your nearest hardware store.

The list’s purpose is to allow you into detail what you need before you shop.

A marketing plan for any business begins the minute you walk in the door, from displays to smells.

These distractions can cost consumers money, so they should arm themselves with a list.

Find loads of Free organization-type lists for printing here on CBB!

Meal Planning Cuts Spending

A weekly or monthly meal plan direction can relieve stress and save money because you aren’t scrambling to find the ingredients.

Remember that meal planning also allows you to shop for weekly deals at your local grocery store to help save you money.

For example, if the beef is on sale, you buy two packages, one for a pot of chili and the other for an Italian Bolognese meat sauce.

These two meals you plan may feed your family for lunch and dinner a few days during the week.

Although meal planning is a way to cut spending, remember that planning around what you already have in your pantry is another level of savings.

Use what you already have instead of buying more to add to your stockpile.

Did you know that lentils are inexpensive, nutritious, delicious, and protein-loaded?

{kind=link}

{kind=link}

Scanning Errors

If you have never heard of SCOP in Canada (Scanning Code Of Practice), it’s a program that saves you money while helping a company realize its pricing errors.

SCOP is when you find an advertised product for one price but are charged more when cashing out.

Not all stores offer SCOP, so it’s essential to understand that it’s NOT a law in Canada.

If you find it’s for more than the tagged price, you should point that out and ask for SCOP to be applied, and you will get the product for free, up to a maximum of $10.

Additional Canadian Savings Opportunities in 2025

Some additional areas that you might consider savings opportunities in 2025.

Cut Savings By Eating In vs. Eating Out

Take-out food once or twice a month is fine if you budget for entertainment, eating out, or give yourself an allowance.

Allowing yourself to eat outside the home too often may affect your finances.

No matter what anyone tells you, eating at home will always cost you less and save you far more money in the long run.

Besides, there are copycat recipes for just about every restaurant and fast food place that you can think of.

Perhaps putting those extra savings towards paying down debt may help motivate you to learn to meal prep and cook at home.

Bad Habits

Whatever you consider your bad habit, try to be mindful of the expenses involved and how you can save money by cutting back or eliminating it.

Memberships

Memberships are great if you use them, especially when you buy them on a whim.

A big money-flop for Canadians is an unused gym membership, which starts with good intentions and ends with monthly payments and little to no visits.

Clothing

We’re believers in recycling, reusing, and re-purposing whenever possible, which means buying secondhand is our first place to shop, especially for clothing.

Always consider what you plan to buy to mix and match outfits, and don’t buy more clothing than you need.

Whether you shop secondhand or not too much means your closet will be bulging full of clothes you probably will only wear once or twice, if ever.

Keep an eye out for online savings from clothing retailers in Canada, and sign up for your favorite shops, which often send discount codes to their VIP customers.

Transportation

Walking, Biking, and taking the bus, subway, or go-train are ways to save money on transportation and exercise simultaneously.

Getting rid of your ride is not always optimal, so consider comparison shopping regarding vehicle insurance and anything related to your vehicle.

When buying a new vs. used car, there are no wrong and right answers apart from ensuring you are covered if something were to go wrong.

The last thing you want is to have a lemon taking up space in your parking space or driveway.

Use your rewards or credit cards to earn and redeem points at your local petrol station.

Also, if you are a Costco member and there is a gas station at your store, the savings are always better than any station in your community.

Canadian Rewards Programs 2025

Canada’s most lucrative rewards program, the PC Optimum program, may already be in your wallet.

Rewards programs help Canadians save money and earn points towards products or cash back.

Related: The Ultimate Guide: Cashback Apps For Online Canadian Shopping

Take the time to explore your options and pick what works because leaving free money on the table is not smart saving.

We earn and save with the below programs, including credit card rewards.

- Credit Card Rewards and Loyalty Programs

- Rakuten Canada

- Nielsen Home Scan Canada

- Swagbucks Canada – Read my review of Swagbucks here.

- Air Miles Canada

- PC Optimum Rewards at Shoppers Drug Mart and Loblaws Stores

Explore all of the Canadian Money Savings possibilities shared on CBB.

Employment/Earn More Money

Saving money in Canada is not always easy, especially when you struggle to balance your budget.

Aside from slashing what you spend your money on, you can save money by earning more.

Second Job

If you can’t balance your budget, the first option is to eliminate or lower your expenses, which can be a struggle.

You may feel as if nothing is left to reduce or cut or are unwilling to give something up.

The other option is to get a second job to earn more money and supplement your budget.

Although you may be spending more time away from home, you’re earning more money that can help pay down debt,

Having a second job helped speed up paying our mortgage, but I was also able to secure full-time employment in my dream job simultaneously.

Side Hustles

Earning money on the side is a great way to save more in Canada.

Why do most Canadians start a side hustle?

- Saving or Spending Money

- Pay off debt

- Making ends meet

- Supplement part-time or no job.

- Build a business

Blogging, for example, is a secondary income for many people who offer their skills and knowledge to consumers online.

I started blogging in 2012 with zero knowledge and now earn a 5 figure income.

Below is a three-part series about how you can start a blog and earn an income.

If you have skills in demand, advertise them and watch the extra cash.

Other Canadian side hustles may include any of the following:

- Photography

- Tutoring

- Pet Sitting

- Reselling

- Social Media Management

- Fitness Trainer

- Podcasting

- Freelance Writing

- Transcribing

- Rideshare Driving

- Virtual Assistant

- Rent A Room or Space

- Social Media Influencer

Ask For A Raise

Please don’t wait for the raise to come; grab it.

I also know that it may seem far-fetched these days the way the Canadian economy is sitting.

However, stand up for your skills and education and ask your boss for a raise.

If they say yes, use the extra cash to pay off debt or stash it in your savings or retirement account.

One of my biggest regrets with my first job in Canada was not asking for a raise, which I strongly encourage.

The worst your employer will say is no, so ask your boss for a raise today!

Upgrading Skills

There was never a time when I thought that education was a waste of time.

Any opportunity you get to upgrade your skills or learn new skills that you can apply to your career will only help you earn more money.

Upgrading your skills may mean returning to college or university.

You can research many online courses and find one that fits your educational direction.

Networking

When I moved to Canada, I returned to school at 30 to upgrade my skills and improve my life.

Education was not part of my plans, but it was the only way to increase my opportunities in Canada and find a career where I could earn more than minimum wage.

Along the way, I was able to network with different business owners in my field, volunteer my time, and eventually secure an employment opportunity.

That one opportunity helped me to get a second job, which ended up being my dream job, where I currently work full-time.

It took me five years to get my foot in the door, working two jobs for my permanent employment offer, but I did it.

I’ve also met lots of people during my time as a soccer coach and at church.

Personal Experiences

Finally, I started what I believed would be a little finance blog documenting our financial journey, only to learn that thousands of Canadians wanted to follow along.

I never realized the impact your personal experiences could have on the lives of those who need motivation the most.

Earning money from blogging was not my intention, but it slowly moved in that direction, which was a nice little perk to our savings.

Ideally, if you want to save money in Canada, find something you love to do and bring it to life, even if it requires baby steps, which most opportunities do.

The saying, “You can’t win the lottery if you don’t play,” comes to mind, and although “I’m not referring you to the lottery, I’m simply stating that risk will not always yield unfavorable results.

Comparison Websites

- Grocery Prices (Flip App) This app has everything from all your weekly flyers to coupons to help you create the ultimate list to save money.

- Petrol Prices (Gas Buddy) If you want the best bang for your buck when filling your gas tank, then Gas Buddy will tell you where to go for the best savings.

- Car Insurance, Home Insurance, and Mortgage (Smarter Loans) Comparison websites such as Smarter Loans help you to decide the best loan rates to fit your budget and help save you money.

Debt Reduction

Canadians endure many types of debts, some of which help enrich our lives to help us work towards employment success and others to build wealth, such as a mortgage.

One thing to remember is that debt is debt, but the worst debt is consumer debt or any debt you can’t repay, such as a mortgage, credit card, or personal loan.

5 Leading Types Of Debt Canadians Hold

- Credit Card (use balance transfer options, snowball debt reduction method)

- Personal Loans are those where you borrow a fixed amount of money and pay it back over a certain amount of time.

- OSAP

- Consumer Debt

- Mortgage

Ideally, trying not to create debt you can’t pay back in whole or reasonably, besides a traditional mortgage school loan, is ideal.

The more debt you create, the harder it gets to spread your money, leading most Canadians into big trouble.

If you want to smash your debt, work on reducing it by finding a second job, working overtime or extra hours, or creating a business where you can work from home.

13 Key Points To Remember To Cut Spending

- Saving money in Canada can be challenging but requires desire and determination.

- Budgeting is a must to know where your money is going.

- Comparing prices is essential to getting the best prices in Canada.

- Always keep your receipts.

- Consider your present and future when saving and investing money.

- Don’t spend more than you earn.

- Buying a house is not the end all be all.

- Less Is More

- Don’t be afraid to negotiate deals or prices.

- Instead of spending money to buy new things, reach out to friends and family and borrow.

- Always have a contingency plan.

- A side hustle is nice to have if your primary income sources dissolve.

- Financial literacy is not something you will learn overnight. Continue to read and be mindful of how finance impacts your life.

Read and Keep Reading Because Finance Never Ends

For anyone needing that extra push in 2025, a motivational read worth buying is Canadian finance blogger, podcaster, and now author Jessica Moorehouse’s new book, “Everything But Money.” (non-affiliate)

Jessica, a millennial money expert, details the hidden barriers between you and your money.

I wish you all a financially fit year and hope you continue to thrive with your budget and conquer debt promptly that works for your lifestyle.

As always, I appreciate your continued support of Canadian Budget Binder and encourage you to subscribe for an exciting 2025 season.

Thanks for reading.

If you have any questions or comments, please leave them below.

Mr. CBB